Case Summary: West Marine Chapter 11

West Marine filed for Chapter 11 with a dual-track plan to equitize $251.2 million in Term Loan Claims into 100% of new equity while paying ABL and FILO lenders in full, following post-pandemic demand decline, macroeconomic headwinds, and an overexpanded store footprint.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Fort Lauderdale, Florida, West Marine, Inc., along with its Debtor⁽¹⁾ affiliates (collectively, "West Marine" or the "Company"), is the leading omnichannel provider of marine aftermarket products in the United States, widely recognized as the principal resource for cruisers, sailors, anglers, yachters, and other boating enthusiasts.

The Company generates revenue through brick-and-mortar retail and wholesale, with eCommerce serving as the online sales channel for customers of both.

- Brick-and-mortar retail (roughly 200 leased stores spanning more than 34 states and Puerto Rico) generated just over 60% of 2025 revenue, and the wholesale arm, West Marine Pro, contributed just over 40%.

- The Company's two eCommerce sites — westmarine.com for retail customers and pro.westmarine.com for wholesale customers — accounted for approximately 8% of 2025 revenue.

Critically, retail and wholesale are operationally interlocked. West Marine offers cross-channel fulfillment options, including West Marine Pro delivery vans, buy-online-pickup-in-store, ship-from-store, and ship-to-store. 85% of U.S. marinas sit within thirty minutes of a West Marine trade area, underscoring the strategic positioning of the footprint.

- The Company's roughly 2,600 employees, referred to as "Crew Members", anchor the "boaters helping boaters" identity.

- In 2024, West Marine became the only retailer to sell marine products certified to American Boat & Yacht Council safety standards.

The Company's principal offices, located at 1 East Broward Blvd., Suite 200 — relocated from Watsonville, California in November 2022 — sit in close proximity to the flagship superstore in Fort Lauderdale, which the First Day Declaration describes as the store West Marine opened in 2011 as "the largest boating store in the United States". Store footprints range from 2,000 sq. ft. to 50,000 sq. ft. (the size of the Fort Lauderdale superstore), with aggregate annual lease expense of approximately $55 million.

West Marine, Inc. and its affiliates filed for Chapter 11 protection on May 17, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the District of Delaware, reporting $500 million to $1 billion in both assets and liabilities.

