Case Summary: QVC Group Chapter 11

QVC Group filed Chapter 11 to deleverage a capital structure tied to declining linear-TV cash flows, after cord-cutting, tariffs, covenant breach, and looming RCF maturity drove a prepack canceling $6.5B of prepetition debt amid preferred-equity litigation over a $400M intercompany settlement.

Reflects updates through May 11, 2026. Also available as slides HERE.

Business Description

Headquartered in West Chester, PA, QVC Group, Inc. ("QVC Group" or "QVCG," f/k/a Qurate Retail, Inc.), along with its Debtor⁽¹⁾ and non-Debtor affiliates (collectively, the "Company"), is a global live social shopping company that curates and sells consumer merchandise through video-driven commerce across linear television, streaming, e-commerce, mobile, and social platforms.

- Through its flagship brands—QVC, HSN, and the Cornerstone brands (Ballard Designs, Frontgate, Garnet Hill, and Grandin Road)—the Company reaches more than 200 million households per day across 15 television channels and engages more than 12 million customers through QVC+ and HSN+ streaming plus Facebook, Instagram, TikTok, YouTube, and mobile apps.

- QVC, Inc. ships approximately 182 million units annually from nine global distribution centers; Cornerstone separately operates four fulfillment centers serving its catalog, e-commerce, and retail business. The business employs approximately 15,800 people across seven countries.

The Company reaches customers through three reportable segments—QxH, QVC International, and Cornerstone Brands ("Cornerstone" or "CBI"):

- QxH: The combined U.S. QVC and HSN platform; FY 2025 net revenue of approximately $5.94 billion (~64% of consolidated), generating approximately $517 million of Adjusted OIBDA—down from $765 million in FY 2024 (QVC Group 2025 10-K).

- QVC International: Operations across Germany, Austria, Japan, the U.K., Ireland, and Italy; FY 2025 net revenue of approximately $2.36 billion (~26% of consolidated), generating approximately $293 million of Adjusted OIBDA—down from $333 million in FY 2024 (QVC Group 2025 10-K).

- Cornerstone Brands: Four home-and-apparel brands sold through e-commerce, catalogs, and outlet stores; FY 2025 net revenue of approximately $937 million (~10% of consolidated), generating approximately $16 million of Adjusted OIBDA—down sharply from $36 million in FY 2024 (QVC Group 2025 10-K).

Recent Financial Performance

- FY 2025 consolidated net revenue of $9.23 billion declined for a second consecutive year, down from $10.04 billion in FY 2024 and $10.92 billion in FY 2023 (QVC Group 2025 10-K).

- Results were weighed down by approximately $2.4 billion of non-cash impairment charges recorded in FY 2025—including the write-off of the remaining $1.465 billion of QxH goodwill and $930 million of impairment to the QVC and HSN tradenames—following $902 million of QxH goodwill and $578 million of QVC/HSN tradename impairments taken in FY 2024 (QVC Group 2025 10-K Note 5). As of December 31, 2025, the QxH operating segment goodwill balance was zero, with $1,190 million of indefinite-lived tradenames remaining (QVC Group 2025 10-K, Critical Audit Matter — KPMG LLP).

- Digital platforms represented 66.9% of QxH revenue in FY 2025 (up from 61.8% in FY 2023) (QVC Group 2025 10-K), and approximately 91% of worldwide shipped sales came from repeat customers (Doc. 4 ¶2).

- Consolidated available liquidity stood at approximately $1.71 billion as of April 10, 2026—$195 million at QVCG, $86 million at LINTA, $1.35 billion at QVC, Inc. and subsidiaries (of which $335 million is held at QVC International), and $74 million at CBI (Doc. 4 ¶37).

QVC Group, Inc. and certain affiliates filed for Chapter 11 protection on April 16, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Southern District of Texas, reporting $1 billion to $10 billion in both assets and liabilities.

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

Origins and the Liberty Era

The Company's corporate lineage runs from the 1995 Comcast / Tele-Communications, Inc. joint acquisition through Liberty Media's consolidating control in 2003 and the September 2011 split-off that spun the interactive-commerce businesses out as Liberty Interactive Corporation (predecessor to QVCG; not to be confused with Liberty Interactive LLC, the QVCG subsidiary defined herein as "LINTA"). The HSN and QVC roots reach further back—HSN to Lowell Paxson's 1977 AM radio format and 1982 cable launch with Roy Speer; QVC to Joseph Segel's November 1986 inaugural broadcast—but the portfolio took its modern shape through two large acquisitions of the 2015–2017 period, neither of which worked as underwritten.

The Zulily and HSN Acquisitions

In October 2015, Liberty Interactive Corporation (predecessor to QVCG) acquired Zulily for approximately $2.4 billion to expand its flash-sale e-commerce offering. Successive impairments followed; the business was sold on May 24, 2023 to Regent, an investment firm, for $25 million of cash plus up to $375 million of contingent consideration, with QVCG contributing approximately $80 million at closing to retire Zulily's RCF balance (Doc. 14). On December 29, 2017, Liberty Interactive Corporation acquired the remaining approximately 61.8% of HSN it did not already own in an all-stock transaction valuing HSN at $2.6 billion on an enterprise basis ($2.1 billion equity value)—approximately 9.98x fiscal-year EBITDA per S&P Global Market Intelligence. Cumulative QxH goodwill impairment losses reached $5,228 million as of December 31, 2025 (QVC Group 2025 10-K), with additional QxH tradename writedowns recorded in FY 2023, FY 2024, and FY 2025 ($930 million in FY 2025 and $578 million in FY 2024 alone) — together reversing the bulk of the HSN acquisition premium on the balance sheet.

