Case Summary: DISH DBS & DISH Wireless Chapter 11

DISH DBS and DISH Wireless, EchoStar subsidiaries, filed dual-track Chapter 11 cases to reorganize the declining DISH/Sling pay-TV business and wind down DISH Wireless via a §363 sale, after the FCC pressed EchoStar to sell the spectrum licenses needed for the 5G network or face license forfeiture.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Englewood, CO, DISH DBS Corporation ("DBS") and DISH Wireless L.L.C. ("DWLLC"), together with their Debtor⁽¹⁾ and non-Debtor affiliates, are subsidiaries of EchoStar Corporation (NASDAQ: ECHO) ("EchoStar," and collectively with the Debtors and EchoStar's non-Debtor subsidiaries, the "Company"). The Company is a provider of technology, networking services, television entertainment, and connectivity, serving consumer, enterprise, operator, and government customers worldwide under a brand portfolio that includes Boost Mobile, DISH, Sling TV, Hughes, and HughesNet.

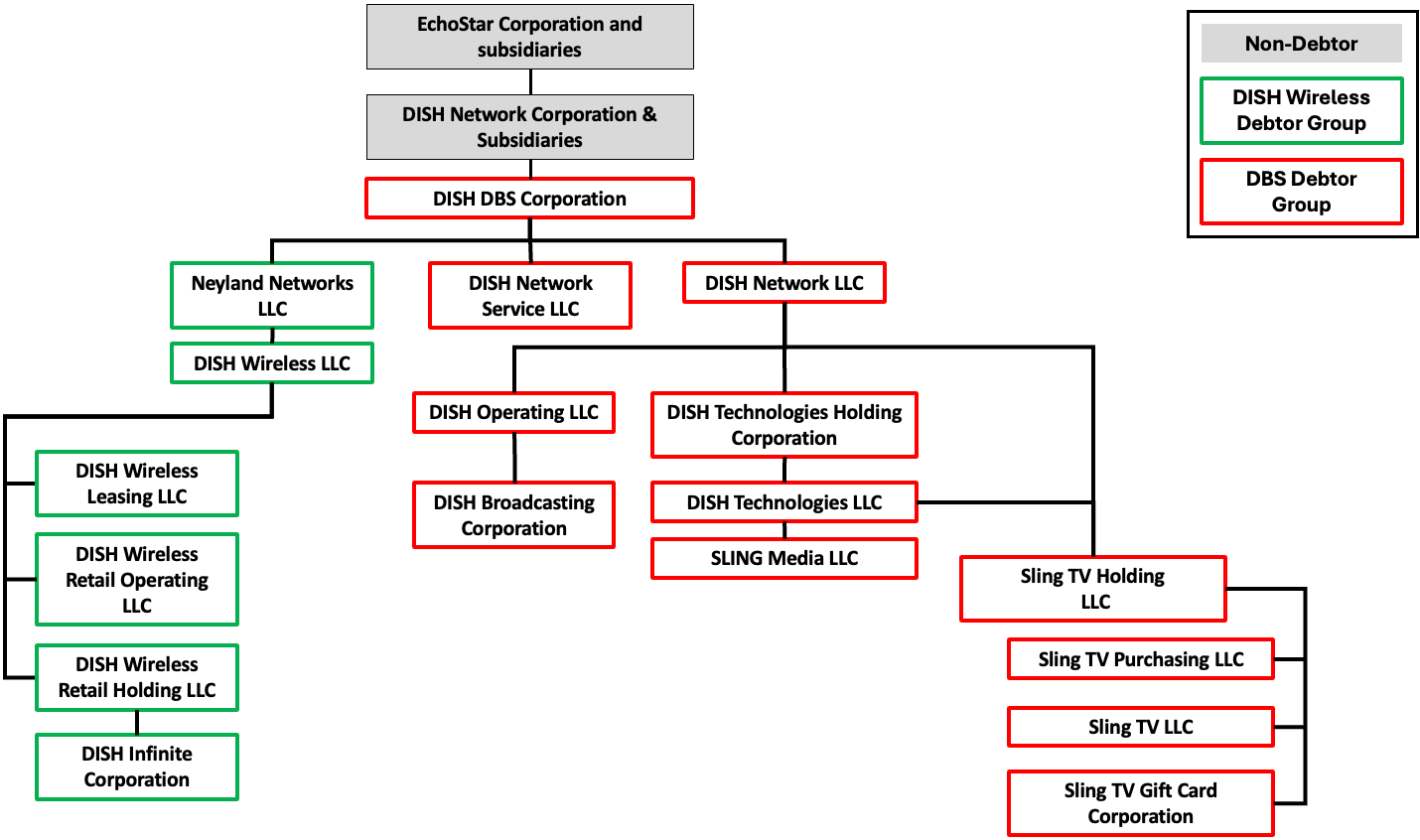

The Debtors comprise 18 entities across two groups:

- DBS Debtors (12 entities) — Comprise DBS and 11 debtor subsidiaries that operate the cash-generative pay-TV business under the DISH and Sling TV brands. The DBS Debtors will reorganize pursuant to a restructuring support agreement, while emerging as a going concern.

- DISH Wireless Debtors (6 entities) — Comprise DWLLC, its parent Neyland Networks LLC, and 4 debtor subsidiaries. From 2020 to 2025, the DISH Wireless Debtors (led by DWLLC) built and operated the Company's nationwide 5G network under the Boost Mobile and Gen Mobile brands, investing over $13 billion in infrastructure. After the FCC compelled parent EchoStar to sell the underlying spectrum licenses, the network was stranded and decommissioned. The DISH Wireless Debtors will now sell substantially all of their remaining assets under section 363, with parent EchoStar as stalking horse bidder.

DISH DBS Corporation and certain affiliates filed for Chapter 11 protection on June 30, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Southern District of Texas, reporting $1 billion to $10 billion in assets and $10 billion to $50 billion in liabilities.

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

Early Satellite Era