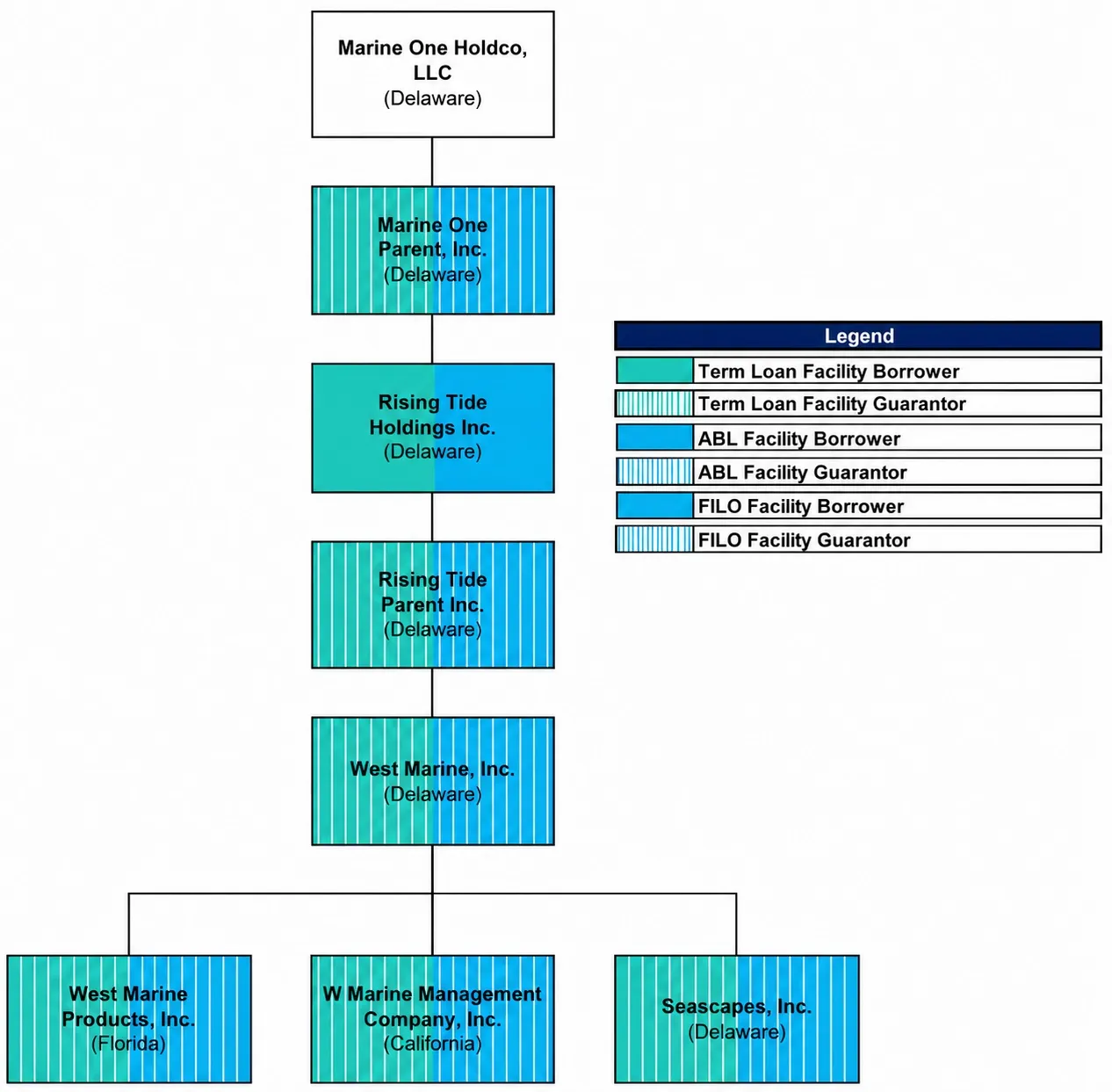

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

West Marine's arc spans nearly six decades: a 1968 mail-order rope business that grew into a 287-store retail leader, was taken private in a $338 million 2017 LBO, relevered by an LVMH-backed sponsor in 2021, and now arrives in Delaware bankruptcy court in 2026 after two out-of-court restructurings failed to right the balance sheet.

Randy Repass founded West Coast Ropes in 1968 as a mail-order branch of his father's New England Ropes business. The Company acquired certain assets of Boston-based West Products in 1977 (rebranding as West Marine Products), launched the Port Supply wholesale division (now West Marine Pro) in 1978, and launched its NASDAQ IPO on November 19, 1993 under the ticker WMAR. It merged with E&B Marine in 1996 (+64 stores), and acquired BoatU.S.'s retail, catalog, and wholesale divisions in 2003 for ~$72M (+62 stores; ~$140 million annual sales). The Company opened its NY flagship store and reached 287 locations nationwide in 2013.

September 2017 — Monomoy Take-Private LBO

On June 29, 2017, West Marine announced a merger with an affiliate of Monomoy Capital Partners at $12.97 per share in cash, valuing the equity at ~$338 million — a 32% premium to the 30-day average stock price on NASDAQ; the deal closed in September 2017. Guggenheim and Sidley advised West Marine; Jefferies and Kirkland & Ellis LLP advised Monomoy; Bank of America and Pathlight Capital provided debt financing.

April 2021 — L Catterton Acquisition; LVMH-Backed Sponsor

On April 14, 2021, L Catterton — the LVMH-backed consumer-focused PE firm in Greenwich, CT — announced it had entered into a definitive agreement to acquire a controlling interest in West Marine from Monomoy Capital Partners; the transaction closed in June 2021. Barclays Bank PLC, Golub Capital LLC, and Nomura provided debt financing; Kirkland & Ellis LLP served as counsel to L Catterton.

March and September 2023 — Out-of-Court Recapitalizations

In March 2023, the Company recapitalized its balance sheet through a series of exchange offers with the overwhelming support of its then-existing lenders and equity sponsor (with 100% of first- and second-lien lenders consenting to the exchange). Existing first lien lenders could swap a portion of their term loans into a new super-senior 1A tranche, while second lien lenders could exchange up to $60M into a new 1B tranche (junior to the 1A Term Loan but senior to non-participating first-lien term loans) and anything above $60M into a new 2A second lien tranche. The ABL facility was also amended to add a FILO component. This transaction brought in ~$150M of new money ahead of the spring boating season — a cash flow generating period for the Company.

In September 2023, West Marine executed a consensual restructuring supported by the equity sponsor and 100% of the holders of its then-existing funded debt, equitizing ~$660M of funded debt and delivering ~$125M of new liquidity. L Catterton contributed approximately two-thirds of the $125M new-money tranche for approximately 33% of newly issued common stock while retaining control; the remaining approximately one-third came from a subset of then-existing lenders. S&P downgraded Rising Tide to "SD" on September 21, 2023, viewing the September exchange "tantamount to a default"; Moody's appended a Caa2-PD/LD limited-default marker on or about September 25, 2023, following the September 18, 2023 closing of the restructuring.

