Case Summary: Spanish Broadcasting System Chapter 11

Spanish Broadcasting System filed for Chapter 11 after $310 million of senior secured notes matured unpaid, with a prepackaged plan that proposes to delever its balance sheet by exchanging the outstanding notes for $70 million in new secured notes and substantially all of the reorganized equity.

Reflects updates through May 15, 2026. Also available as slides HERE.

Business Description

Headquartered in Miami, FL, Spanish Broadcasting System, Inc. ("SBS"), along with its Debtor⁽¹⁾ affiliates (collectively, the "Debtors" or the "Company"), is a cross-platform Hispanic media company with operations spanning radio, television, and digital platforms targeting U.S. Hispanic audiences in the United States.

- The Company owns and operates radio stations across the top U.S. Hispanic markets — New York, Los Angeles, Miami, Houston, Chicago, San Francisco, Orlando, Tampa, and Puerto Rico — and runs AIRE Radio Networks (national affiliate platform), MegaTV (broadcast/cable/satellite television), the LaMusica and HitzMaker digital apps, the DigIdea digital marketing arm, and a nationwide live concerts and events franchise.

- Key on-balance-sheet assets include the owned Miami head-office building (~$16.3 million, reflecting a pre-petition negotiated sale price), an FCC license portfolio with aggregate book value of ~$153.8 million, and additional intangibles of ~$32.8 million.

Revenue is overwhelmingly ad-driven — airtime sold to local, national, and network advertisers, supplemented by digital ads on LaMusica and streamed stations, special-events ticketing/licensing, barter (airtime swapped for goods and services), and ancillary income (tower-space rent, subchannel leases, cable/satellite subscriber fees). Net revenue is gross less agency commissions of generally ~15%. The Company's 9M 2025 revenue mix (vs. 9M 2024) was: Local & Digital 70% / 68% (the largest category); National & Network 20% / 22%; Barter 6% / 4%; Special Events 3% / 5%; Other (tower rent, subscriber fees, ancillary) 1% / 2%.

As of the Petition Date, the Company employed 324 people, of whom 286 were full-time and 38 were part-time, with 19 employees unionized or party to collective bargaining agreements or similar labor arrangements. The Debtors operate 17 radio stations, with FCC licenses held through dedicated 'Licensing' subsidiaries (each a co-Debtor); MegaTV's remaining South Florida television operations are also held through Debtor entities. The Puerto Rico television stations WVEO(DT), WTCV(DT), and WVOZ-TV were sold pre-petition in August 2025.

Spanish Broadcasting System, Inc. and certain affiliates filed for Chapter 11 protection on May 11, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the District of Delaware, reporting $100 million to $500 million in both assets and liabilities.

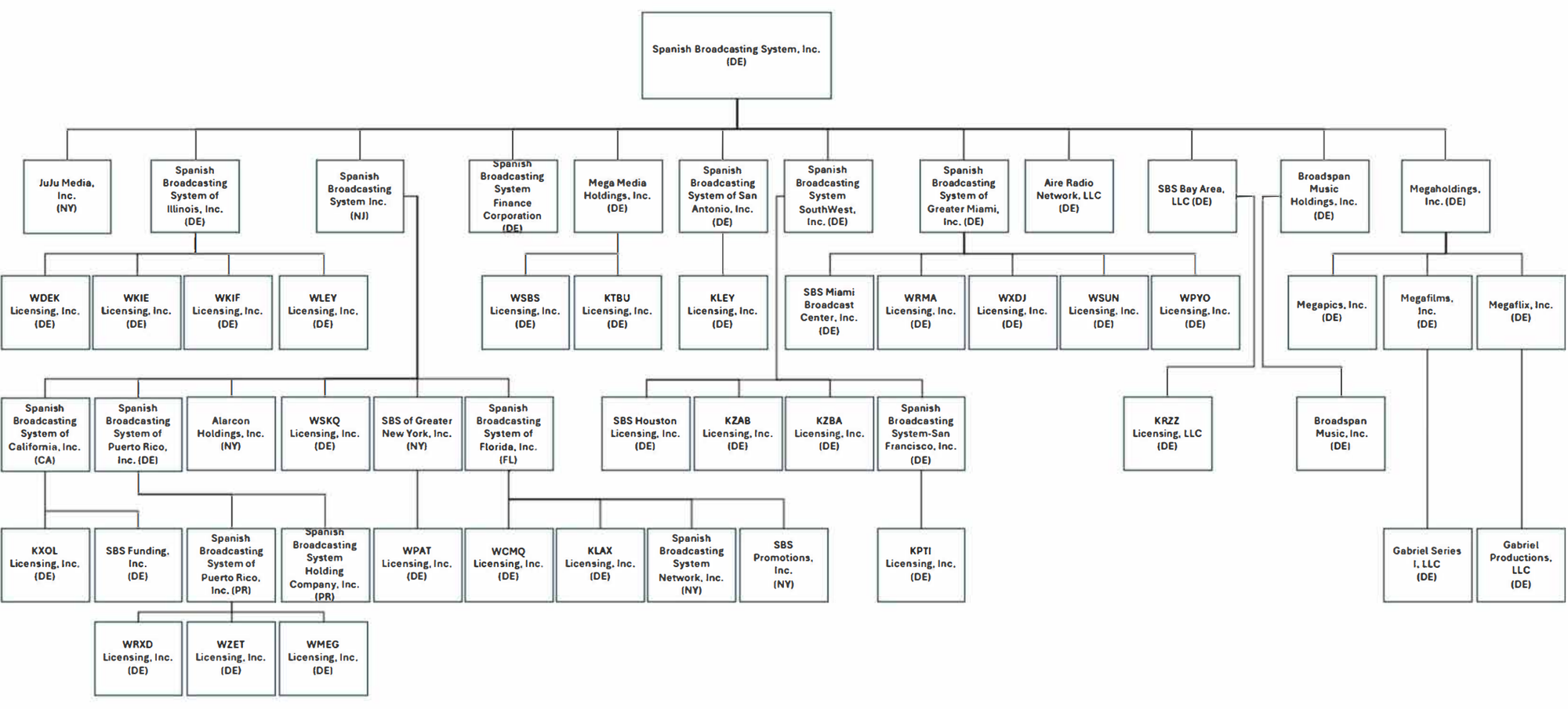

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

Spanish Broadcasting System was founded in 1983 by Pablo Raúl Alarcón Sr. and Raúl Alarcón Jr. as a Spanish-language radio operator and later reincorporated in Delaware in 1994. Throughout the 1980s and 1990s, SBS built its franchise by acquiring radio stations in major U.S. cities including New York, Los Angeles, Chicago, San Francisco, Dallas, and San Antonio; and in the early 2000s consolidating the largest radio group in Puerto Rico and opening a broadcast complex on the island. SBS completed its initial public offering in 1999, after which it operated as an SEC-registered reporting company for two decades.