The December 2020 International Restructuring

The December 2020 Restructuring is load-bearing for the current case. A 15-step multi-jurisdiction reorganization formed QVC Global Corporate Holdings, LLC ("QVC Global") and positioned it to retire legacy Liberty-era 3.5% MSI Exchangeables (participating hybrid option note securities due 2031, the "MSI Exchangeables") using Tax Cuts and Jobs Act repatriation mechanics; through a Nineteenth Supplemental Indenture and a payment reimbursement agreement, the restructuring also created a $1.825 billion face LINTA Promissory Note accruing interest at 0.48%—now the largest single item resolved under the Intercompany Settlement (Doc. 4 ¶43; Doc. 14). Earlier in 2020—declared August 21 and distributed September 14—QVCG paid a special dividend that included issuance of 8.0% Series A Cumulative Redeemable Preferred Stock (Nasdaq: QVCGP) with an initial aggregate liquidation preference of approximately $1.3 billion (approximately $1.272 billion face amount outstanding as of the Petition Date) to legacy Qurate Retail common stockholders (Qurate Retail press release, Aug. 21, 2020; Doc. 4).

Management and Standalone Transition (2021–2025)

David L. Rawlinson II, formerly CEO of NielsenIQ, succeeded Mike George as CEO on October 1, 2021, shortly before the December 18, 2021 Rocky Mount fire. On February 21, 2025, QVCG (then Qurate Retail, Inc.) rebranded as QVC Group, Inc. to complete its transition to a standalone public operating entity; beginning in March 2025, QVC executives took over the public-company functions (tax, accounting, investor relations, and reporting) that Liberty Media Corporation ("LMC") had previously provided under the September 23, 2011 Services Agreement. Dr. John C. Malone did not stand for re-election at the 2025 annual meeting following the September 25, 2024 settlement of the Delaware stockholder derivative action Atallah v. Malone; Gregory B. Maffei remains as Chairman. LMC is not a Debtor in the Chapter 11 Cases.

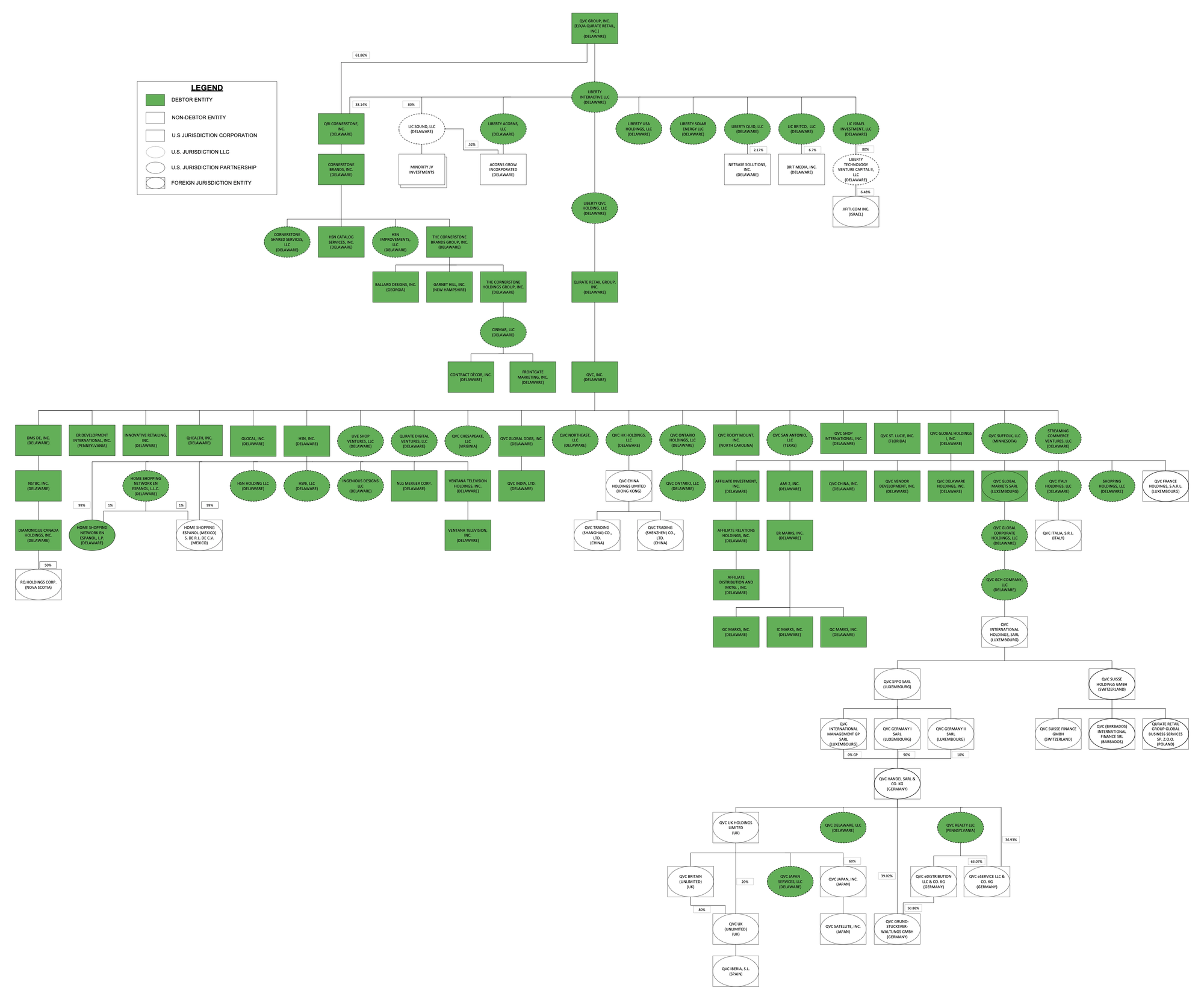

Organizational Structure

At the April 17, 2026 first-day hearing, Debtors' proposed counsel Aparna Yenamandra of Kirkland & Ellis LLP characterized the prepetition organization as "four capital structures in one". Four Key Entities anchor the architecture:

- QVC Group, Inc. (QVCG) — public TopCo. Tickers QVCGA / QVCGB / QVCGP; holds 100% of LINTA and 62% of CBI.