The Company was founded in 1980 by Charlie Ergen, Candy Ergen, and James DeFranco as a C-band satellite distributor, before moving into direct broadcast satellite television. It filed for a direct broadcast satellite license in 1987, secured orbital slot 119° west longitude in 1992, and launched its first satellite, EchoStar I, in 1995, gaining its first pay-TV customers the following March. Through the late 1990s and 2000s, the Company steadily expanded its satellite fleet and consumer television operations.

Wireless Expansion Era

In 2008, the Company separated into two publicly traded entities, with EchoStar retaining satellite and infrastructure assets and DISH Network Corporation ("DNC") holding the consumer satellite television business. That same year, it began a sustained push into wireless, ultimately spending more than $30 billion to acquire spectrum licenses through FCC auctions and secondary-market purchases. In 2015, it launched Sling TV, a live over-the-top streaming service, and in 2020 the Company acquired Sprint's Boost Mobile to preserve a fourth facilities-based wireless carrier following T-Mobile's acquisition of Sprint — a commitment that led to the buildout of a nationwide 5G network on a cloud-native, open radio access architecture.

On December 31, 2023, the two companies reunited when DNC merged back into EchoStar, combining the Satellite and Broadband Communications, Pay-TV, and Wireless businesses under a single corporate structure after more than a decade apart. Most recently, in March 2026, the Company launched the EchoStar XXV Ku-band satellite to support DISH Network's direct-to-home broadcasting across North America.

Corporate Organizational Structure

Operations Overview

The Company operates four business segments, but only two fall within these Chapter 11 cases: Pay-TV, the DISH and Sling TV business run by the DBS Debtors (a going concern being restructured through the Plan), and Other, the legacy 5G network held by the DISH Wireless Debtors (being sold and wound down after the spectrum was sold off). The remaining two — Wireless, the operating Boost Mobile/Gen Mobile business now run as a Hybrid MNO through non-Debtor BoostCo, and Broadband and Satellite Services, run through EchoStar's Hughes subsidiaries — sit outside the filing.