Beginning in the mid-2000s, the Company diversified beyond terrestrial radio into the adjacent business lines that now sit in separate Debtor sub-chains: it launched MegaTV in 2006 (a Spanish-language television platform housed in the Mega Media Holdings entities), built the AIRE affiliate radio network throughout the 2010s, and rolled out the LaMusica website and the LaMusica and HitzMaker mobile apps, with the digital business operating through JuJu Media, Inc. (a/k/a SBS Interactive). The result is the four-line operating platform — Radio, Television, Internet/Digital, and Live Events — detailed in the Operations Overview below.

The principal capital-markets inflection occurred in 2020, when SBS filed a Certification and Notice of Termination of Registration under Section 12(g) of the Securities Exchange Act of 1934, terminating registration of its securities and suspending its Section 13 and 15(d) periodic-reporting obligations. On February 17, 2021, SBS issued $310 million of 9.75% Senior Secured Notes due 2026. Since deregistration, and with no SEC periodic-reporting obligations, post-2020 public disclosure has been driven primarily by indenture-required reporting under those Notes.

Organizational Structure

Operations Overview

The Debtors operate four complementary business lines — Radio, Television, Internet and Digital Content, and Live Concerts and Events — anchored by a national footprint in the largest U.S. Hispanic markets.

Radio

- The Debtors own and operate 17 radio stations, including three of the top six Spanish-language stations in the United States. Flagship WSKQ is the number-one ranked U.S. station in New York City on an average-listeners-per-quarter-hour basis. The owned-and-operated footprint covers the top U.S. Hispanic markets — Los Angeles, New York, Miami, Houston, Chicago, San Francisco, Orlando, Tampa, and Puerto Rico — with LA and NY representing the first- and second-largest U.S. Hispanic populations and the first- and second-largest U.S. radio markets by advertising revenue.

- The Debtors also operate AIRE Radio Networks, a national Spanish-language affiliate platform with over 250 affiliate stations across 79 U.S. Hispanic markets, covering 94% of the U.S. Hispanic market and reaching 21 million listeners monthly.

Television, Digital, and Live Events

- Television (MegaTV): The Debtors' television stations broadcast under the "MegaTV" brand via owned-and-operated stations and through programming and distribution agreements, including nationally on a subscriber basis. On August 15, 2025, the Company exited the Puerto Rico television market, closing the sale of WVEO(DT), WTCV(DT), and WVOZ-TV and related transmission equipment to Word of God Fellowship (also known as Daystar Television Network) for $5.7 million in cash, recognizing a gain of approximately $2.8 million. Post-sale, MegaTV's owned-and-operated footprint consists of two South Florida stations — WSBS-CD Miami (Class A LPTV) and WSBS-TV Key West (Channel 22).

- Internet and Digital Content: The Debtors operate Spanish and bilingual websites including www.lamusica.com; the LaMusica mobile app, which offers short-form videos, simultaneous live streams of the Debtors' radio stations, and curated playlists; HitzMaker, a new-talent destination for aspiring artists; and DigIdea, the Debtors' pure-play digital marketing department serving brands and the podcast community.

- Live Concerts and Events: Through SBS Entertainment, the Debtors typically produce more than 40 live concerts, events, and activations annually across the contiguous United States and Puerto Rico, drawing more than 130,000 attendees, with revenue generated through ticket sales, sponsorship, licensing, and profit-sharing arrangements tied to the Debtors' radio and digital properties.