- Liberty Interactive LLC ("LINTA"; called "LI LLC" in the 10-Ks) — intermediate holding company. Carries all unsecured holdco debt; holds the remaining 38% of CBI and, indirectly through Debtor affiliates Qurate Retail Group, Inc. ("QRGI") and Liberty QVC Holding, LLC, the QVC, Inc. operating stack.

- QVC, Inc. — operating company. Carries every dollar of secured funded debt; houses QVC Global Corporate Holdings, LLC ("QVC Global") and the QVC International foreign subsidiaries.

- CBI (QRI Cornerstone, Inc.) — intermediate holder of operating subsidiary Cornerstone Brands, Inc. No funded debt at either tier; on April 1, 2025 QVC notified the RCF Lender Group of its election to remove Cornerstone Brands, Inc. as a borrower under the RCF (Doc. 14).

QVC International and the QVC Japan 60/40 joint venture with Mitsui & Co., Ltd. operate through non-Debtor foreign subsidiaries, and no foreign insolvency proceedings have been filed or are expected to be filed (Doc. 4 ¶29 & fn.4).

Operations Overview

Fulfillment Network

The Company runs a vertically integrated live video commerce platform supported by an asset-light fulfillment network of nine distribution centers and four QVC, Inc. contact centers worldwide. The five U.S. distribution centers — Bethlehem, PA; Suffolk, VA; Florence, SC; Ontario, CA; and Piney Flats, TN — are identified in the QVC, Inc. 2025 10-K Item 2 (Properties), alongside international centers in Chiba, Japan; Hückelhoven and Düsseldorf, Germany; Knowsley and London, U.K.; and Brugherio, Italy. Cornerstone operates four dedicated fulfillment centers and 35 retail and outlet locations. In FY 2025, QVC, Inc. employees handled approximately 70 million customer-service calls and shipped approximately 182 million units globally.

QxH

QxH reaches approximately 88 million U.S. television households across five linear channels (QVC, QVC2, QVC3, HSN, HSN2), but the operating center of gravity has shifted online: digital-platform revenue rose to 66.9% of QxH net sales in FY 2025 from 61.8% in FY 2023, and roughly 90% of new QxH customers now make their first purchase through a digital channel. QxH net revenue declined 10% in FY 2025, attributable to a 10.6% decrease in units shipped and a $53 million decrease in shipping and handling revenue, partially offset by a $156 million decrease in estimated product returns. Separately, FY 2025 cost of goods sold as a percentage of revenue rose to 66.4% from 65.6%, driven in part by "higher product costs driven by tariffs at QxH"; the Disclosure Statement frames the tariff backdrop as having "increased inflationary cost pressures and recessionary fears".

QVC International

QVC International was the portfolio's most resilient segment in FY 2025, with the smallest revenue decline among the three reportable segments. FY 2025 revenue was $2.4 billion and Adjusted OIBDA was $293 million. International e-commerce penetration reached 54% in 2025, compared with a domestic QxH rate of 67%, which the Debtors describe as "room for further international e-commerce penetration in line with domestic performance". Mitsui's 40% noncontrolling interest in QVC Japan is reflected in consolidation.

Cornerstone Brands

Cornerstone has been in steady operational decline—segment Adjusted OIBDA fell from $137 million in FY 2021 to $36 million in FY 2024 and to $16 million in FY 2025 (a 56% YoY drop and ~88% peak-to-trough contraction), and the Q4 2025 quantitative impairment test triggered a $12 million CBI goodwill writedown (QVC Group 2025 10-K). Cornerstone (Cornerstone Brands, Inc.) carries no funded debt and was removed as a Revolving Credit Facility borrower effective on or about April 1, 2025 (Doc. 14); critically, the Plan conditions the CBI Debtors' Debtor Release on Class D3 (CBI general unsecured claims) remaining Unimpaired (Doc. 15), giving the Cornerstone Debtors a structural veto over the upper-box release architecture.

Streaming and Live Social Commerce

The growth story underlying the November 2024 WIN Strategy — which targets $1.5 billion+ run-rate streaming-and-social revenue within three years — centers on TikTok Shop and the QVC+ / HSN+ streaming apps. On April 2, 2025, QVC Group launched "the first U.S. 24/7 live social shopping experience with TikTok Shop" (QVC Group press release, Apr. 2, 2025). Trade-press reporting in April 2026 by Beauty Independent stated that in November 2025 QVC was "the highest-earning store on TikTok Shop, generating over $25 million in revenue and overtaking K-Beauty powerhouse Medicube at $22.46 million." The TikTok channel acquired nearly one million new customers in 2025 and contributed to QVC US growing its total customer file in 2025 for the first time in over four years (QVC Group press release, Apr. 16, 2026). QVC+ / HSN+ reached approximately 1.5 million monthly average users.

