Case Summary: RAD Diversified REIT Chapter 11

RAD Diversified REIT filed Chapter 11 following an SEC order declaring its offering statement abandoned, an ongoing Florida Attorney General investigation characterizing the enterprise as a potential Ponzi scheme, and mounting foreclosures across its portfolio of over 300 properties and vacant lots.

Business Description

Headquartered in Port Richey, FL, RAD Diversified REIT, Inc. ("RAD REIT"), along with its Debtor⁽¹⁾ affiliates (the "Debtors"), was an externally managed, real estate investment trust formed to acquire, renovate, lease, and manage income-producing real estate at discounts to fair market value. The REIT targeted single-family and multi-family residential properties, mixed-use buildings, income-generating farms, and vacant lots, sourced through on-market and off-market transactions, tax deed foreclosure sales, bank foreclosures, "real estate owned" acquisitions, and other transactions. All investment decisions were made by RAD Management, LLC, a Delaware LLC controlled by co-founders Brandon "Dutch" Mendenhall and Amy Vaughn.

As of the Petition Date, the Debtors' portfolio comprised more than 300 residential rental properties and vacant lots located predominantly in Pennsylvania, Texas, and Florida, with additional holdings in New Jersey. The largest concentration consisted of nearly 100 rowhouses in Philadelphia's low-income neighborhoods, while the Debtors also held approximately 2,282 acres in Randolph County, Arkansas.

- The Debtors received total rental income in excess of $90,000 in each of December 2025 and January 2026, though the Declaration (Doc 3) notes that many properties were vacant and numerous tenants had withheld rent after being served with foreclosure lawsuits.

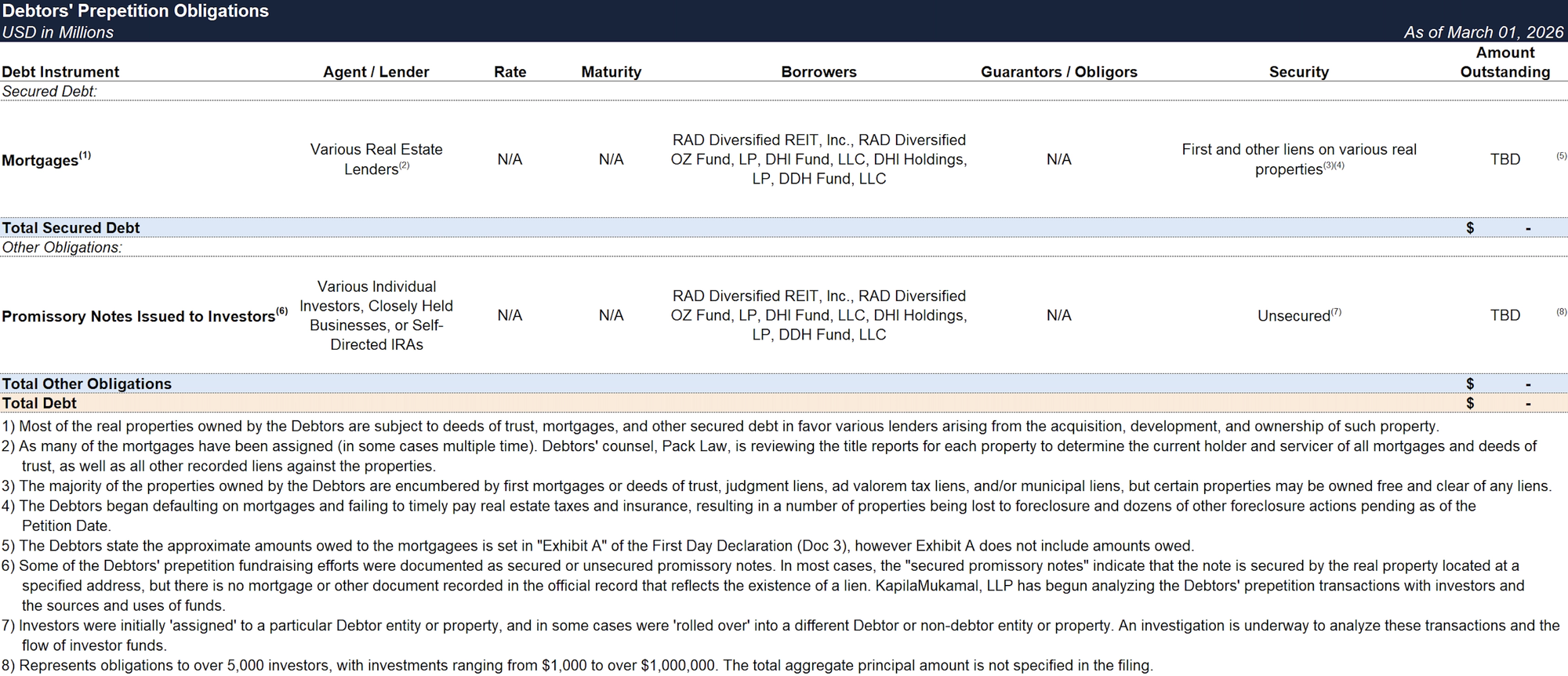

The Debtors engaged in a variety of prepetition fundraising efforts from more than 5,000 investors—largely individuals, closely held businesses, and self-directed IRAs—including Regulation A and Regulation D offerings. Beyond equity offerings, the Debtors raised additional capital through secured and unsecured promissory notes, joint ventures, and direct equity investments, with investors sometimes "assigned" to a particular Debtor entity or property and later "rolled over" to a different Debtor or non-Debtor entity. Individual investments ranged from $1,000 to more than $1 million.