Sponsor Cap Table at the Petition Date

West Marine's equity is co-sponsored by L Catterton and Oaktree, with equity held principally through three vehicles on Exhibit A to the Voluntary Petition:

- LC9 Marine One Aggregator, L.P. (an L Catterton vehicle) — 3,302,975 common units plus 33,509,919 warrants (comprised of 265,485 warrants and 33,244,434 penny warrants), the largest block.

- OPIFVOF WM Holdings LP (an Oaktree-affiliated vehicle) — 1,182,786 common units plus 25,169,634 warrants (comprised of 8,218 warrants and 25,161,416 penny warrants).

- Oaktree-Copley Investments LLC — 1,659,610 additional penny warrants.

Approximately 200 lender and warrant holders round out the cap table — Jefferies, Prospect Capital, Evolution Credit, Barclays, AEA Middle Market Debt, Silver Rock, Pimco Dynamic Income Fund, and CLO managers (Octagon, Sound Point, Rockford Tower, ICG, OCP, GoldenTree, Crescent, Ivy Hill). Many also sit in the term-loan stack — a residue of the September 2023 equitization in which holders of 1B and 2A Term Loan claims received warrants — likely a driver of the high 93.9% equity-holder RSA support. Existing equity is cancelled under the Plan. The equity sponsor (L Catterton) and largest lender (Oaktree) contribute no fresh 2026 equity, but committed to fund at least $7.5M of Exit Term Loan new money (potentially upsized to $10M) (L Catterton $5M; Oaktree $2.5M committed, with the additional $2.5M offered to other Tranche A Term Loan Lenders).

CEO Succession

S&P cited "significant management turnover over the last year" as a credit concern in October 2023, noting it "heightens uncertainty in the company's ability to execute on its operating strategies". Five permanent CEOs followed the 2017 LBO close (with an interim CEO, Jeff Lasher, bridging Hyde's departure and Robinson's arrival) — Matt Hyde (departed October 2017), Doug Robinson (2018), Ken Seipel (2018–2021), Eric Kufel (2021–2022), and Chuck Rubin (2022–May 2025; former CEO of Ulta Beauty and Michaels) — before Paulee Day was appointed on November 13, 2025. Day joined in 2022 and rose through Chief Legal/HR Officer, CAO, and COO; she previously spent fifteen years at MarineMax, Inc. as Executive Vice President and Chief Legal Officer.

Organizational Structure

Operations Overview

West Marine's revenue runs through a single omnichannel operation spanning in-store retail, wholesale, and eCommerce across ~200 stores and 2 distribution centers. The Company offers comprehensive tech-enabled fulfillment solutions — including West Marine Pro delivery vans, buy online pick up in store, ship from store, and ship to store.

Three Channels and Operational Interdependence

Retail generated just over 60% of 2025 revenue, selling core boating products — including maintenance, electronics, sailboat hardware, anchors, dockings, moorings, engine systems, safety, electrical, plumbing, deck hardware, and boat covers — alongside apparel (including West Marine's own private label), footwear, clothing accessories, fishing, watersports, paddlesports, coolers, electronics, and waterlife lifestyle accessories. West Marine Pro, the wholesale arm, contributed just over 40%, stocking 85,000-plus products from over 1,000 marine vendors for professional boaters, sailors, other industry professionals, and government agencies. The two eCommerce sites — westmarine.com (~100,000 products) and pro.westmarine.com (the same functionality as the retail site, plus checking inventory levels across multiple locations, building requisition lists, and looking up invoices) — together accounted for ~8%.

Workforce

As of the Petition Date, the Company had approximately 2,600 employees, spanning (i) storewide - sales associates, cashiers, and merchandise experts; (ii) distribution centers - general warehouse associates, order management associates, and inventory specialists; (iii) marketing - social media specialists, marketing associates, and photographers; (iv) transportation - transportation coordinators and vehicle operators; and (v) equipment - rigging associates, hazard specialists, and equipment operators.

Lease Portfolio

All of the Company's ~200 stores are leased, with stores ranging in size from 2,000 sq. ft. to superstore proportions of 50,000 sq. ft. These approximately 200 leases require approximately $55 million in annual lease expense for the Debtors. Per the First Day Declaration, the Company is obligated to make approximately $166.7 million of future payments to landlords under its unexpired leases — implying a ~3.03 years remaining tail and $275K simple average rent per store.