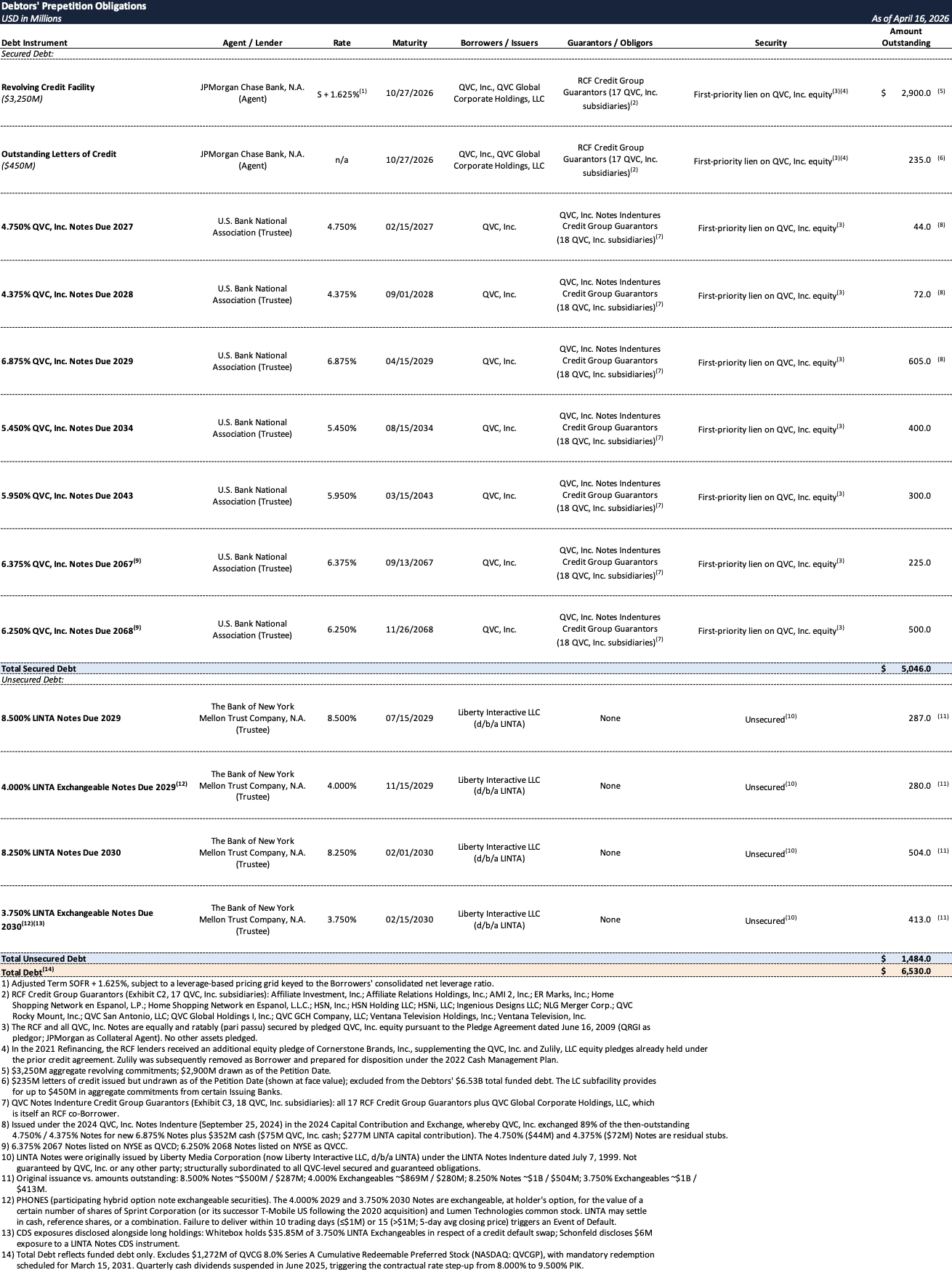

Prepetition Obligations

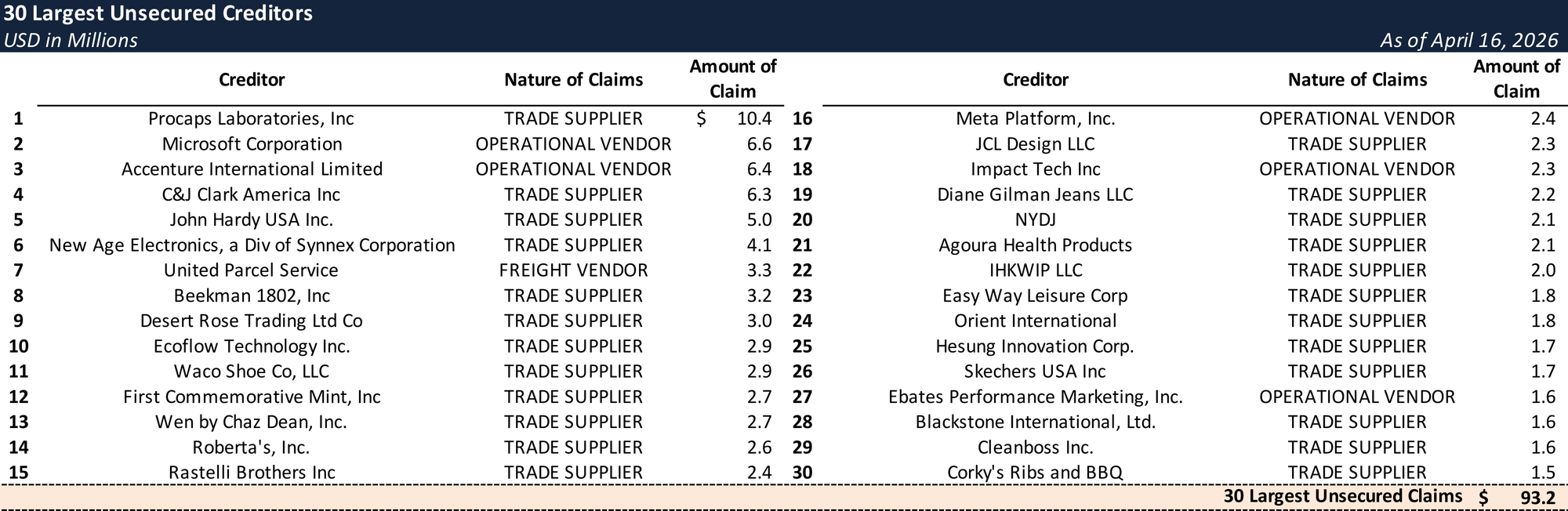

Top Unsecured Claims

Events Leading to Bankruptcy

The Secular Thesis

QVC Group's capital structure—sized against linear-TV cash flows that have contracted materially over the past decade—no longer matches the economics of the business. Management's petition-date materials characterize the filing as a recognition that "QVC Group's debt burden—premised on now-declining cash flows from linear TV—has impaired its ability to invest at the level necessary to fully transition to the new digital and live social shopping age" (Doc. 4 ¶5). Doc. 14 describes sustained cord-cutting and declining television watch-time as core secular pressures.

In 2025, the Company also faced a materially more punitive tariff regime, which together with cord-cutting and elevated leverage was cited as reasons for the May 23, 2025 cash-dividend suspension. QVC, Inc.'s global merchandise mix is concentrated in tariff-exposed categories (Home 41%, Apparel 19%, Beauty 18%, Accessories 11%, Electronics 6%, Jewelry 5% per the QVC, Inc. FY 2025 10-K).

Rocky Mount and the Turnaround

The December 18, 2021 five-alarm fire that destroyed approximately 75% of QVC's 1.5 million-square-foot Rocky Mount, NC fulfillment center—the Company's second-largest distribution center, processing roughly 25%–30% of U.S. volume and serving as the primary hard-goods returns hub—was the largest structure fire in North Carolina history and killed Kevon Ricks, a 21-year-old contractor. A multi-agency investigation concluded in late 2022 that the cause was "undetermined" and that there was no evidence of criminal activity. Management cites an ultimate revenue loss of more than $500 million and a customer-count loss exceeding one million (Doc. 4 ¶39); QVC reached a final insurance settlement in June 2023 and "received $280 million of insurance proceeds" during 2023 (QVC, Inc. 2025 10-K), and the Edgecombe County property was sold in February 2023 for approximately $19 million in net cash proceeds (the gross transaction price was approximately $20.8 million per local property records) after QVC declined to rebuild.

Under CEO Rawlinson, Project Athens (June 2022) ultimately delivered "over $500 million of annual adjusted OIBDA impact" (Doc. 14)—but the program stabilized margin rather than reversed the top-line decline. QVC, Inc.'s consolidated Adjusted OIBDA fell by $288 million in FY 2025 ($248 million decline at QxH and $40 million at QVC International, per QVC, Inc. 2025 10-K MD&A), and Q3 2025 consolidated Adjusted OIBDA was down approximately 32% year-over-year (QVC Group Q3 2025 investor materials). The November 2024 WIN Strategy (Doc. 14) pivoted toward live social shopping, drove the February 2025 QVC Group rebrand and the March 2025 announcement of approximately 900 headcount reductions, and set the $1.5 billion 2027 streaming-and-social-revenue target.