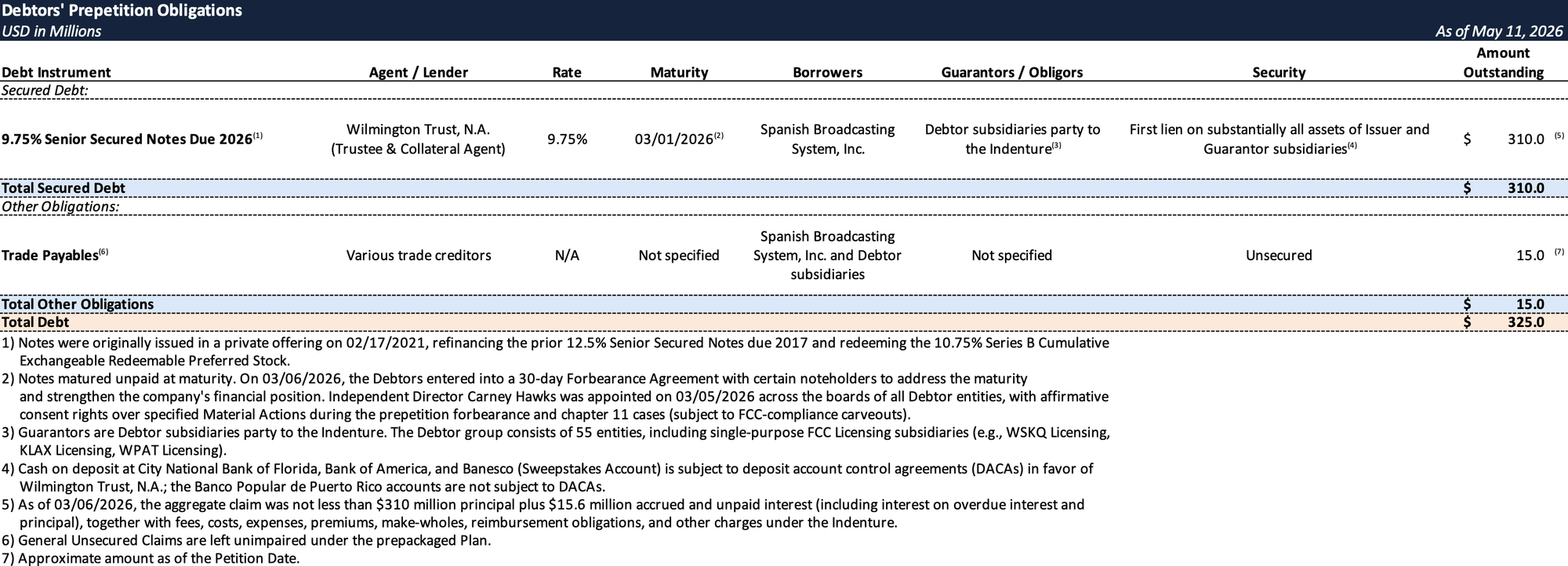

Prepetition Obligations

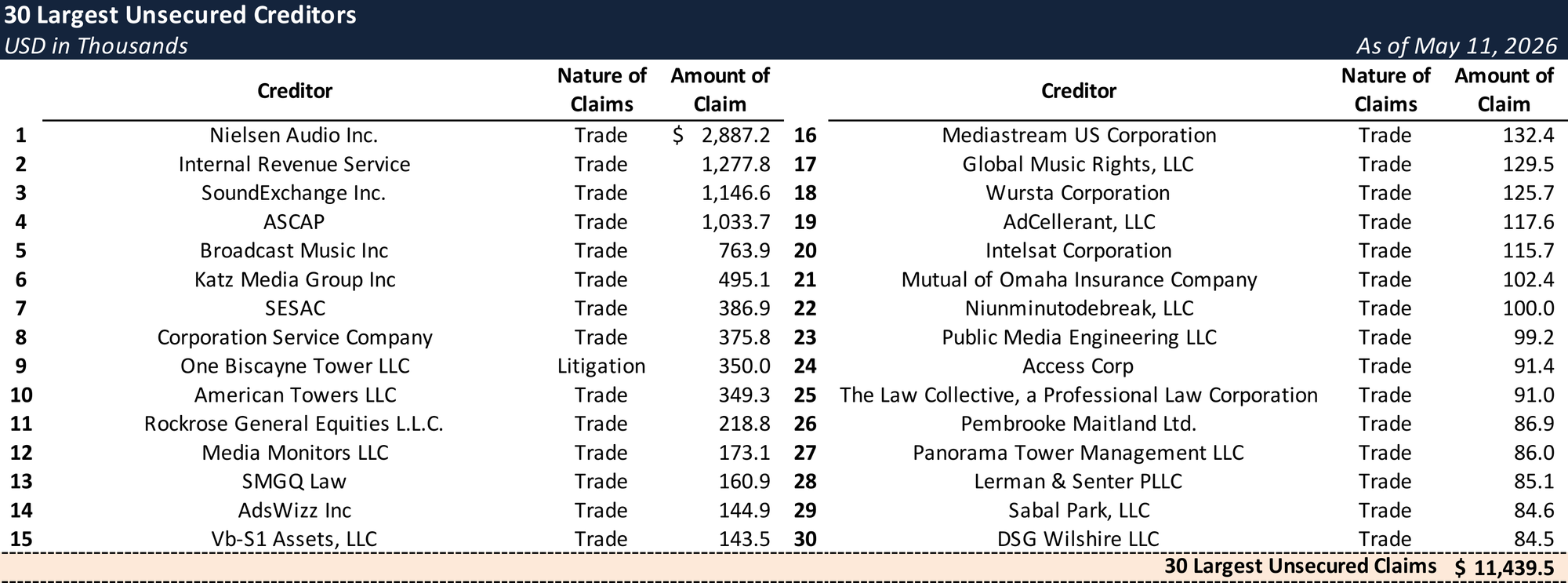

Top Unsecured Claims

Events Leading to Bankruptcy

The Debtors filed on May 11, 2026 (Case No. 26-10708-BLS, D. Del., Hon. Brendan L. Shannon) under a prepackaged plan supported by holders of more than 90% of the funded debt and backstopped by Brigade Capital Management, Bardin Hill Investment Partners (now an indirect subsidiary of UK-domiciled Man Group plc since the October 1, 2025 acquisition closing), and Bayside Capital (the credit affiliate of H.I.G. Capital). The filing was precipitated by the March 1, 2026 maturity of $310 million of 9.75% Senior Secured Notes that the Debtors could not refinance. The Plan delevers the Company to $70 million of new 9.750% Senior Secured Notes due 2030 and equitizes the residual claim into 100% of the New Common Stock (subject to a 10% MIP), leaving trade, employees, and other general unsecured creditors unimpaired.

Industry Backdrop and Operating Headwinds

The Company's revenue base has been on a decline under the well-documented secular decline of linear radio — streaming/podcast audience migration, advertiser follow-on, and rising multi-platform technology and licensing costs. Additional company-specific drags also contributed to top line erosion: the Company's principal markets (NY, FL, CA, IL) have ceased to be swing-state political-ad beneficiaries, and the January 2025 Los Angeles wildfires, alongside broader uncertain market conditions, contributed to a decrease in broadcast advertising and non-cash impairment charges in Los Angeles — the Company's largest U.S. Hispanic radio market. A high prepetition leverage profile and constrained capital markets access limited digital reinvestment. Ahead of the October 27, 2025 ABL maturity, the Debtors prepaid and terminated the $15 million Revolver on October 20, 2025 (shortly after the August 15, 2025 sale of the Puerto Rico TV stations for $5.7 million in cash), leaving the Existing Notes as the sole funded-debt instrument and effectively first-lien across the full collateral package.

Prepetition Restructuring Process

In October 2025, the Company retained Fried, Frank, Harris, Shriver & Jacobson LLP and GLC Advisors & Co., LLC to address the March 1, 2026 Notes maturity; the Ad Hoc Committee of Existing Noteholders organized with Milbank LLP and M3 Advisory Partners, LP. The Notes matured unpaid on March 1, 2026, and subsequently a 30-day Forbearance Agreement was executed on March 6, 2026 (with approximately $15.6 million of accrued and unpaid interest in addition to the $310 million principal). One day before the forbearance, the Debtors appointed Carney Hawks as the sole independent, disinterested director across the boards of all Debtor entities, with affirmative consent rights over specified Material Actions subject to FCC-compliance carveouts. The Debtors added Morris, Nichols, Arsht & Tunnell LLP as Delaware co-counsel and Riveron RTS, LLC (with Riveron Management Services, LLC providing CRO services through Jesse York). On April 3, 2026, the Debtors executed the Restructuring Support Agreement with holders of more than 66.67% of the Existing Notes (rising to more than 90% by the Petition Date), providing for the equitization Plan, a $30 million DIP, and an optional Approved Sale toggle exercisable by the Required Consenting Creditors at any time prior to the Confirmation Hearing (if elected, milestones reset to a 30/45/105/180-day Sale-Pivot timeline, the equitization Plan serves as a back-up bid, and the $10 million delayed-draw DIP tranche automatically unlocks). Section 9.03 establishes a 360-day Outside Date measured from the RSA Effective Date (April 3, 2026), with a 90-day extension if the only remaining impediment is required FCC or other governmental approval; Section 9.03 also separately requires entry of the Confirmation Order within 180 days of the Petition Date.