Pay-TV

The DBS Debtors deliver pay-TV under the DISH and Sling brands — a declining but cash-generative business, at roughly 65% (~$9.7 billion) of EchoStar's FY2025 consolidated revenue and ~$2.4 billion of operating income. At March 31, 2026 they served approximately 6.6 million subscribers: ~4.8 million DISH satellite and ~1.8 million Sling. DISH is a vertically integrated direct-to-home satellite service delivered via a fleet of eight satellites (seven owned, one leased) under multiyear, tiered-bundle agreements. Debtor Sling TV L.L.C. is the Company's over-the-top streaming offering: an internet-delivered, no-contract skinny bundle aimed at cord-cutters and mobile-first viewers seeking a lower-cost alternative.

Wireless

Wireless is the Company's newest revenue segment, offering nationwide service under the Boost Mobile and Gen Mobile brands to approximately 7 million subscribers as of the Petition Date. This business was originally built and operated by DWLLC and its subsidiaries (the DISH Wireless Debtors), which spent more than $13 billion deploying a nationwide 5G network. After the FCC compelled EchoStar to sell the underlying spectrum to AT&T and SpaceX, the Company could no longer run its own network and, in August 2025, carved the going-concern wireless business out of the DISH Wireless Debtors: the customer relationships, key contracts, and core network assets were contributed to Boost SubscriberCo L.L.C. ("BoostCo"), a non-Debtor subsidiary under DNC, in exchange for $5.0 billion of intercompany debt forgiveness.

The segment now operates as a Hybrid MNO — the Company owns the network core (the software that authenticates subscribers and processes calls, texts, and data) and retains the customer relationship, while leasing spectrum and cell sites from a third-party carrier (principally AT&T) to carry the traffic. Because this business now runs through non-Debtor BoostCo, the operating Wireless segment is not part of the Chapter 11 cases. For FY2025, the segment generated ~25% (~$3.8 billion) of consolidated revenue but posted an operating loss of ~$495 million and has run operating losses every year since 2022.

Other (Legacy 5G Network)

The Other segment consists of the Company's legacy 5G network and related deployment assets that are not used in the Hybrid MNO operations — in effect, what remained inside the DISH Wireless Debtors after the going-concern wireless business was carved out to BoostCo. When EchoStar sold the spectrum licenses that DWLLC needed to operate the 5G network, the physical infrastructure DWLLC had built was stranded: DWLLC discontinued deployment in August 2025 (having met its interim and final FCC buildout requirements), began decommissioning, and by November 15, 2025 the network carried no customer traffic.

Legal and Regulatory Framework

The Company's businesses are built on federal spectrum rights, and the FCC is the central regulator across them. Under the Communications Act, the FCC issues the licenses and authorizations required to use electromagnetic spectrum, sets buildout milestones and other conditions whose breach can result in termination, and acts through its Wireless and Space Bureaus, which can grant extensions, review petitions for reconsideration of prior decisions, and terminate licenses. Licensees must pay annual regulatory and filing fees, maintain control of their licenses and facilities, avoid harmful interference with other users, and coordinate their operations with them.

- On the Pay-TV side, FCC oversight sits at the core of the DISH satellite television framework. The DBS Debtors hold the satellite and orbital-slot licenses used to deliver pay-TV, subject to construction and public-interest obligations and to technical parameters governing interference, signal strength, and coverage. The business also depends on retransmission consent from local broadcast stations and on multiyear content-licensing agreements that intersect heavily with copyright law, and it is subject to FCC and FTC truth-in-billing and advertising standards, telemarketing restrictions, and privacy statutes.

- On the Wireless side, the dependency is more acute: the Company cannot operate its facilities without an FCC license for its frequencies, so the FCC's stated intention to invalidate EchoStar's licenses meant the Company could not continue operating its licensed system. Critically, the wireless spectrum licenses that carried the 5G buildout milestones were held by EchoStar and its non-Debtor affiliates — not by the DISH Wireless Debtors.

