Case Summary: Brightmark Chapter 11

Brightmark has filed for Chapter 11 bankruptcy to pursue a 363 sale, citing liquidity constraints and operational challenges, with junior DIP financing in place to support operations.

Business Description

Headquartered in San Francisco, CA, Brightmark Plastics Renewal LLC (“Brightmark Ashley”) and its affiliated Debtors⁽¹⁾ (collectively, "Brightmark" or the "Debtors") operate a plastics recycling circularity center in Ashley, IN.

- The facility leverages advanced pyrolysis technology to convert post-consumer and post-industrial plastic waste into PyBright™, a pyrolysis oil that serves as a sustainable alternative to virgin fossil fuels.

- Designed for a 100,000-ton annual capacity, the Circularity Center is currently operating at approximately 5% of this volume.

- To date, the Debtors have recycled over 10 million pounds of plastic and are working to increase production while addressing operational challenges.

Operations rely on proprietary licensed technology (“Licensed IP”) from non-Debtor Brightmark Plastics Renewal Technologies LLC, with the license limited to a single facility with six pyrolysis vessels and exclusive rights within a 300-mile radius of the Circularity Center.

Brightmark filed for Chapter 11 protection on Mar. 16 in the U.S. Bankruptcy Court for the District of Delaware. As of the Petition Date, the Debtors reported $100 million to $500 million in both assets and liabilities.

⁽¹⁾ Brightmark Plastics Renewal Indiana LLC ("Brightmark Indiana") and Brightmark Plastics Renewal Services LLC (“Brightmark Services”).