DIP Financing, Sale Pivot, and Marketing Process

The DIP is a $30 million senior secured super-priority multi-draw term loan provided several-and-not-joint by the three Backstop Lenders and syndicated pro rata to other RSA-electing holders, with Brigade Agency Services LLC as DIP Agent / Collateral Agent and Jefferies Capital Services, LLC as Fronting Lender. Mechanics:

- Tranching: $7M Interim / $13M Final / $10M Delayed Draw — the third tranche conditioned on the written consent of the Backstop Parties (under the RSA) or, alternatively, the occurrence of the Sale Pivot Date.

- Pricing: 9.75% cash coupon, plus a 2.00% default rate; premium stack of 2.50% Backstop / 2.00% Commitment / 2.00% Exit. Backstop Premium is treated as a put premium for U.S. tax; Commitment and Exit Premiums give rise to OID. The Backstop Premium accrues solely to the three Backstop Lenders; the Commitment Premium is syndicated to all participating lenders.

- Roll-up: None — no portion of the $310 million prepetition Notes is rolled up.

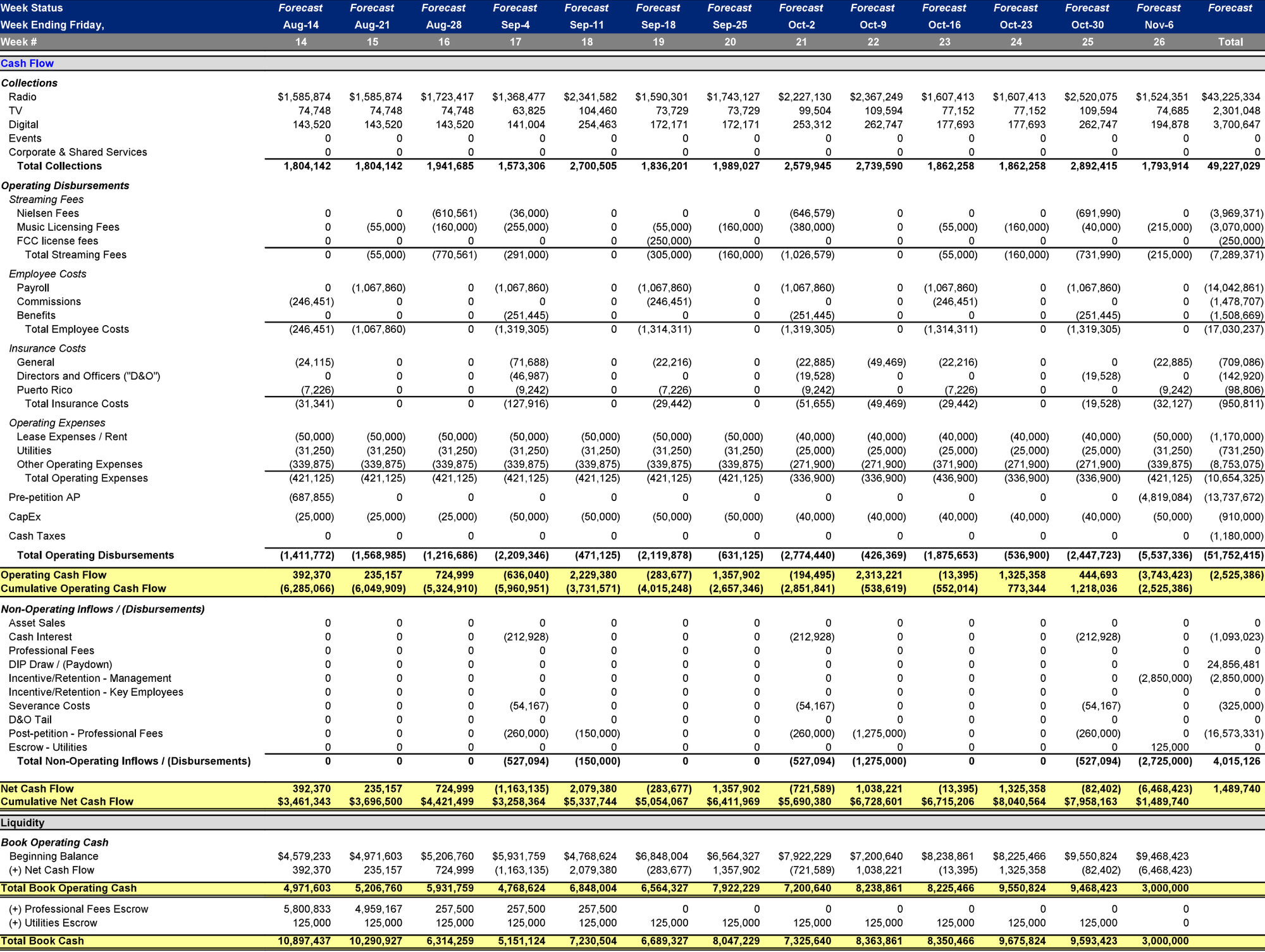

- Maturity: December 31, 2026, with a permissive extension of up to 90 additional days (to as late as March 31, 2027) at the Required Supermajority Lenders' determination/consent if the sole remaining Effective-Date condition is governmental or regulatory approval (i.e., FCC consent to the Transfer of Control).

- Covenants and protections: $3 million minimum liquidity; permitted unfavorable variance of 20% (receipts) and 10% (disbursements) tested 4-week / rolling 2-week; $750,000 Post-Trigger Carve-Out (excluding success fees); $50,000 Investigation Cap and 75-day Challenge Period on stipulated releases; full credit-bid rights for both DIP Agent and Existing Trustee.

- Market-test: GLC contacted 24 third-party potential DIP lenders, yielding one expression of interest (in providing a consensual priming DIP), but the holders of the Existing Notes (i.e., the Ad Hoc Committee) declined to consent to being primed.