Liability Management and the Credit Profile

The Company pursued sustained out-of-court liability management from 2020 forward. In October 2021, QVC amended its JPMorgan-administered revolving credit facility (the "RCF"), extending the maturity three years to October 27, 2026.

Sale-leasebacks in July 2022 (five U.S. properties, $443 million proceeds) and November 2022 (two properties in Germany and the U.K., $182 million) added roughly $625 million of liquidity (Doc. 4 ¶¶54–55). On December 21, 2022, ahead of potentially approaching credit-document restrictions and with QVCG and LINTA facing ongoing cash needs, QVC, Inc. distributed $800 million up to QVCG, ultimately split (as of December 29, 2022) into $499 million retained at QVCG and $301 million pushed down to LINTA (Doc. 4 ¶48).

- Two days earlier, on December 19, 2022, QVC Group's independent financial advisor Kroll, LLC delivered a solvency opinion and presentation to the QVCG board regarding the transfers (Doc. 4 ¶48 n.6).

The September 2024 "Capital Contribution and Exchange" was a pivotal pre-filing transaction, undertaken to make room for an RCF extension: QVC, Inc. exchanged 89% of its 2027 and 2028 Notes for $605 million of new 6.875% Senior Secured Notes due 2029 plus $352 million of cash consideration, funded $75 million from QVC, Inc. cash and $277 million as a capital contribution from LINTA to QVC, Inc. (Doc. 14). The exchange left approximately $116 million of 2027 and 2028 stubs on their original covenant and collateral package.

- The Preferred Shareholders dispute this characterization, citing QVC, Inc.'s 2025 10-K (Item II-39) which describes the $277 million as "contributed by [QVCG]" via an intermediate transfer to LINTA — implicating a potential QVCG claim against LINTA/QVC that the Intercompany Settlement does not address (Doc. 205 ¶13(d)).

By 2025, the credit profile had deteriorated sharply. S&P Global Ratings downgraded QVC's senior secured rating from 'B-' to 'CCC' on August 26, 2025; per Investing.com's contemporaneous reporting, S&P cited elevated risk that QVC would pursue a distressed debt exchange ahead of an upcoming maturity and characterized the Cornerstone Removal and related steps as likely preparation for a debt exchange or balance sheet restructuring tantamount to default (Investing.com, Aug. 26, 2025; downgrade also reflected in Doc. 14); Moody's followed to Caa3 in October 2025 (Doc. 14). By year-end 2025, QVC had breached the facility's net-leverage covenant ("greater than 4.5 to 1.0" as of December 31, 2025). KPMG's 2025 audit report included a going concern paragraph citing both the upcoming October 27, 2026 maturity and the covenant breach as raising "substantial doubt about the Company's ability to continue as a going concern" (QVC, Inc. 2025 10-K, KPMG Report; Note 1).