That short tail is what makes the § 502(b)(6) economics distinctive. The cap is the greater of (a) one year's rent or (b) the rent reserved for 15% of the remaining lease term (the 15% measures time, with the resulting period capped at three years), plus prepetition rent arrears. At portfolio averages, 15% × 3 years equals 0.45 years of rent (~$125K), below the one-year floor (~$275K) — so the one-year cap controls for nearly every store, and the 15% formula does not bind until tails exceed ~6.67 years. Rejecting 50 stores illustratively yields a capped claim of ~$13.8M against $41.7M of contractual exposure (~$27.9M of estate savings); the portfolio-wide $111M spread between $166.7M of contractual obligations and the ~$55M cap ceiling is, in effect, "free deleveraging" for the Debtors.

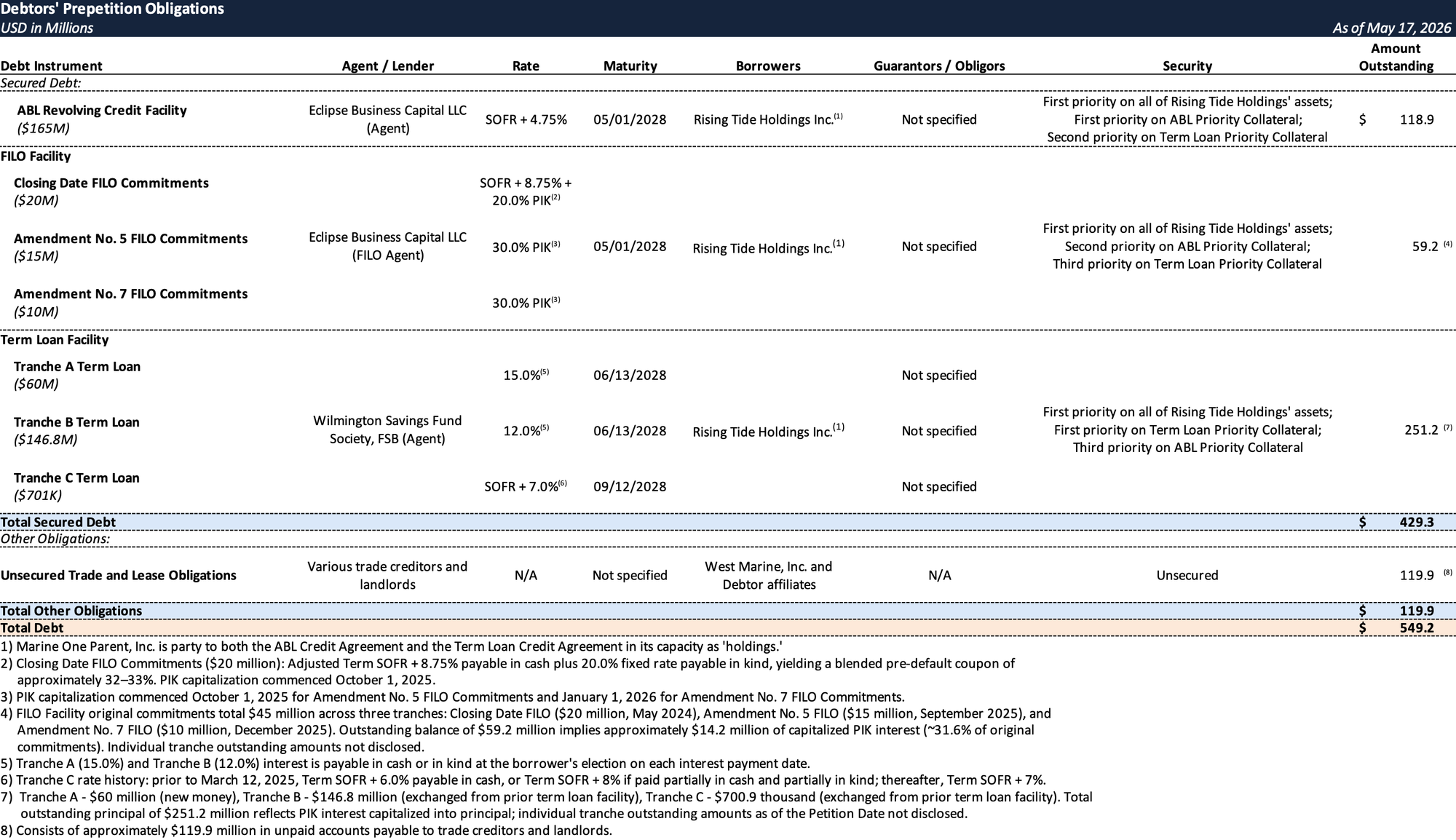

Prepetition Obligations

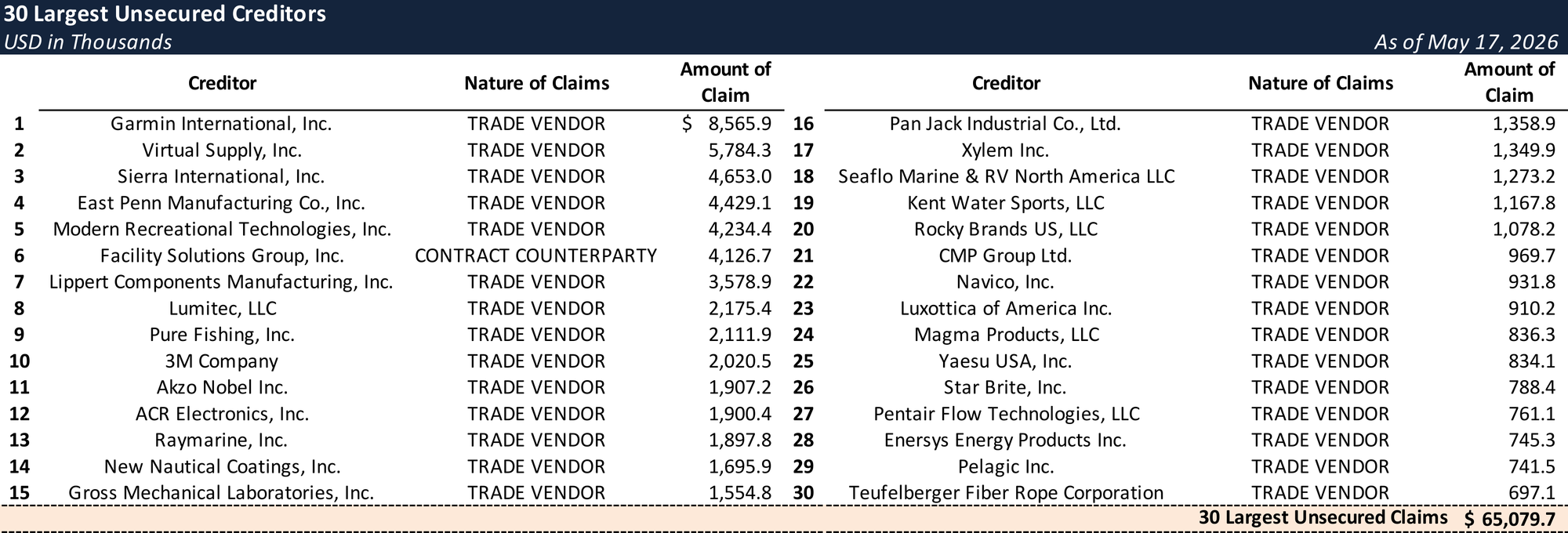

Top Unsecured Claims

Events Leading to Bankruptcy

The Demand Cycle and 2023 Out-of-Court Recapitalizations

West Marine's distress traces a multi-year decline cycle following the pandemic peak. The Company expanded into lifestyle and discretionary categories (apparel, footwear, accessories, and water toys) to meet increased demand during COVID, only to realize that the spike was temporary. In the subsequent years following the pandemic, supply chain disruptions, coupled with underperforming sales, increased costs, inflationary pressures, and long-term leases in undesirable locations resulted in strained liquidity.