Workforce

The Debtors have no employees of their own. Their entire workforce is legally employed by non-Debtor Echosphere L.L.C. — the Company's employer of record — and made available to the Debtors under a Shared Services Agreement dated May 5, 2026. Echosphere employs approximately 9,100 U.S. workers who serve the enterprise as a whole, with each Debtor bearing the cost of only the portion of their time spent on its operations. Non-Debtor parent DNC funds the associated payroll and benefits on Echosphere's behalf, and the Debtors reimburse DNC for their allocated share as intercompany Reimbursement Obligations. As of the Petition Date, DBS owed DNC approximately $47.7 million on account of these employee-services allocations, while the DISH Wireless Debtors owed roughly $1.0 million.

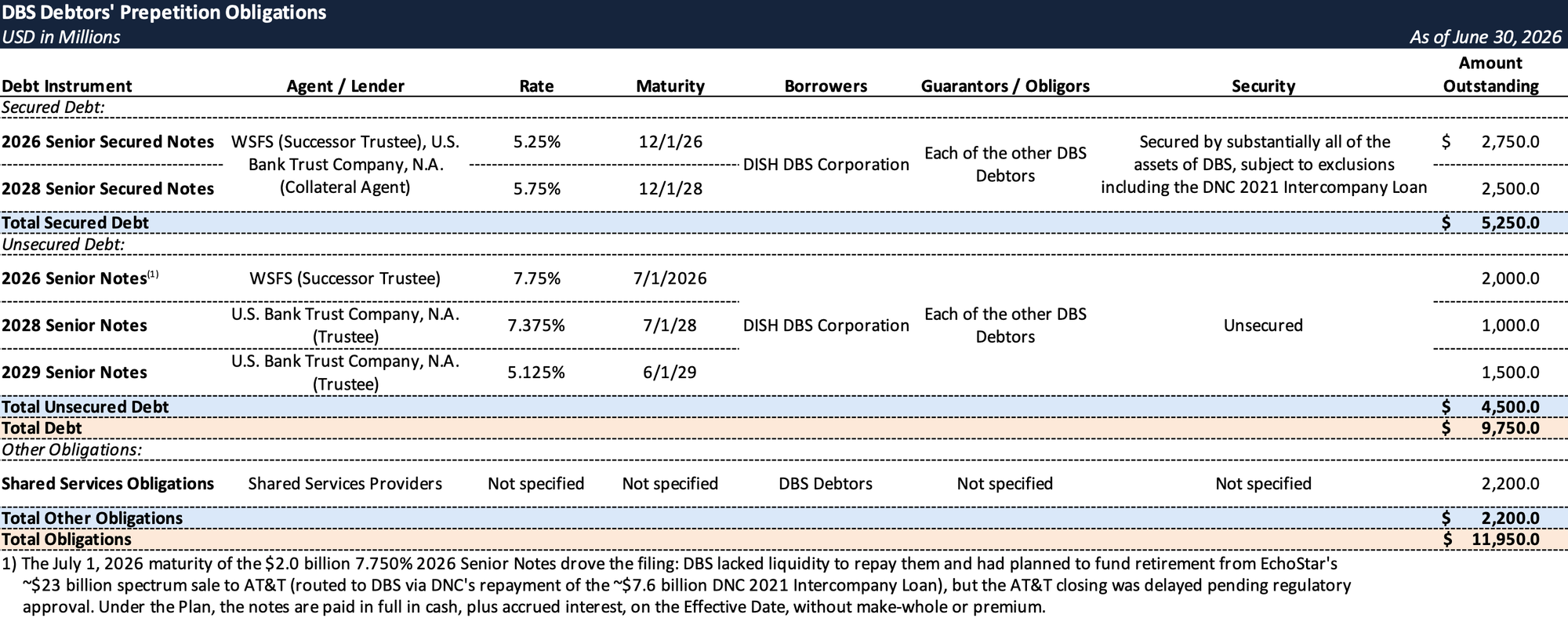

Prepetition Obligations

DBS Debtors — Intercompany Loans

- $7.6 billion 2021 intercompany loan to DNC ("DNC 2021 Intercompany Loan") — DNC used the proceeds to finance wireless spectrum license purchases and general corporate purposes, including the 5G network deployment. The loan comprises 2 tranches — one maturing on December 1, 2026 with $4.8 billion outstanding as of the Petition Date (the "2026 Tranche"), and another one maturing on December 1, 2028 with $2.8 billion outstanding as of the Petition Date (the "2028 Tranche"). The DNC 2021 Intercompany Loan was initially secured by interests in the Company's 3.45–3.55 GHz licenses. In the first quarter of 2025, certain of those licenses were substituted for other previously unencumbered wireless spectrum licenses of equal or greater value. In January 2024, the Company completed a series of assignments, resulting in the transfer of the receivable of $4.7 billion in respect of the 2026 Tranche from DBS to EchoStar Intercompany Receivable Company L.L.C., a direct subsidiary of EchoStar.