RAD Diversified REIT, Inc. and four affiliated entities filed for Chapter 11 protection on March 1, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Middle District of Florida, reporting $50 million to $100 million in both assets and liabilities.

⁽¹⁾ For a complete list of debtor entities, see Chapter 11 Debtors table below.

Corporate History

RAD Diversified REIT, Inc. was incorporated in Maryland on May 11, 2017 and elected REIT status effective November 1, 2019. RAD REIT traces its origins to a series of predecessor entities, affiliated real estate investment vehicles, formed prior to RAD REIT's creation and managed by the same principals. Limited partners of these predecessor entities received shares of RAD Diversified REIT in connection with a restructuring completed around June 2020, with intercompany promissory notes issued in the process.

Founders and Marketing Machine

RAD REIT was co-founded by Mendenhall and Vaughn. Mendenhall served as CEO, President, and a Director; Vaughn served as CFO until April 2020 (when Mendenhall assumed interim CFO duties) and remained on the Board.

The Debtors' marketing strategy included running simultaneous Facebook ads, promoting heavily on Instagram and YouTube, and hosting in-person events including "Invest Wealth Summit" and "Inner Circle Retreats" featuring paid celebrity speakers such as Grant Cardone and Tucker Carlson.

- Marketing materials promised significant annual returns and touted a substantial stock price increase from 2019 to 2023. Investors could purchase shares via credit card—highly unusual for securities—and were encouraged to take out home equity lines of credit to fund investments. Inner Circle membership reportedly required $50,000.

Capital-Raising Pathway

- RAD REIT commenced its Regulation A offering on November 1, 2019, with the SEC qualifying a post-qualification amendment on January 19, 2022 for an ongoing offering capped at $75 million. Through March 15, 2023, RAD REIT had issued 3,811,552 shares for total gross proceeds of approximately $73.8 million.

- In December 2021, RAD Diversified OZ Fund LP, a Qualified Opportunity Zone fund, was formed. On September 8, 2022, a separate vehicle, RAD Diversified Land REIT, Inc. (d/b/a RADD America), was formed and later filed its own Regulation A offering in October 2023. Florida records show the entity registration was revoked in September 2025 for failure to file an annual report.

Chapter 11 Debtors

- The CRO has stated that certain affiliates owning non-residential real estate have not filed bankruptcy, and that investigations into intercompany transactions are underway.

Operations Overview

Management Fees

RAD Management, LLC collected three layers of fees from the REIT: a property management fee equal to 4% of gross revenue, paid monthly in arrears, a financial management fee of 20% of any increase in net asset value (excluding investment activity), and a $1,000 acquisition fee per property. A March 2022 Philadelphia Inquirer investigation found that over 60% of the Debtors' 2020 operating expenses—more than $730,000—flowed to insiders through these fees, even as the real estate business lost $1.12 million in the first half of 2021.

Property-Level Leverage

The majority of the Debtors' properties are encumbered by first mortgages or deeds of trust, plus judgment liens, ad valorem tax liens, and/or municipal liens, though some may be owned free and clear. Repeated note assignments and servicing transfers have complicated lien identification, requiring title-by-title review by counsel to determine current holders and servicers.

- Prepetition management represented that certain properties retain equity and that others need only minor repairs to return to a rentable condition, but the CRO and the Debtors' advisors have not yet independently verified values, liens, or conditions at the property level.

Investor Documentation Gaps

The CRO flags material concerns about how investor interests were documented:

- "Joint venture" investors were in most cases not reflected on property deeds or in official records.

- "Secured promissory notes" referencing specific property addresses often lacked recorded mortgages or other lien instruments.

Cash Management

Tenant rents flow through AppFolio property management software and transfer by ACH into the REIT's prepetition bank account. The Debtors are establishing DIP accounts—with GGG personnel as sole signatories—though the AppFolio ACH redirection requires approximately 30 days. Post-petition rents, estimated at roughly $90,000/month, are expected to be the Debtors' sole revenue source and will fund insurance, taxes, maintenance, and case administration.

Intercompany Complexity

The CRO notes significant intercompany transactions among Debtors and non-Debtor affiliates, with books and records maintained on a consolidated basis and many expenses unallocated across entities. KapilaMukamal, LLP has been engaged for forensic accounting services, including tracing the sources and uses of investor funds. The Debtors anticipate more than 7,500 creditor and investor claimants and have sought appointment of Epiq Corporate Restructuring, LLC as claims and noticing agent.