The Company underwent two restructuring transactions in March and September 2023. These consensual recapitalizations — supported by 100% of first and second lien lenders and equity sponsor L Catterton in March 2023, and by 100% of funded-debt holders and equity sponsor L Catterton in September 2023 — equitized ~$660M and injected ~$275M of new capital (~$125M in new capital from the September 2023 transaction, and ~$150M in new money from the March 2023 transaction), but proved insufficient. The Company continued to face internal and external headwinds which ultimately led to underperformance compared to its business plan, and several macroeconomic factors that plagued the Company prior to the 2023 recapitalization transactions have lingered into 2026.

Weather-Driven Revenue Headwinds

Erratic and increasingly severe weather patterns have meaningfully undermined West Marine's core business, which is inherently weather-dependent as the business is tied to the number of days customers can use their vessels. In recent years, hurricanes, tropical storms, prolonged heat advisories, and unseasonal cold have reduced usable boating days across key markets, driving down new boat sales and demand for boating-related products and accessories, as well as maintenance and repairs due to less wear-and-tear on vessels as a result of fewer boating days. These disruptions have been particularly damaging because extreme weather disruptions often strike hardest during the peak summer selling season — the period in which the Company is most dependent on the ability to generate the cash flow necessary to fund its operations throughout the rest of the year.