The DIP Conversion Election permits the Required DIP Lenders, in their sole discretion, to convert DIP Claims (principal plus all premiums other than accrued interest and expenses, which are paid in cash) into newly issued 9.750% Superpriority Senior Secured Notes due 2030. Under the Disclosure Statement projections (Exhibit E), the post-emergence stack will be approximately $43.1 million of New Secured Notes plus $26.9 million of New Superpriority Secured Notes, with the latter sitting senior to the former pursuant to the New Secured Notes Intercreditor Agreement. The aggregate $70 million New Secured Notes Amount is reduced dollar-for-dollar by any Superpriority issuance, so the DIP economically moves up the takeback stack at Existing Holders' expense.

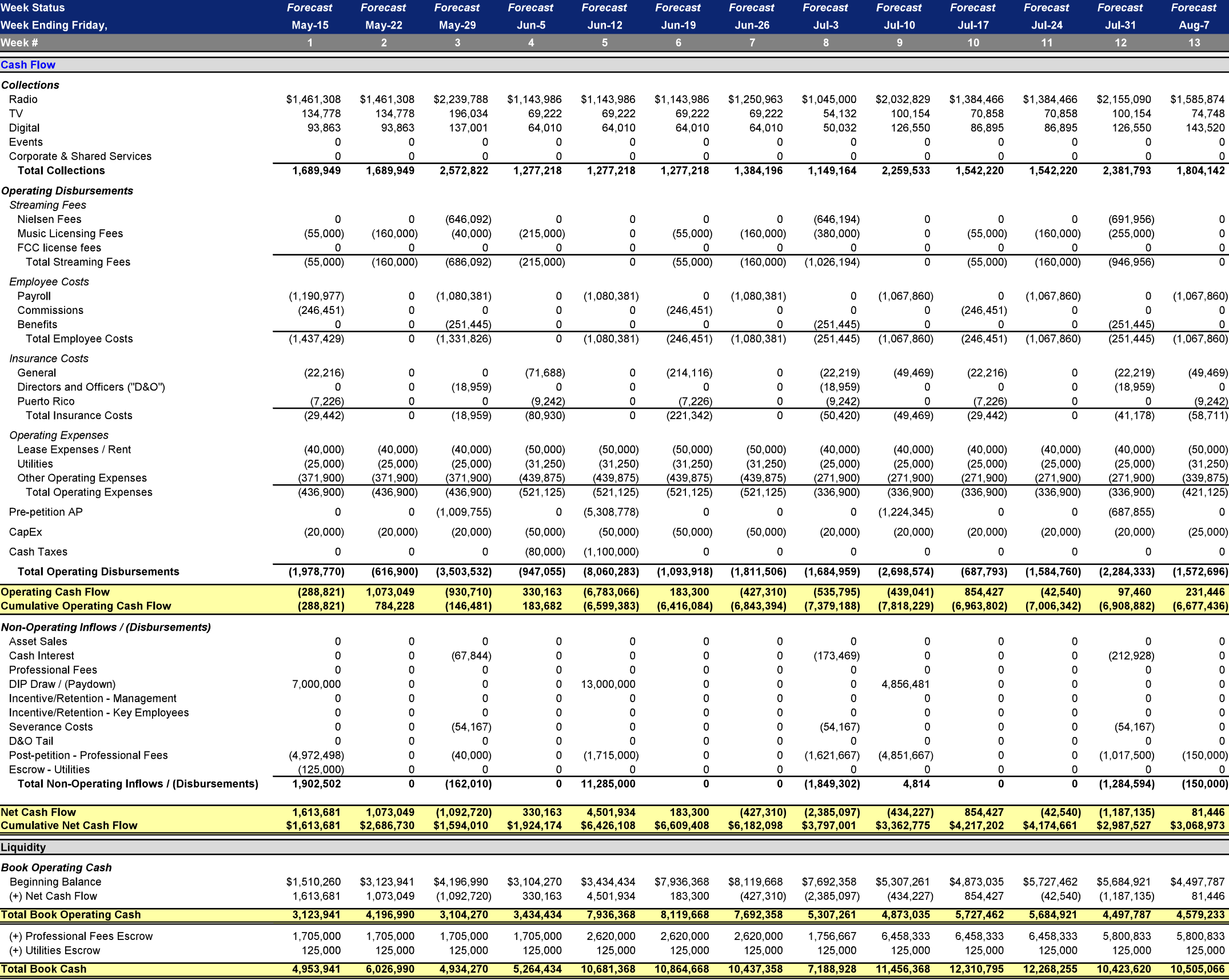

Interim Approved DIP Budget

Plan Treatment, Reorganized Capital Structure, and Recovery Waterfall

The Plan classifies claims into nine Classes plus unclassified DIP, Administrative, and Priority Tax Claims; Class 2 (Existing Notes) is the sole voting class. The Voting Deadline is June 18, 2026; the Debtors target a combined Disclosure Statement Approval and Confirmation Order within 55 days of the Petition Date (Confirmation Hearing week of June 22, 2026), with an Effective Date no later than 180 days after entry of the Confirmation Order — an extended window to accommodate required FCC approval prior to the Transfer of Control.

- Class 2 — Existing Notes (Impaired; voting): Allowed at approximately $310 million principal plus $15.6 million accrued interest as of March 6, 2026. Each holder receives Pro Rata (a) 100% of the $70 million of New Secured Notes (which is reduced dollar-for-dollar by any New Superpriority Secured Notes issued to DIP Lenders if a DIP Conversion Election is made) and (b) 100% of the New Common Stock, subject only to MIP dilution. Disclosure Statement recovery: 29.0%–38.1%, implying combined package value of $96.3M–$126.3M.

- Classes 1, 3, 4 (Other Priority, Other Secured, GUC) — Unimpaired; 100%

- Class 5 (Intercompany Claims) and Class 6 (Intercompany Interests): reinstated, compromised, or cancelled (Class 5) / reinstated for administrative convenience (Class 6), at the Debtors' election with Required Consenting Creditor consent.

- Classes 7–9 (Series C Preferred / Class A and B Common / §510(b)) — Impaired; 0%: Cancelled for no consideration, terminating Raúl Alarcón Jr.'s voting control over 2.34 million Class B shares (10 votes per share) and the Series C preferred.