- $75 million term loan to DWLLC (the "DBS Secured Loan") — DBS lent DWLLC $75 million under an April 21, 2026 term loan for general corporate purposes, approved by the DWLLC Special Committee and guaranteed by DISH Wireless Leasing L.L.C. This facility matures April 21, 2027, bears interest at 5.50% per annum payable monthly in cash, and is secured by a lien on substantially all of DWLLC's and DW Leasing's assets. The full $75 million remained outstanding as of the Petition Date and is to be repaid in full on the closing of the DISH Wireless Debtors' asset sale.

DBS Debtors — Prepetition Obligations

DISH Wireless Debtors — Prepetition Obligations

- $75 million term loan from DBS Debtors — described above.

- $3.5 billion DNC Senior Secured Notes Guaranty — DWLLC and DW Leasing guarantee DNC's 11.75% senior secured notes due 2027 ("DNC Senior Secured Notes"), which are secured by the 600 MHz spectrum licenses being sold to AT&T.

- $8.8 billion loan from DNC ("DWLLC Intercompany Loan") — Beginning in 2020, DNC lent to DWLLC to fund the 5G network buildout, later memorialized under an August 22, 2025 Loan Agreement. As of June 28, 2026 the balance was ~$8.86 billion (principal and accrued interest), maturing November 30, 2030 at 11.50% interest paid in kind. The $8.8 billion balance is net of $5.0 billion DNC forgave as consideration for the core assets and contracts DWLLC contributed to non-Debtor BoostCo in the Hybrid MNO transaction.

- $3.7 million Shared Services Obligations — Similar to the DBS Debtors, the DISH Wireless Debtors also rely on certain non-Debtor affiliates for the provision of certain operational, administrative, technological, and other corporate services that are critical to their business operations. As of the Petition Date, the DISH Wireless Debtors owe approximately $3.7 million to the Shared Services Providers in respect of their shared services obligations.