Macroeconomic Volatility

Post-COVID consumer behavior has weighed heavily on West Marine's retail and eCommerce sales across multiple fronts. Economic uncertainty, inflation, and reduced consumer confidence have led consumers to prioritize essential expenses and pull back on non-essential purchases, directly reducing demand for boating accessories and lifestyle recreation products. Compounding this, the pandemic-era boating boom saw many customers make significant upfront investments in discretionary accessories and recreational equipment, meaning those same customers now typically only purchase maintenance-level boat supplies. In 2025, retail sales for new powerboat units were down approximately 8% to 10% on average, reflecting the broader contraction in the sector.

Beyond consumer spending trends, the boating, marine, and outdoor recreation sector continues to face structural headwinds in 2026. Significantly elevated diesel prices, persistent inflationary conditions, and global supply chain disruptions have created an adverse operating backdrop. The volatile tariff environment has added further pressure — the imposition of reciprocal tariffs, despite some recent easing, has increased the cost of imported goods across a broad range of countries, compressing margins and creating a challenging and uncertain operating environment for the Debtors.

Overexpanded Retail Portfolio

The Company's approximately 200-store retail network became a significant financial burden as declining consumer spending made it increasingly difficult for stores to cover their lease and operating costs. Many locations carry unfavorable leases negotiated under better economic conditions, with limited early termination flexibility, leaving the Debtors with little ability to reduce their footprint outside of a court-supervised process. Fixed costs including rent — which alone exceeds $50 million annually — have consistently consumed a disproportionate share of operating cash flow, eroding margins and crowding out investment in operational improvements.

Operational Inefficiencies

When Paulee Day joined West Marine in 2022, in-stock levels were in the high 80% range — suboptimal for retail — driven largely by inefficiencies at its largest distribution center. Stale inventory tracking technology and lack of human infrastructure created communication breakdowns across the business, resulting in mismatches between online orders and actual stock availability, as well as greater lag times in getting products from the distribution center to store shelves.

A new inventory replenishment system implemented mid-2022 was still maturing when post-COVID demand subsided, leaving the Debtors continuing to purchase bloated product assortments without proper lifecycle management. This resulted in excess and duplicative inventory accumulating across all categories. The pandemic-era demand surge had led retailers across the marine industry to dramatically overbuy product in discretionary categories — precisely those most affected by the subsequent pullback in consumer spending — leaving the Company sitting on elevated inventory levels it cannot simply sell through, further eroding profitability.

While management made some progress improving distribution center operations following the 2023 transactions, these efforts were insufficient to overcome the combination of macroeconomic headwinds and an overleveraged balance sheet.

Special Committee Investigation

On April 13, 2026, the Company established Special Committees of the boards of directors of Marine One Parent, Inc. and each of its subsidiaries, comprised of existing disinterested directors Matthew Kahn and Hugh Charvat. The Special Committees were delegated binding authority to: (a) investigate and determine whether a conflict of interest exists or is reasonably likely to exist between the Debtors, on the one hand, and any of the Debtors' current or former managers, officers, committee members, direct and indirect equity holders, successors, assigns, subsidiaries, creditors, or affiliates, among others, on the other hand — collectively defined as "Conflict Matters"; and (b) take any action with respect to any Conflicts Matters, including the investigation, release, or settlement of potential claims or causes of action and make any decision regarding all or part of any transaction that constitutes (in whole or in part) a Conflict Matter.

Prior to the Petition Date, with the assistance of the Company's proposed co-counsel and conflicts counsel YCST, the Special Committees began an initial assessment of (a) the existence of any potential claims or causes of action the Debtors may hold relating to insiders and other affiliated entities, and (b) whether the Debtors should retain, release, or seek to settle any such potential claims or causes of action (the "Independent Investigation"). Since their appointment, the Special Committees have held meetings with advisors to analyze and discuss potential Conflict Matters and the facts and circumstances surrounding potential claims and causes of action. As of the Petition Date, the Independent Investigation remains ongoing, and the Debtor releases contemplated in the RSA remain subject to its outcome.