The take-back paper consists of $70 million of 9.750% Senior Secured Notes due 2030 (4-year tenor, PIK toggle at the Required Consenting Creditors' option, no call protection, first-lien on the full prepetition collateral package plus newly perfected previously unencumbered assets, junior to Superpriority Notes if issued) and, if a Conversion Election is made, Superpriority Notes on the same coupon and maturity. New Common Stock is issued under Bankruptcy Code § 1145 (MIP and other restricted issuances under § 4(a)(2) / Reg D / Rule 701 / Reg S); Reorganized SBS will not be SEC-registered or exchange-listed, will furnish financials privately via data room, and is expressly exempt from Sarbanes-Oxley § 404. The five-member New Board allocates two directors to any >40% holder and one director to any 20%–40% holder, with the CEO sitting ex officio and a "Specified Director" appointed by Bayside Capital while the Bayside Condition is satisfied. Customary tag-along and preemptive rights at a 5% holding threshold; drag-along rights exercisable by holders of a majority of outstanding Common Shares; Board observer seat at 10%; demand registration rights at 20% (with tag-along triggered by transfers of at least 20% of outstanding Common Shares). Information rights are available to all non-competitor Holders via the data room.

Valuation, Liquidation Analysis, and Financial Projections

GLC's Valuation Analysis (Doc. 4, Exhibit D), prepared as of May 4, 2026 for an assumed October 31, 2026 valuation date and applying comparable-companies and DCF methodologies (no precedent transactions, peers, WACC, or multiple range disclosed), estimates Reorganized SBS at $120–$150 million TEV / $53–$83 million equity after deducting $70 million of New Secured Notes and adding $3 million pro forma cash — an implied 6.2x–7.8x EV / FY2027E Adj. EBITDA (5.3x–6.6x on the FY2028E political-cycle peak).