The Company has been in dialogue with Evercore Group L.L.C. on capital-structure matters since Q2 2023, engaged Kirkland & Ellis as restructuring counsel in April 2025, and engaged AlixPartners as financial advisor in May 2025.

- Gray Reed serves as local co-counsel to Kirkland & Ellis; Kroll Restructuring Administration LLC is the claims agent.

Governance Build and Intercompany Settlement

Recognizing that any deleveraging would have to resolve the intercompany claims alongside the funded debt, the Debtors seated eight Disinterested Directors across four parallel Governing Bodies between June and November 2025:

- QVCG Special Committee — Carol Flaton and Roger Meltzer (Kobre & Kim LLP); formed June 20, 2025.

- QVC, Inc. board — Paul Keglevic and Jill Frizzley (Katten Muchin Rosenman LLP); constituted September 22, 2025 upon effectiveness of QVC's Amended and Restated Certificate of Incorporation, which terminated QVC's Delaware "close corporation" status under sole shareholder QRGI (Doc. 147; Doc. 14).

- LINTA Board of Managers — Eugene Davis and Thomas Walper (Milbank LLP); seated effective October 1, 2025.

- CBI Special Committee — Jonathan Foster and Michael Zendan (Seward & Kissel LLP); directors appointed effective October 1, 2025, with the Special Committee formally constituted November 2, 2025.

Over five months, the Disinterested Directors and their counsel conducted an independent investigation, supported by AlixPartners forensic accounting covering 2019–2025 and an Evercore solvency analysis covering 2020–2025 (Doc. 14; Doc. 147 ¶¶11–13; Doc. 148 ¶¶9–10). They evaluated ten categories of historical intercompany transactions for fraudulent transfer, preference, illegal dividend, and fiduciary-duty exposure:

- The 2020 Restructuring and LINTA Promissory Note

- The 2021 RCF Refinancing

- The December 2022 $800 million Cash Management Plan

- Approximately $586 million of Post-2022 QVC dividends

- The Intercompany Tax Sharing Agreement

- The Intercompany Shared Services Agreement

- Notes Retirements (June 2022 – February 2025)

- The September 2024 Capital Contribution & Exchange

- Cornerstone's April 1, 2025 removal as an RCF borrower

- The Zulily divestiture

The Plan releases the resulting Causes of Action subject to a Schedule of Retained Causes of Action to be filed with the Plan Supplement, with Section 546(e) safe harbor a common defense thread across these categories.

The resulting Intercompany Settlement is the load-bearing mechanism of the upper-box waterfall:

- QVC–LINTA Claim receives no distributions. QVC, Inc.'s $1.74 billion claim against LINTA (the 2020 LINTA Promissory Note, net of an $85 million December 2021 paydown from its $1.825 billion face) "shall not receive any distributions from the LINTA Debtors or from the LINTA Distributable Cash"; separately, the LINTA Debtors affirmatively "waive any and all Intercompany Claims against the other Debtors" (Doc. 15; Doc. 14).

- QVC–QVCG Settlement Claim Allowed at $400 million (Class A4). QVC, Inc. receives a newly Allowed $400 million unsecured intercompany claim against QVCG, which sweeps essentially all QVCG Distributable Cash—approximately $187 million of balance-sheet cash at the holdco—to the operating company (Doc. 15 Art. III.B.4 (Class A4 treatment); Art. IV.B (Intercompany Settlement); Doc. 14 Liquidation Analysis).

- LINTA Settlement Cash Pool of $23.28 million. Contributed by non-LINTA Debtors and combined with LINTA's $88 million of petition-date cash, this funds the LINTA Notes' projected up-to-approximately-7.5% recovery (Doc. 15 Art. I.A ¶105 (LINTA Settlement Cash Pool) and Art. I.A ¶94 (LINTA Distributable Cash); Doc. 14 Class C3 recovery schedule).

The QVC Disinterested Directors' Statement (Doc. 147) and the QVCG Special Committee's parallel Statement (Doc. 149) quantify the QVCG Claims at approximately $1 billion (low) to $3 billion (high) — comprising approximately $800 million distributed in connection with the 2022 Cash Management Plan (Doc. 147 ¶23; Doc. 149 ¶14 cites approximately $500 million of retained dividends from this transaction), approximately $343 million of Post-2022 Dividends to QVCG, approximately $691 million (Doc. 149 ¶14) to $1.3 billion (Doc. 147 ¶23) of Intercompany Tax Sharing Agreement payments, plus "potential tax indemnification claims" under that agreement — against no "meaningful payments that flowed from QVCG downstream to QVC during the relevant period" (Doc. 149 ¶14). Doc. 147 separately notes that QVCG issued "approximately $450 million in quarterly dividend payments to holders of the QVCG Preferred Equity, which dividend payments were funded in large part with cash from QVC." The $400 million Settlement Claim therefore represents a 13–40% recovery on the face range, and remains conditional on completion of Kobre & Kim's broader Independent Investigation (Doc. 149 ¶¶20, 22).

Cleary Gottlieb Steen & Hamilton LLP (with McKool Smith PC as local co-counsel), representing an ad hoc group of QVCG Preferred holders, flagged at the first-day hearing that the $400 million Settlement Claim "has never been previously disclosed in any of the debtors' SEC files" and that "absent the settlement that they've proposed, there will be actually a meaningful recovery to the preferred" (4/17 Hr'g Tr., Brody). Cleary also signaled an intent to raise the question of an Official Equity Committee "in the first instance with the U.S. trustee's office."