The Restructuring Support Agreement

On May 17, 2026, the Company entered into a Restructuring Support Agreement with FILO Lenders holding 100% of outstanding FILO Claims, Term Loan Lenders holding 96.2% of outstanding Term Loan Claims, and Equity Holders holding 93.9% of outstanding Interests in West Marine, which contemplates a dual-track restructuring under which the Debtors shall pursue a Recapitalization Transaction — equitizing approximately $251.2 million of Term Loan Claims (Allowed in that aggregate principal amount) into 100% of the New Equity Interests, subject to dilution by the Management Incentive Plan (MIP), with Prepetition ABL Claims ($118.9 million principal) and Prepetition FILO Claims ($59.2 million principal) each either paid in full in cash or converted dollar-for-dollar into loans under, respectively, a new $135 million Exit ABL Facility and a new Exit Term Loan Facility — unless they determine, with the consent of the Required Consenting Term Loan Lenders, to pursue a Sale Transaction followed by a wind-down of the Debtors' estates pursuant to the Plan.

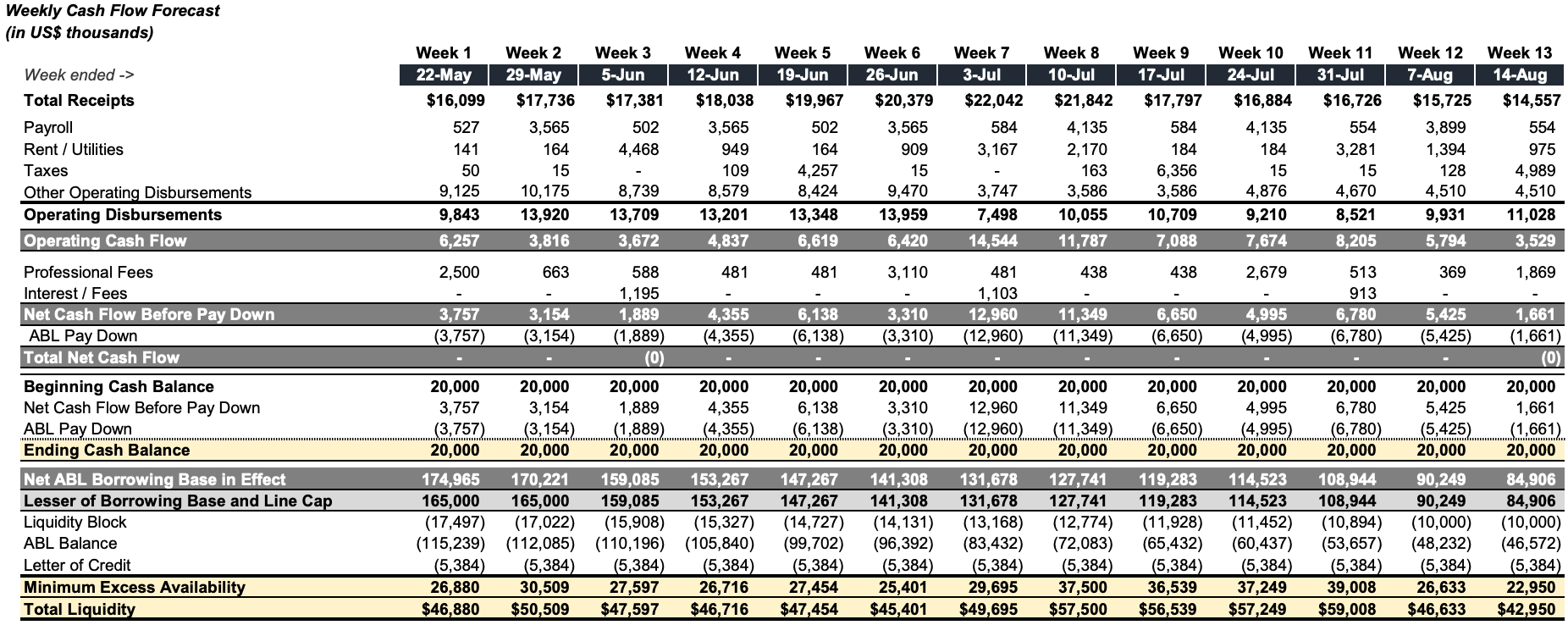

Cash Collateral

The Debtors intend to use cash collateral in lieu of a priming DIP. The 13-week budget maintains a $20M weekly ending cash floor, with any consolidated cash in excess of $20M (excluding the Funded Reserve Account) swept weekly to Eclipse as a mandatory Excess Cash prepayment, taking ABL outstanding from ~$115M at Week 1 to ~$47M by Week 13. Adequate protection payments are asymmetric across the secured debt stack: ABL lenders receive current cash pay at SOFR + 4.75% (approximately $1.0-1.1M per month), while Term Loan lenders accrue adequate-protection interest entirely as PIK, and FILO lenders receive current cash payments or payment-in-kind, which is expected to build the aggregate funded secured claim by approximately $10-15M to $440-450M by the Plan Effective Date.