Corporate History

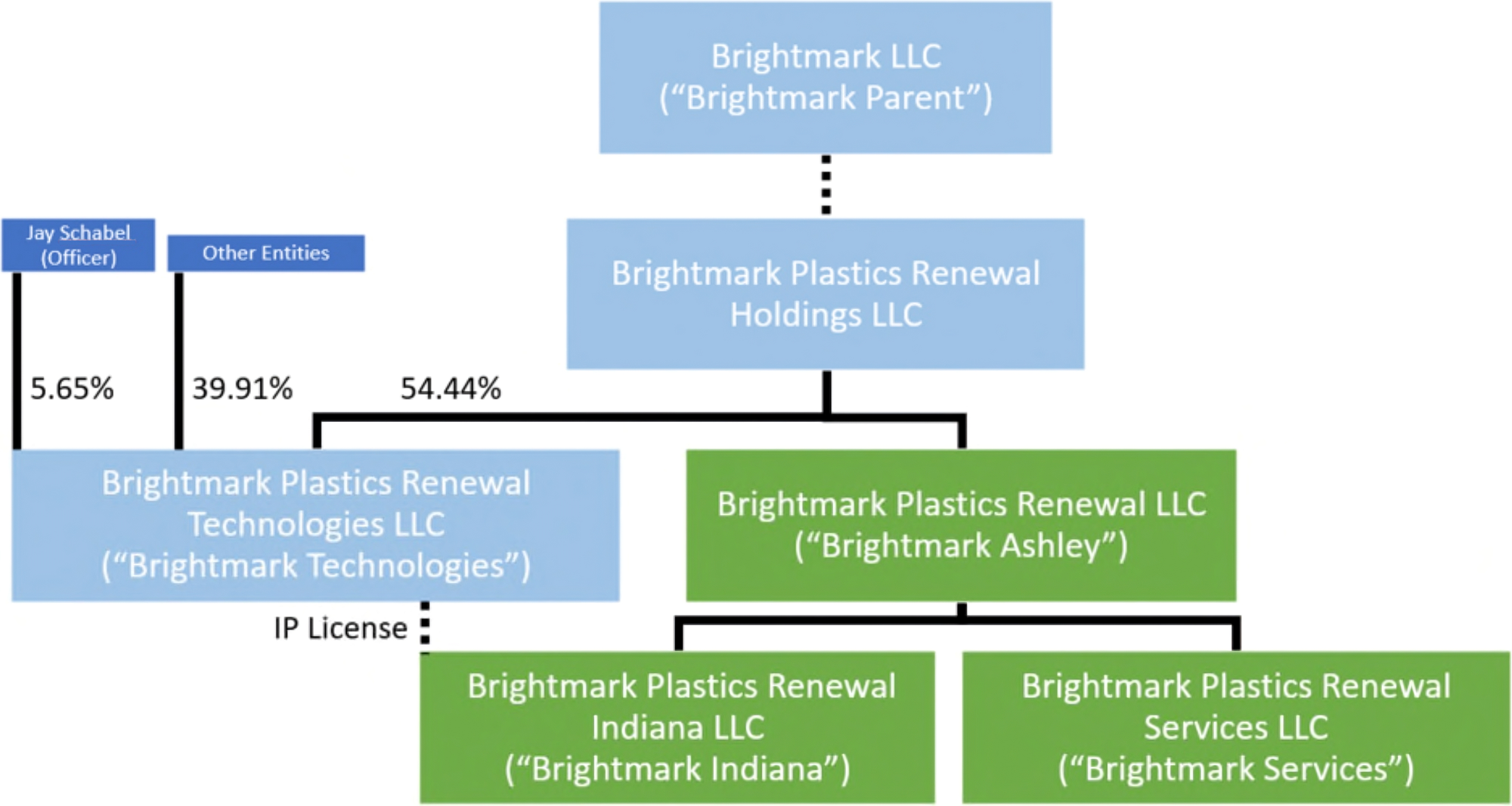

The Debtors are indirect subsidiaries of Brightmark LLC (“Brightmark Parent”), founded in 2016 with a mission to renew waste products for economic and environmental benefit. Key milestones include:

- Brightmark Indiana – Established in September 2016 as RES Polyflow Indiana LLC, this entity serves as the operating company, owning the Circularity Center and acting as the licensee of the Licensed IP.

- Brightmark Ashley – Formed in January 2018 as BME Renewable Polyfuels LLC, Brightmark Ashley acts as the holding company for the other Debtors. Brightmark Parent acquired a minority interest in October 2018 and increased ownership to 100% by February 2022.

- Brightmark Services – Established in October 2018 as BME Polyfuel Services LLC, this entity provides operational and managerial support to Brightmark Indiana.

- Circularity Center – Construction began in 2019, with the first sale of pyrolysis oil occurring in 2023.

Organizational Structure

- The Debtors’ operations are heavily reliant on shared services and management from Brightmark Parent, with costs allocated across the corporate structure to support operations.

Operations Overview

Brightmark’s operations center on converting plastic waste into PyBright™, a sustainable alternative to fossil fuels that commands a premium price.

- Brightmark sources mixed plastic waste primarily from Midwest-based third-party suppliers.

- The facility’s operations are complex, requiring specialized spare parts, continuous maintenance, and strict compliance testing.

Capital Projects

According to the Debtors, over $100 million in capital investment is required to scale operations and achieve sustainable operational profitability over the coming years. Capital projects are focused on:

- Upgrading existing equipment, addressing health, safety, and environmental concerns.

- Enhancing PyBright™ quality to increase its market value.

Customers

Brightmark sells PyBright™ to three petrochemical companies, with demand exceeding current and projected production capacity.

Workforce

The Debtors employ approximately 113 individuals through Brightmark Services, consisting of salaried employees, hourly workers, and independent contractors. The workforce is critical for sustaining operations, supporting mechanical services, quality assurance, and customer relations.