On April 27, 2026, Counsel filed both a Rule 2019 verified statement formally identifying the Preferred Shareholders as Cygnus Capital (1,248,003 QVCGP shares plus 1,800 Class A Common shares), William Pulman (150,000 QVCGP shares), and Kevin Barnes (20,000 QVCGP shares)—an aggregate 1,418,003 preferred shares (~11.1% of the 12.72 million outstanding QVCGP per QVC Group 2025 10-K, ~$141.8 million aggregate liquidation preference at the $100 liquidation price per share)—and confirming the engagement is in connection with "the possible appointment of an official preferred equity committee" (Doc. 138, Ex. A); and an Emergency Motion under Section 1102(a)(2) seeking entry of an order directing appointment of an Official Committee of Preferred Equity Security Holders (Doc. 133).

On April 29, 2026, a second Preferred Shareholder Group—Adam Gui (15,000 QVCGP shares) and Kenneth Grossman (39,331 QVCGP shares), represented by Glenn Agre Bergman & Fuentes LLP with Kane Russell Coleman Logan PC as local co-counsel—filed both a parallel Rule 2019 statement (Doc. 153) and a Joinder to the Emergency Motion (Doc. 156) emphasizing that QVCG holds approximately $195 million of cash, a 62% CBI equity stake, and zero funded debt, such that QVCG "is solvent absent the Intercompany Claim" (Doc. 156). With the Doc. 133 motion plus Glenn Agre's joinder, Section 1102(a)(2) was now an active confirmation-litigation front rather than a hypothetical vector — the May 19 objection deadline and May 26 combined hearing making relief time-sensitive.

On May 1, 2026, Brown Rudnick LLP (Robert J. Stark; Adam Schiffer (Houston)) filed a third § 1102(a)(2) motion (Doc. 169) on behalf of 14 holders aggregating 864,084 QVCGA Common shares (~10.9% of common) and 3,310 QVCGP—seeking a combined common-and-preferred Official Equity Committee and differing from Doc. 133's preferred-only formulation on the question of scope.

At a same-day status conference, Judge Pérez directed the parties to confer on scheduling a contested evidentiary hearing for the § 1102(a)(2) motions — tentatively set for May 8, 2026; the U.S. Trustee (Whitworth) formally took no position. Sussberg signaled the Debtors will put on affirmative evidence supporting the $400 million Settlement Claim—citing "in 2023, $343 million of dividends" and "more than $500 million . . . over the last several years for tax sharing payments . . . over the tax amount that was due"—and conceded that if equity holders prevail at confirmation, they can make a substantial contribution claim, noting that the holding company has $192 million of cash and that he would not object. Sussberg also disclosed that lead Cleary client Cygnus's preferred position grew from approximately 1% in late 2025 to approximately 9% by May 1; Brody's adequate-representation hook—that the QVCG Disinterested Directors "couldn't be bothered to talk to any of the preferred holders" despite reaching all other constituencies—is a central § 1102(a)(2) procedural attack. Judge Pérez signaled the May 26 confirmation hearing remains firm.

On May 8, 2026 — the same day as the scheduled evidentiary hearing — the Preferred Shareholders escalated materially. An Amended Rule 2019 Verified Statement (Doc. 204) consolidated their representation under joint Cleary / Glenn Agre / Kane Russell Coleman Logan counsel and disclosed twelve institutional holders aggregating approximately 2.81 million QVCGP shares (~22.1% of outstanding — roughly double the prior cohorts, now including Highbridge Tactical Credit (two funds, 356,617 shares), Kawa Fund (402,676), Plum Island Partners (241,081), Converium (179,950), Fore Capital (128,272), and Asterozoa (106,308) alongside Cygnus). Concurrently, the same counsel filed an Emergency Motion to Terminate Exclusivity at QVCG only under § 1121(d) (Doc. 205), signaling an Alternative Plan that would fund QVCG's defense of the Alleged Intercompany Claims at no cost to QVCG creditors. The motion attacks the Plan on multiple grounds, including: (i) the Plan transfers QVCG's 62% Cornerstone equity stake to QVC for no consideration beyond the $400 million cash Settlement Claim — a potential best-interests defect given Cornerstone's $74 million cash, no funded debt, and projected $30–42 million Adjusted OIBDA through 2029 (Doc. 205 ¶33); (ii) the Plan cannot satisfy § 1129(a)(10) at QVCG because every class is either deemed unimpaired or deemed to reject, while QVC's $400 million claim is an insider claim under § 101(31)(E) (Doc. 205 ¶32); and (iii) QVCG's Disinterested Directors relied entirely on Evercore — which has advised QVC since Q2 2023 — for solvency analysis (Doc. 205 ¶14). The motion also flags that the Disclosure Statement's own Liquidation Analysis implies approximately $168 million of residual cash for Preferred Shareholders absent the Settlement, before crediting the 62% Cornerstone stake or any non-cash assets (Doc. 205 ¶12, citing Disclosure Statement Ex. D at 9).

RSA

The Restructuring Support Agreement executed on the Petition Date carries at least 75% of RCF claims (Class B3), at least 55% of QVC Notes (Class B4), and at least 45% of LINTA Notes (Class C3)—the descending support stack mirroring descending projected recoveries.