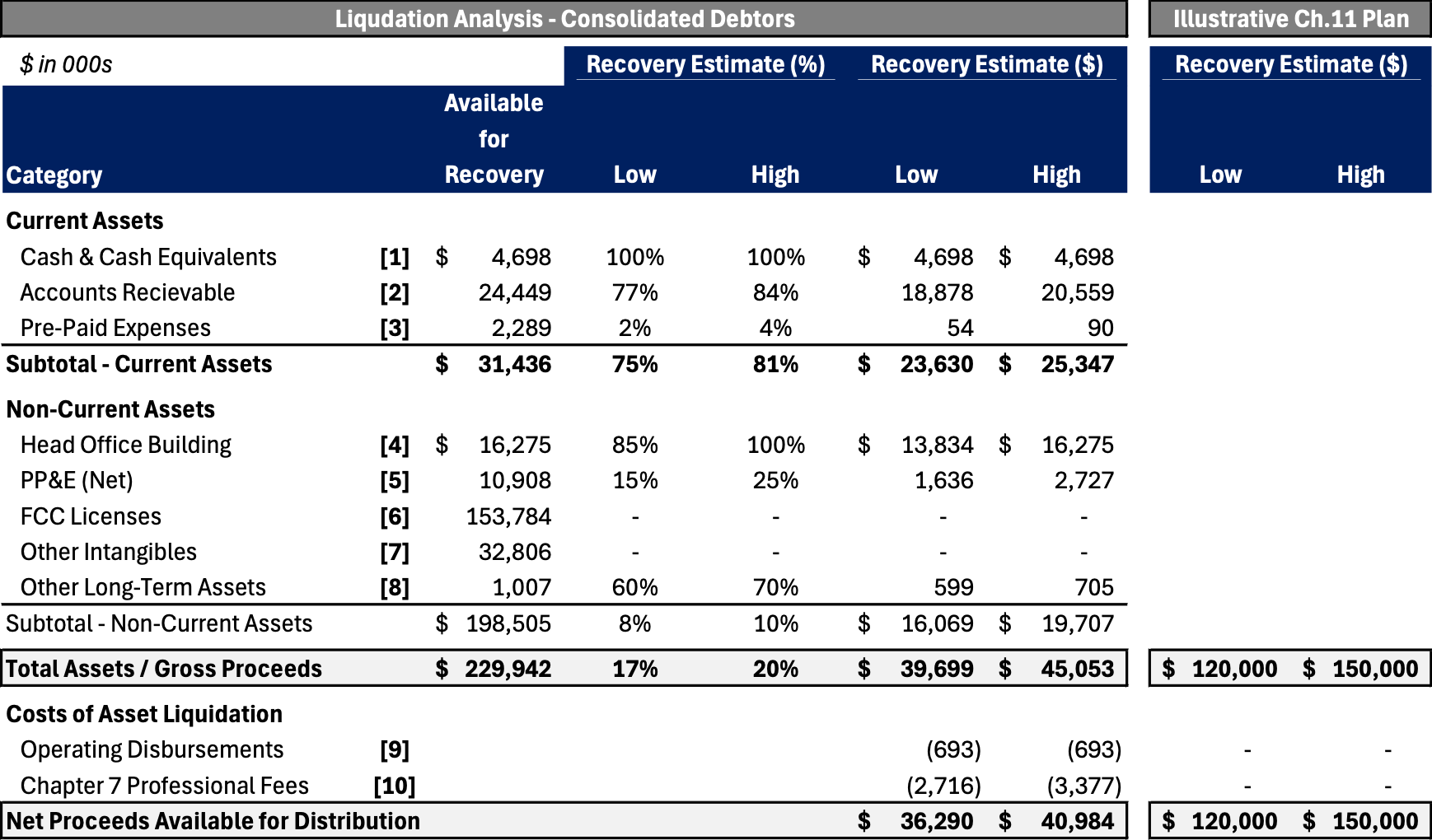

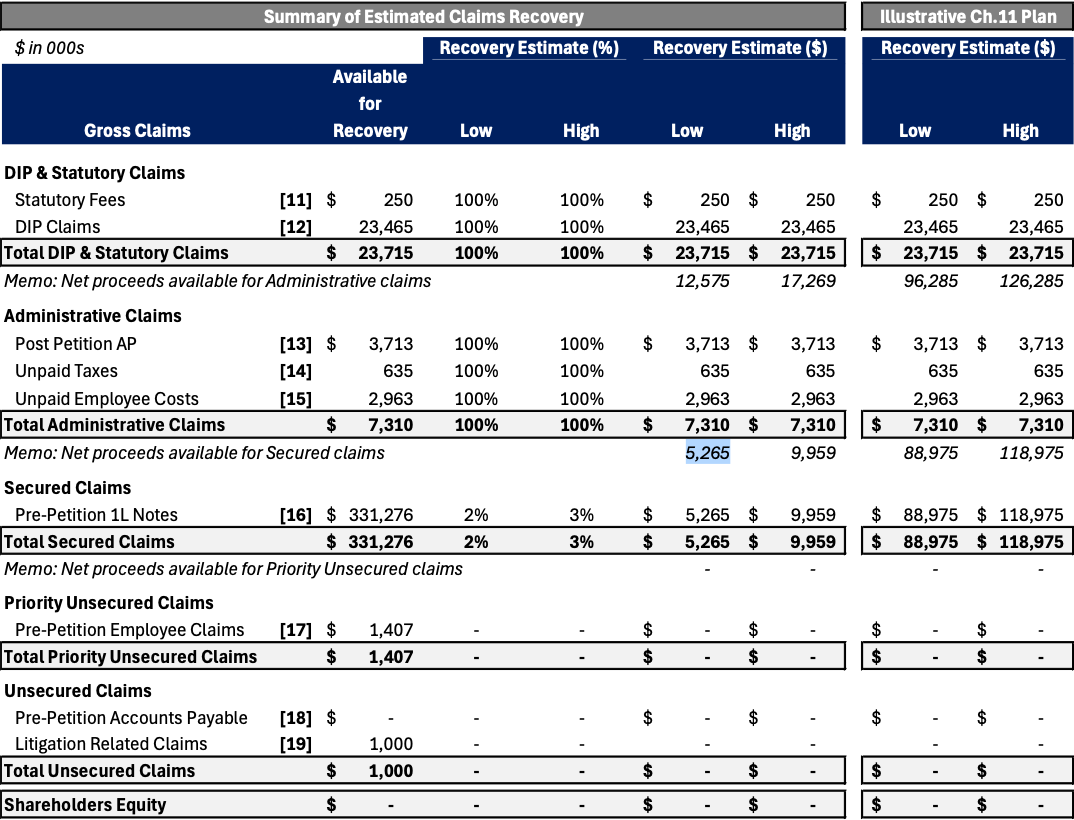

The Liquidation Analysis and Estimated Claims Recovery (Doc. 4, Exhibit C, Riveron; assumed November 6, 2026 conversion, four-month wind-down, consolidated-Debtor basis) yields net proceeds available to the First Lien Notes of $5.3–$10.0 million (FCC licenses recovered at 0% due to forced-sale impairment and ~$70 million tax leakage; headquarters at 85%/100% via a pre-petition negotiated sale; PP&E at 15%/25%; AR at 77%/84%).

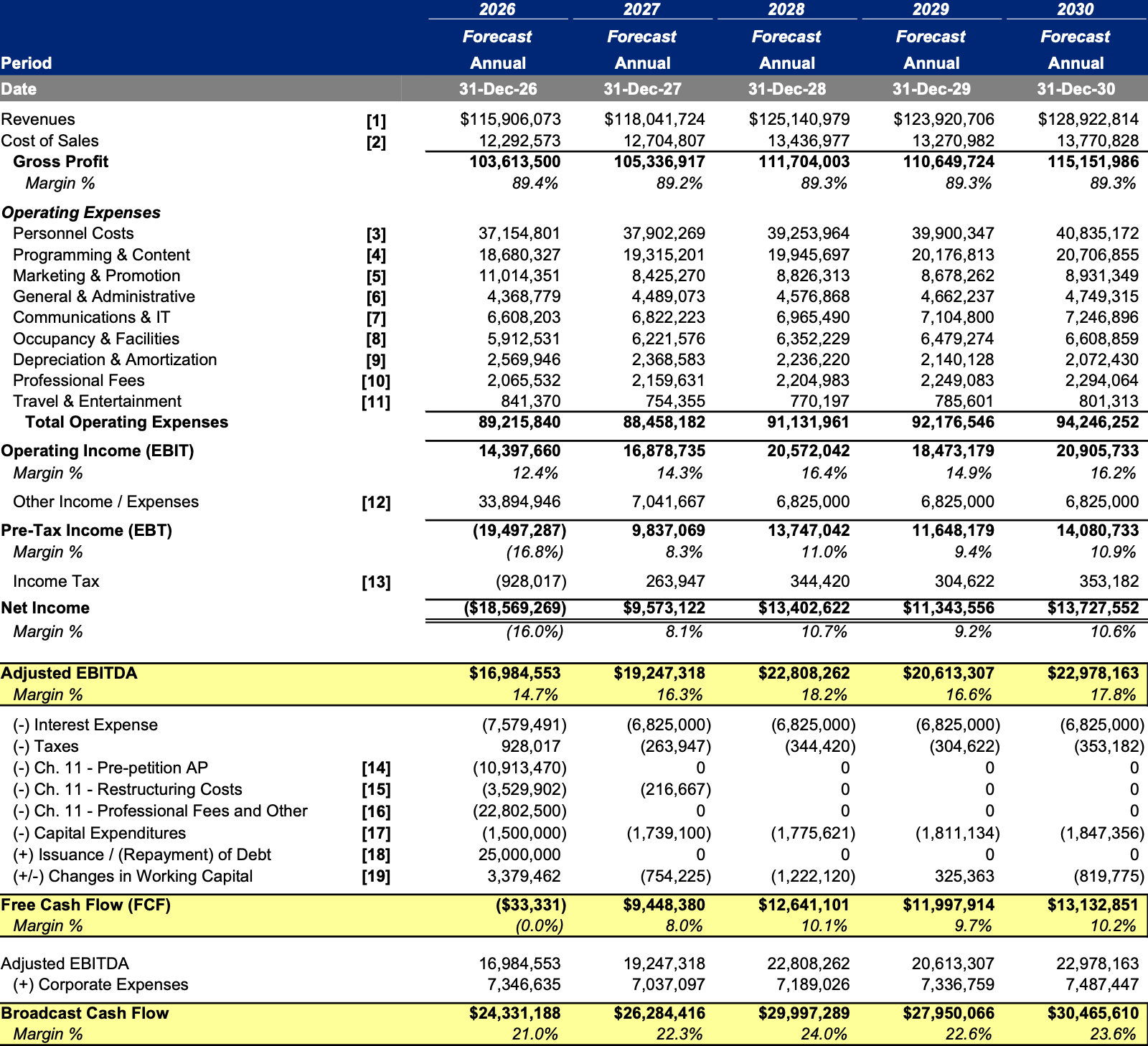

Below is Riveron's bridge and the five-year management projections (Exhibit E).