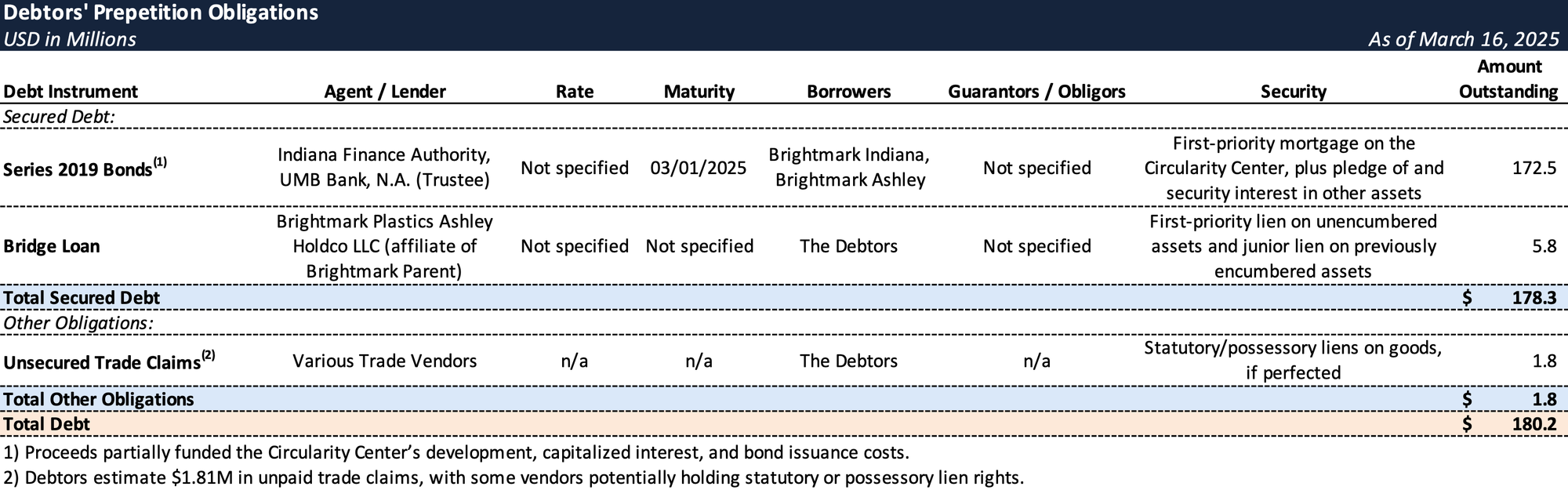

Prepetition Obligations

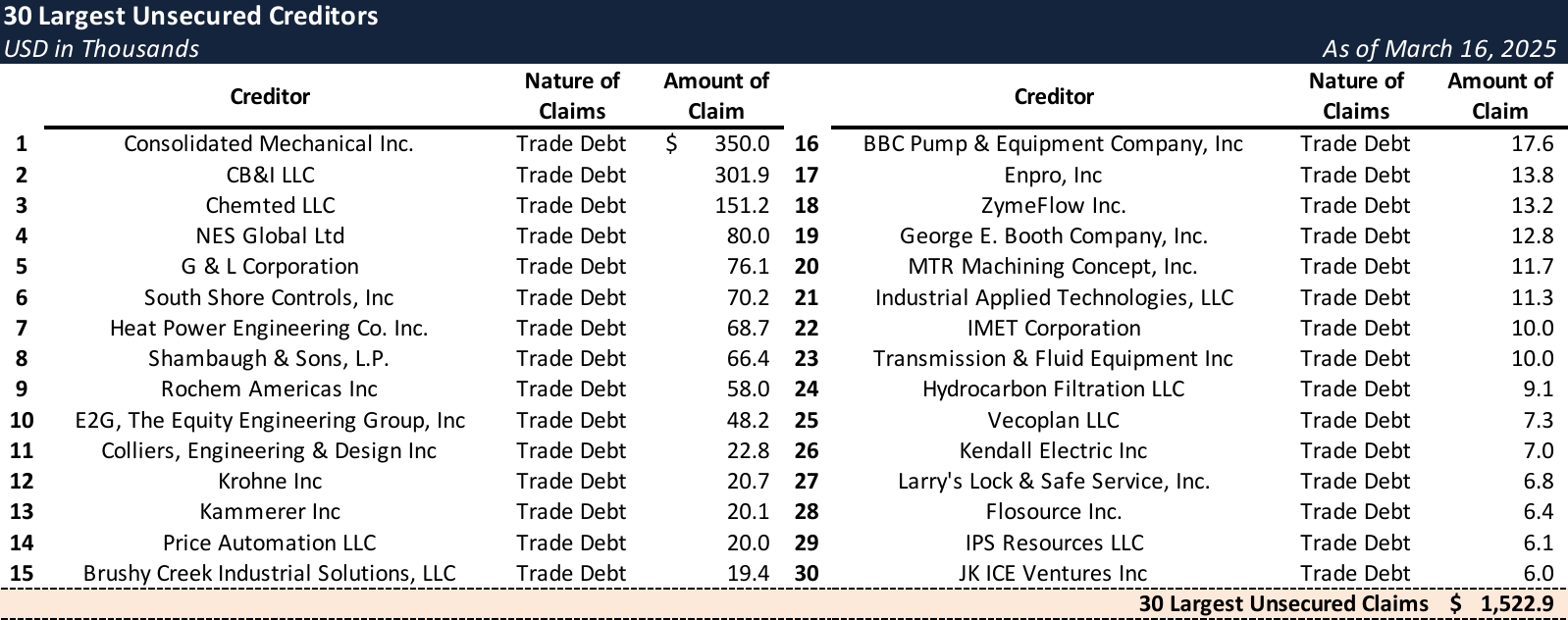

Top Unsecured Claims

Events Leading to Bankruptcy

Project Design Flaws and Strategic Shift

- Brightmark’s original vision centered on converting plastic waste into fuels and wax through a three-step process: feedstock preparation, pyrolysis conversion, and an upgrade system to refine the resulting oil into commercial products. However, after launching its Circularity Center, critical components of the facility failed to operate as designed, requiring significant redesign and engineering fixes.

- As market conditions evolved, Brightmark pivoted away from fuel production, focusing instead on producing pyrolysis oil for circular plastics. The Circularity Center has so far only yielded PyBright™, diverging from its initial business strategy.

Operational Underperformance and Financial Strain

- The Circularity Center has struggled to reach its intended processing capacity, resulting in revenue shortfalls that have hampered Brightmark’s ability to cover operating expenses. More than three years after mechanical completion and two years into production, the facility remains significantly underutilized.