Simpson Thacher's April 30 Rule 2019 (Doc. 168) discloses the RCF Lender Group as twelve members holding $2,916 million of RCF commitments (~89.7% of the $3,250 million facility), led by Strategic Value Partners at $1,042 million (~32% of the facility) and Silver Point Capital at $412 million, with the remaining ten seats held by the prepetition issuing-bank syndicate (JPMorgan, BofA, Citi, BNP at ~$216 million each, Wells Fargo at ~$166 million), plus Scotiabank, PNC, and RBC ($130 million each), Credit Agricole ($25 million), and Société Générale ($20 million). Silver Point alone holds across the full cap stack—every QVC Notes series plus 583,700 QVCG Preferred shares (~$27 million liquidation preference)—making it the only cross-class holder among the RCF Members. Because Class B3 + B4 split 100% of the New QVC Equity pro rata (subject to up to 10% MIP dilution), SVP and Silver Point are on track to be the dominant individual reorganized-equity holders.

The deleveraging cancels the $2.9 billion drawn RCF, the $2.146 billion of QVC Notes, and the $1.485 billion of LINTA Notes, replacing them with $1.275–$1.325 billion of Takeback Debt (senior secured, six-year bullet, no amortization, no call protection, 10.00% per annum coupon on the Takeback Notes; Term SOFR + margin sized to a 10.00% all-in rate at closing on the Takeback Term Loans; 100% par change-of-control put on the Notes version; 2.00% default spread) plus 100% of the QVC New Equity Interests, issued pro rata to B3 and B4 under the "QVC Funded Debt Plan Consideration" formula and subject to dilution of up to 10% for a post-emergence Management Incentive Plan. There is no rights offering, no equity commitment, and no backstop. Class A6 (QVCG Preferred, $1.272 billion face / aggregate liquidation preference exceeding $1.4 billion including accrued and unpaid dividends as of the Petition Date per Doc. 205 ¶4) and Class A7 (QVCG Common) are cancelled for 0% recovery; all general unsecured claims are unimpaired at every Debtor.

An Exit ABL Facility of up to $750 million is being marketed, alongside a contemplated Syndicated Exit Financing that, if consummated by the Effective Date, would replace the Takeback Debt dollar-for-dollar (Doc. 15 Art. IV re Syndicated Exit Financing).

On May 4, 2026, Evercore filed its Valuation Analysis as Exhibit E to the Disclosure Statement (Doc. 196): Net Enterprise Value of $1,850–$2,250 million (midpoint $2,050 million) as of an Assumed Effective Date of August 31, 2026, derived from a blended DCF and trading-multiples analysis. After deducting $1,275 million of pro forma Takeback Debt (potentially $1,325 million if the Exit ABL is consummated without a minimum-utilization requirement) and adding $423 million of emergence cash ($350 million at QVC, Inc. plus $73 million at Cornerstone), Evercore implies an Equity Value for the New QVC Equity Interests of $998–$1,398 million (midpoint $1,198 million), net of the 40% Mitsui minority interest in QVC Japan. Combined with the Takeback Debt, this implies a blended recovery of approximately 45–53% of par on Class B3+B4 secured paper ($2,273M–$2,673M of total consideration against $5,046M of cancelled RCF + QVC Notes par, allocated pro rata under the "QVC Funded Debt Plan Consideration" formula).

DIP Structure

The DIP structure is as distinctive as the collateral package that required it. Because the prepetition collateral is limited to the pledge of QVC, Inc. equity, the Debtors' cash is unencumbered; there is therefore no "use of cash collateral" and no traditional adequate-protection package granted to the prepetition secured lenders.

JPMorgan Chase leads a $300 million senior secured superpriority DIP letter-of-credit facility—no new money, no revolver—with a five-bank issuing syndicate (JPMorgan, Bank of America, BNP Paribas, Wells Fargo, Citibank) that also sat behind the prepetition RCF LCs. The facility is fully cash-collateralized at 105% by a $315 million segregated JPMorgan account and absorbs the RCF-issued prepetition letters of credit, releasing the prepetition issuing-bank syndicate from RCF LC exposure and freeing roughly $49 million of incremental availability (Doc. 48).

Pricing is bank-market rather than capital-markets: 2.50% participation fee, 0.50% commitment fee, 0.75% closing fee, 2.00% default spread. The facility terminates on the earlier of October 16, 2026 (six months post-Petition, 11 days before the RCF stated maturity), the Plan Effective Date, dismissal or conversion, a Section 363 sale, or an Event of Default.

First Day Orders

Judge Pérez granted interim relief on all first-day motions on April 17, 2026, including an All Trade Order capping interim payments at $317.4 million of an estimated $426.1 million of total prepetition trade claims (in the ordinary course, not limited to "critical vendors") (Doc. 69; Doc. 21 ¶10) and an interim NOL trading order designed to preserve "almost $5 billion of tax attributes".

The Section 382 ownership change at emergence is expected to occur and constrain NOL utilization; under the Section 108(b) attribute-reduction waterfall, NOLs are reduced first, but the precise post-emergence NOL balance is undetermined; the Debtors have not yet determined whether the 382(l)(5) Exception will be available or whether to elect out in favor of 382(l)(6) (Doc. 14).

The Combined Disclosure Statement and Confirmation Hearing is set for May 26, 2026, with the Debtors' target Emergence / Effective Date of June 8, 2026 (Doc. 14). The RSA's 90-day plan-effectiveness deadline runs to July 15, 2026; note that the separately defined RSA "Outside Date" is 180 days from the Agreement Effective Date (Doc. 4).

The post-emergence capital structure contemplates $1.275 – $1.325 billion of Takeback Debt against FY 2026E OIBDA of $602 million (Doc. 14 Ex. C), implying gross leverage of approximately 2.1x – 2.2x and net leverage in the ~1.2x area assuming the projected year-end cash balance — a meaningful deleveraging from pre-petition levels.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.