FY2026 FCF is essentially break-even after $37.2M of one-time bankruptcy-related outflows ($10.9M prepetition AP catch-up, $3.5M restructuring costs, $22.8M chapter 11 professional fees), and is supported by a $25M DIP draw; from FY2027 onward, $9.4–$13.1 million of annual FCF comfortably covers the ~$6.83 million of cash interest on the take-back paper. Steady-state leverage of ~2.9x–3.6x compares against the ~7.7x prepetition multiple. For tax purposes, the equitization is expected to trigger an IRC §382 ownership change (with the choice between the (l)(5) and (l)(6) exceptions deferred); the long-term tax-exempt rate applicable to May 2026 ownership changes is 3.65%. COD income is excluded under §108 at the cost of attribute reduction. NOL/equity trading procedures are in place at Docket 15.

FCC Regulatory Approvals and Comparable Precedents

The Plan Effective Date is conditioned on FCC grant of both (i) the Long Form Application (Schedule 315 transfer of control) and (ii) the Petition for Declaratory Ruling. The PDR is required as the post-emergence ownership structure — given Bardin Hill's UK-domiciled Man Group plc parent and the broader investor base of the other Backstop Parties — may cause indirect foreign ownership to exceed the 25% cap under Section 310(b)(4) of the Communications Act of 1934, and FCC authorization is required before that threshold can be crossed. A pro forma transfer-of-control filing will be made shortly post-petition; 180-day post-confirmation Effective Date milestone (waivable only by Required Consenting Creditors), backstopped by a separate 360-day-post-RSA Outside Date with an automatic 90-day extension if FCC approval is the sole outstanding condition. The post-emergence governance package was negotiated "to be consistent with FCC rules and policies" — Backstop Parties take no role in programming, personnel, finances, or day-to-day broadcast operations, which remain with the licensee subsidiaries. Critically, and unlike Audacy, the SBS Plan as drafted requires the Petition for Declaratory Ruling to be granted as a condition to the Effective Date (no temporary-waiver / emerge-pending-PDR construct), placing more of the FCC timing risk in front of emergence rather than behind it.

Releases, Governance, and Other Plan Mechanics

Article IX of the Plan implements a tiered, consensual release architecture — automatically capturing institutional parties (Debtors, Reorganized Debtors, Consenting Creditors, Backstop Parties, Ad Hoc Committee, Existing Trustee (Wilmington Trust), DIP Secured Parties, DIP Lenders, and New Trustees / New Noteholders) and accepting Class 2 holders, while requiring affirmative opt-in from abstaining or rejecting Class 2 holders and non-voting Classes 1, 3, 4, and 7-9. The release extends via a broad affiliate and professional advisor tail. Releases, indemnity, and insurance expressly extend to Manuel E. Machado in his former-director capacity. Debtor and third-party releases each carve out actual fraud, gross negligence, willful misconduct, and criminal conduct. Exculpation is narrower — limited to estate fiduciaries (Debtors' Estates, retained professionals, and Debtors' directors and officers who held office between the Petition Date and the Effective Date) and carved-out only for actual fraud, willful misconduct, or gross negligence. A § 1141(d)(1) discharge runs at Effective Date; the Existing Indenture survives solely to permit Wilmington Trust to make distributions, preserve charging liens, seek expense reimbursement, appear in these Cases, and execute Lien-release documents. All D&O Liability Insurance Policies are assumed under § 365(a), with a six-year tail to be purchased.

Reorganized SBS governance vests with a five-member New Board (40%/two directors; 20–40%/one director; Bayside-appointed Specified Director while the Bayside Condition holds; CEO ex officio; 10% holders entitled to a board observer). Customary tag, drag, preemptive, demand-and-piggyback registration rights apply at 5%/20% thresholds; transfers to competitors or transfers triggering foreign-ownership issues are restricted; Sarbanes-Oxley § 404 is expressly disapplied. Raúl Alarcón, Jr. continues as CEO (no longer Chairman) under a 12-month auto-renewing employment agreement at a $1,750,000 base salary with a closing-and-FCC cash bonus; Richard Lara continues as COO and General Counsel at a $750,000 base plus a $750,000 cash bonus on the same trigger. All payments to Alarcón-family Related Parties were halted on RSA execution and may not resume except for eight "Necessary Related Parties" identified at Exhibit 4 to the Restructuring Term Sheet, each in a defined operational role; no severance or exit compensation is payable. A Management Incentive Plan reserving up to 10% of fully diluted New Common Stock is available for management and non-employee directors of Reorganized SBS, with allocations, vesting, and repurchase rights set by the New Board post-emergence.

First-Day Relief and Professional Advisors

Consistent with the full-pay character of the Plan, the Debtors filed a customary first-day slate alongside the $30 million DIP motion: interim/final caps of approximately $2.8M / $4.78M on wages (including $1.29M PTO) for the Company's 324 employees (286 FT / 38 PT; 19 union; ADP processed); $2M / $15M trade payables (no critical-vendor designation given GUC unimpairment); $1.66M / $2.25M taxes (plus ~$200K residual Puerto Rico audit exposure); $1.2M customer programs; $50,096 utilities adequate-assurance deposit; $202K insurance / premium finance against ~$3M annual premium load. Schedules, SOFAs, and the § 341 meeting are requested to be waived conditioned on confirmation within 60 days. The Debtors operate ten bank accounts plus a PayPal account across City National Bank of Florida (where Account #1182 serves as the primary master account), Bank of America, Banesco, and Banco Popular de Puerto Rico; substantially all subject to deposit account control agreements (DACAs) in favor of Wilmington Trust; limited § 345(b) relief and continuation of intercompany transfers are requested. NOL trading procedures (Docket 15) protect § 382 tax attributes pending emergence.

Debtor advisors: Fried, Frank, Harris, Shriver & Jacobson LLP (lead counsel); Morris, Nichols, Arsht & Tunnell LLP (Delaware co-counsel); GLC Advisors & Co., LLC (investment banker); Riveron RTS, LLC and Riveron Management Services, LLC (financial advisor / CRO services through Jesse York); Kroll Restructuring Administration LLC (claims agent).

Ad Hoc Committee advisors: Milbank LLP and Richards, Layton & Finger, P.A. (counsel); M3 Advisory Partners, LP (financial advisor).

Existing Trustee (Wilmington Trust, N.A.) advisors: Seward & Kissel LLP (Counsel).

DIP Agent: Brigade Agency Services LLC.

Fronting Lender: Jefferies Capital Services, LLC.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.