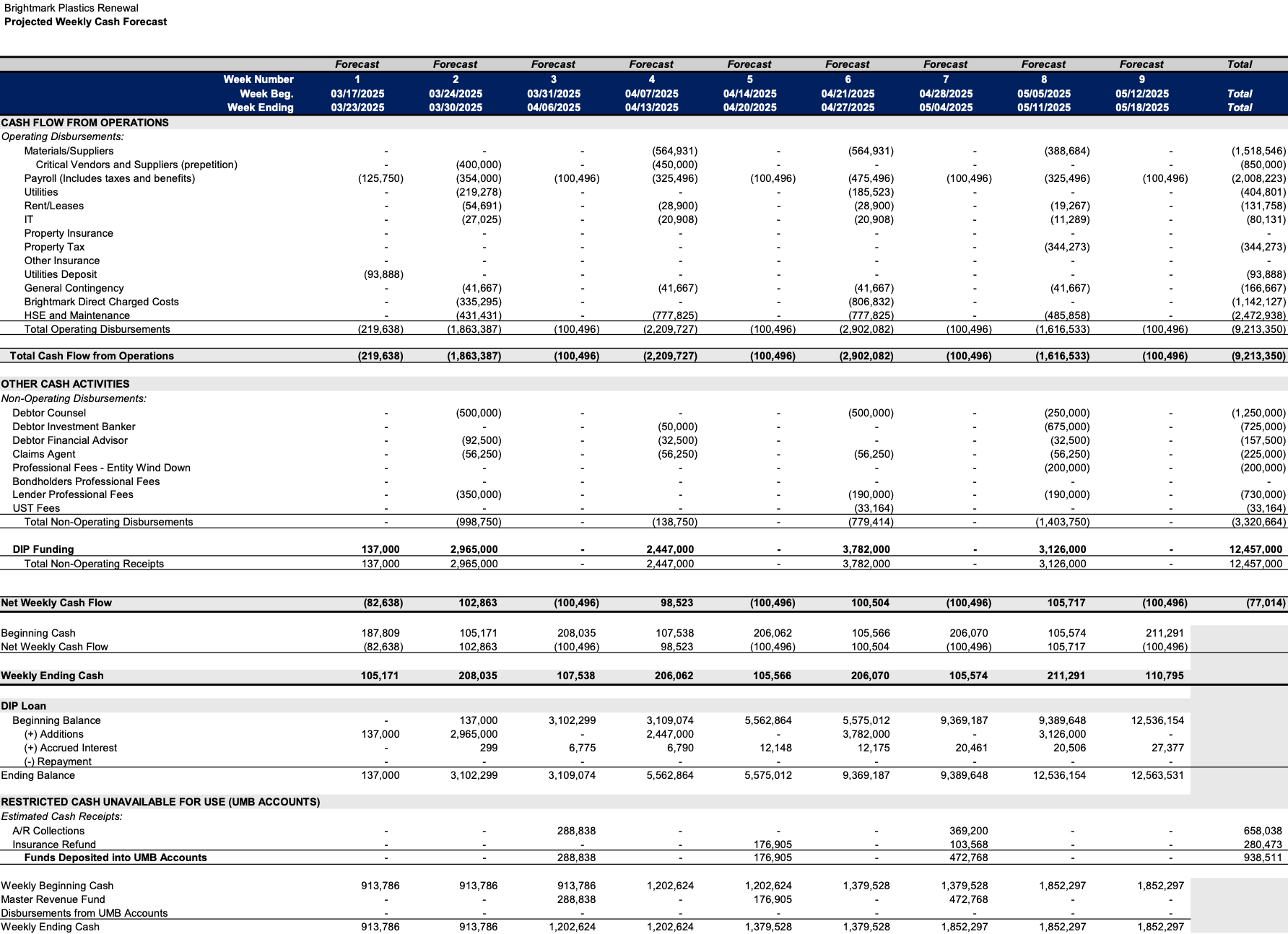

- Weekly cash burn for operations and required capital improvements stands at ~$800,000, excluding debt servicing.

Debt Burden and Limited Access to Capital

- Brightmark’s heavy senior secured debt load has constrained its ability to raise additional funds for operations, capital expenditures, and expansion efforts. Attempts to secure liquidity through conventional channels were unsuccessful, as ongoing operational struggles and capital-intensive requirements made the Debtors a challenging prospect for lenders.

- Efforts to secure junior secured financing from six alternative asset-based lenders failed to yield viable offers, while senior secured options were blocked by the Prepetition Secured Parties.

Strategic Review and Sale Process

- Amid mounting financial pressure, Brightmark launched a strategic review, appointing an Independent Manager and a Chief Restructuring Officer to oversee the process. The Debtors retained SSG Advisors, LLC to explore strategic alternatives, ultimately determining that a court-supervised sale under Section 363 represented the best option for maximizing creditor recoveries.

Sale Process and DIP Financing

- Prepetition Secured Parties showed late-stage interest in providing DIP financing but failed to finalize terms pre-filing, leaving the Debtors without a senior funding solution.

- To avoid priming disputes and preserve going-concern value, Brightmark negotiated a junior DIP facility with the Bridge Lender, an affiliate of Brightmark Parent.

- The DIP facility provides up to $13 million in postpetition liquidity on a junior basis, with no priming or roll-up of prepetition debt.

- Funds will support operations through the conclusion of the sale process.

Initial Budget

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

If you’re already a subscriber and would like to receive timely filing alerts, please reach out and we’ll add you to the distribution list.