The post-trigger professional fee carve-out is set at $500K. Cash collateral is subject to a 15% rolling four-week variance covenant, breach of which constitutes a Cash Collateral Termination Event, waivable without Court approval by the Prepetition Agents at the direction of the requisite Prepetition Lenders.

Below is the Company's 13-week cash flow forecast:

First-Day Relief

The Debtors are seeking first-day relief across several operational areas. On the trade side, the Debtors seek authorization to pay up to $33.45M in trade claims on a final basis and $20.7M on an interim basis, subject to a customary trade terms clawback. Customer program relief covers $30.2M in outstanding gift card face value subject to the §507(a)(7) $3,800 per-consumer priority cap, with the program extending to approximately 900,000 rewards members and 40,000 Pro members. The Wages Motion seeks approximately $9.66M in prepetition relief on account of employee compensation and benefits (including $3.1M of unpaid workers' compensation obligations). Separately, the motion also asks the Court to authorize the Debtors to maintain a $4.17M letter of credit issued by The Travelers Indemnity Company in connection with the Workers' Compensation Insurance Policy; the motion also footnote-discloses prepetition retention bonuses paid to certain insider and non-insider Crew Members, though no court relief is being sought with respect to those payments. The Debtors additionally seek to protect $194.6M in NOLs and $189.6M in §163(j) interest expense carryforwards through a 4.5% substantial shareholder ownership threshold. First Day Relief also covers the continued operation of 49 bank accounts.

Bidding Procedures and the Sale Toggle

The Bidding Procedures Motion (Docket 49) launches a marketing process with no stalking horse designated at filing; the Debtors are authorized but not obligated to select one or more stalking horse bidders during the process. Bid protections, if subsequently awarded to a named stalking horse, are capped at 3% of the cash purchase price and are junior to ABL and Term Loan §507(b) superpriority claims. The bid deadline is June 26 at 5:00 p.m. ET, with an auction set for June 29, a sale objection deadline of June 30, a cure objection deadline of July 8, and a sale hearing on July 30, noting that Exhibit 1 to the Bidding Procedures Order reflects July 29, 2026 for the Sale Hearing in both its key dates table and Section 18, while the motion body and Order text consistently state July 30, 2026 — a discrepancy that appears to be a drafting error in Exhibit 1. A 10% cash deposit is required of all qualified bidders.

Credit bidding rights are preserved for all Secured Parties with valid and perfected liens, including Eclipse (as ABL and FILO Agent) and Wilmington Savings Fund Society, FSB (as Term Loan Agent). A qualified credit bid must include a cash component sufficient to pay in full all claims secured by a lien senior to the credit bidder's claim, as well as projected distributions under the Plan and the Wind-Down Amount.

The 95-Day Calendar

- May 17 — Petition.

- May 18 — Plan (Doc. 46), DS (Doc. 47), Solicitation (Doc. 48), Bidding Procedures (Dkt. 49), Bar Date (Dkt. 50); Joint Admin entered.

- May 19 — First Day Hearing.

- June 1 — Conditional DS Objection Deadline.

- June 2 — Final Order objection deadline for all First Day Motions (including Critical Vendors).

- June 4 — Voting Record Date.

- June 11 — Conditional DS Approval; remaining First Day Finals.

- June 18 — Solicitation Commencement.

- June 21 — RSA Day +35 (Final CC outside-date; Investigation conclusion).

- June 26 — Bid Deadline.

- June 29 — Auction (if any).

- July 8 — Cure Objection.

- July 10 — Voting Claims Objection.

- July 13 — Plan Supplement.

- July 16 — Exit ABL commitments.

- July 20, 4:00 p.m. ET — Voting + Opt-In/Opt-Out + Plan/DS Objection.

- July 27 — Confirmation Brief + Voting Report.

- July 30 — Combined Hearing (DS + Confirmation + Sale; six days before the RSA's August 5 Confirmation Order milestone / 80 days from the Petition Date).

- August 20 — Target Effective Date.

Failure of any RSA Milestone is an enumerated termination event under § 11.01(i); milestones may be extended by written agreement of both the Debtors and the Required Consenting Stakeholders (email by counsel sufficient), and are deemed automatically extended to the extent the extension results from Bankruptcy Court scheduling issues or a Bankruptcy Court order setting the date.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.