Prepetition Obligations

Events Leading to Bankruptcy

Early Scrutiny (2022)

- In March 2022, the Philadelphia Inquirer published an investigative report revealing that the Debtors' real estate operations lost $1.12 million in the first half of 2021, that more than 60% of 2020 operating expenses flowed to insider management fees, and that approximately 20 properties purchased by DHI predecessor funds appeared in SEC filings as RAD holdings despite public records showing no recorded title transfers.

- Some Philadelphia properties listed as generating rental income were actually boarded up with no rental licenses—4243 Leidy Avenue, for instance, was claimed to produce $14,400/year in rent despite being vacant and boarded.

- RAD REIT's own offering circular warned: "If we are unable to continue to raise sufficient capital through this offering, there is a strong likelihood our business will fail and you may lose your entire investment."

SEC Action and Redemption Freeze (February 2024)

- On February 2, 2024, the SEC declared RAD REIT's Regulation A offering statement "abandoned," terminating the Debtors' ability to raise capital from non-accredited investors. RAD REIT had filed multiple amended 1-A forms, but the offering circular never received qualification. It had also stopped filing annual reports (Form 1-K) after FY 2021 and semi-annual reports (Form 1-SA) after September 2022.

- On the same day, the Board froze the Share Redemption Program, refusing all pending and new redemption requests. The freeze was subsequently extended at the April 1 and June 27, 2024 board meetings and appears to have remained in effect through the Petition Date.

Communication Blackout and Office Eviction (2024–2025)

- Throughout 2024 and 2025, investors increasingly reported difficulty contacting RAD REIT, including disconnected phone numbers and unanswered emails.

- In May 2025, the landlord of RAD REIT's Tampa office at 100 S. Ashley Drive, Suite 700 filed an eviction action that the CRO Declaration confirms "received substantial publicity."

Florida Attorney General Investigation (July 2025)

- In July 2025, Florida Attorney General James Uthmeier issued investigative subpoenas to RAD Diversified REIT, its subsidiaries, and Mendenhall and Vaughn personally, publicly stating: "This appears to be a Ponzi scheme, and with several individuals claiming they've been exploited, we are investigating to ensure Floridians are not being deceived by greedy fraudsters."

- The Debtors' prepetition management "strenuously disagrees" with the characterization, but the CRO Declaration acknowledges the accusation "crippled" the Debtors' ability to operate.

Mounting Litigation

- The Debtors' legal exposure spans multiple jurisdictions:

- Civil RICO suit: Nationally syndicated talk radio host Buck Sexton filed a federal racketeering complaint in the Middle District of Florida on August 25, 2025 (Case No. 8:25-cv-02261), alleging he was defrauded of more than $100,000 in connection with RAD REIT-related programs.

- Foreclosure actions: Southwest Georgia Farm Credit ACA sued over a $2.1 million loan, seeking judicial sale of 2,282 acres in Arkansas. RAD REIT itself filed at least eight federal suits in the Southern District of Texas (2024–2025) against lenders and trustees, apparently fighting to retain properties subject to foreclosure.

Loan Defaults

- The CRO Declaration attributes the Debtors' decline to multiple pressures: legal fees tied to regulatory matters, low occupancy, high overhead, stagnant real estate markets, and elevated mortgage interest rates. Over time, the Debtors began defaulting on Mortgages and Deeds of Trust and failing to timely pay real estate taxes and insurance. As of the Petition Date, the Debtors had already lost properties to foreclosure and deed-of-trust sales, with dozens more actions pending.

Independent Management and Emergency Filing

- In February 2026, the Debtors moved to install independent governance:

- On February 20, Katie S. Goodman was appointed CRO. Goodman is Managing Partner of GGG Partners, LLC.

- Subsequently, Michael T. Roye was appointed Independent Director, receiving full managerial authority via Independent Director Agreements.

- On March 1, 2026, the Independent Director authorized the Chapter 11 filings for all five Debtor entities.

Chapter 11 Objectives

- The Debtors have outlined three objectives for the cases:

- Forensic review and independent oversight: The CRO and Independent Director have engaged KapilaMukamal, LLP to investigate historical transactions, intercompany transfers, potential avoidance actions, and whether additional affiliates should file their own petitions.

- Assessment of Real Properties and Sale Process: The Debtors plan to sell certain properties and establish a post-confirmation trust to manage and liquidate the remainder, while negotiating consensual cash collateral use with mortgagees to fund insurance, taxes, and maintenance.

- Plan of reorganization: The Debtors intend to confirm a plan transferring all real property and claims to one or more trusts.

Key Parties

- The Debtors’ professional team includes Pack Law, P.A. (general bankruptcy counsel), GGG Partners, LLC (Katie S. Goodman, Chief Restructuring Officer), KapilaMukamal, LLP (financial advisor and forensic accounting firm), and Epiq Corporate Restructuring, LLC (claims and noticing agent).

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.