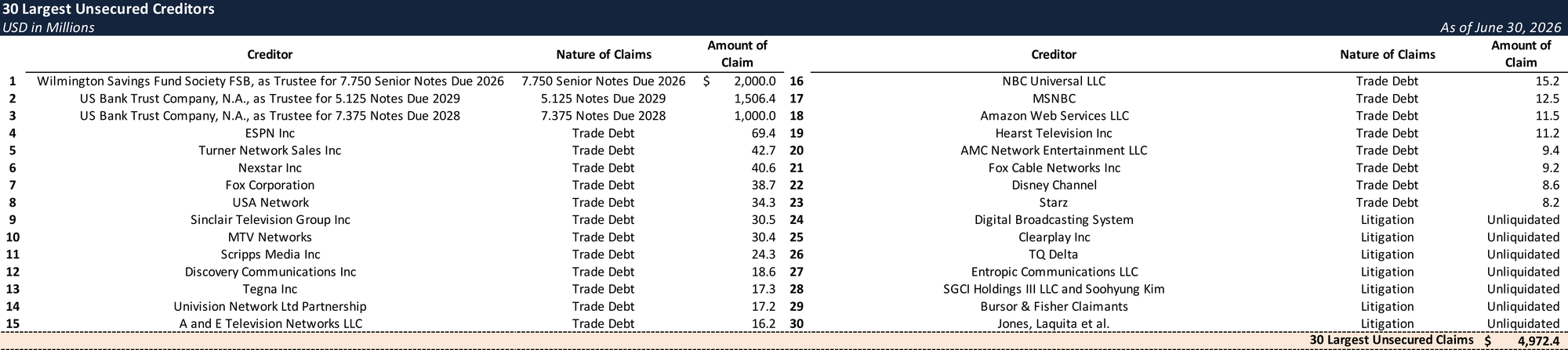

Top Unsecured Claims

Events Leading to Bankruptcy — DBS Debtors

Operational Challenges

The DBS Debtors remain a significant revenue and cash-flow generator, but the pay-TV business has been in sustained decline, pressured by industry-wide cord-cutting, rising programming costs, and streaming competition. After peaking above 14 million subscribers in 2010, the Company recorded its first full-year net pay-TV subscriber loss in 2014 and has declined every year since — a cumulative loss of roughly 7.3 million net subscribers — even with Sling TV's growth. Sling offsets some of the erosion by appealing to cord-cutters but carries higher churn than satellite because of its month-to-month model, requiring continual marketing to hold subscriber levels.

In response, the DBS Debtors have shifted from chasing gross subscriber counts to maximizing profitability per remaining subscriber. On the satellite side, this includes targeted retention credits (rather than blanket discounts), selective bill reductions or contract extensions for higher-value customers, improved service, and selective content packaging. For Sling, it means moderating acquisition-marketing spend and avoiding heavy promotional pricing. To contain programming costs, the Company has taken a harder line with broadcasters — at times accepting temporary channel takedowns rather than paying inflated rates — moved high-cost channels into higher tiers, and cut corporate staff, fleet, field/warehouse, and call-center operations to fit a smaller subscriber base.

The January 2024 Transactions and Bondholder Litigation

After EchoStar absorbed DISH Network on December 31, 2023, the combined group undertook a series of integration transactions that the DBS noteholders alleged moved value outside the DBS note credit group and beyond their reach — an allegation the debtor disputed. The January 2024 Transactions (i) assigned roughly three million pay-TV subscribers to a newly unrestricted subsidiary (DBS SubscriberCo), (ii) designated the Sling TV business as unrestricted, and (iii) transferred the ~$4.767 billion 2026-tranche intercompany receivable from DBS to an EchoStar affiliate.

DBS made intercompany loans to DNC for ordinary-course cash-management purposes, memorialized by an intercompany loan agreement maturing in 2028 (the "2024 Intercompany Loans"). Separately, on September 29, 2024, DBS SubscriberCo entered into the DBS SubscriberCo Financing — approximately $2.3 billion in secured debt and $200 million in preferred equity from outside investors — and on-lent the proceeds to DBS, primarily to repay in full ~$2.0 billion of DBS senior notes maturing in November 2024, with the remainder used for general corporate purposes including interest on other DBS debt.

In April 2024 the DBS indenture trustee sued, alleging breach and actual and constructive fraudulent transfer concerning (i) the January 2024 Transactions, (ii) the 2024 Intercompany Loans, and (iii) the DBS SubscriberCo Financing. On August 21, 2025, the court dismissed the counts tied to a later September 2024 SubscriberCo financing as speculative but allowed the remaining claims to proceed. The RSA resolved the dispute. In exchange for a dismissal with prejudice, the Consenting Creditors received a nonrefundable $125 million all-cash settlement — $75 million paid by DBS on signing and $50 million by EchoStar on June 1, 2026 — and the challenged 2024 structure was largely unwound: DBS SubscriberCo and the Sling TV entities were reconsolidated and restored as guarantors of the DBS Notes, and DNC repaid to DBS the ~$2.1 billion of 2024 Intercompany Loans ahead of their 2028 maturity.

The Failed DirecTV Transaction

The Company first sought to address its pay-TV leverage through a sale. On September 29, 2024, it signed an Equity Purchase Agreement to transfer all DBS equity to DirecTV in a debt-exchange transaction that would have cut consolidated Pay-TV debt by an estimated $11.7 billion. The deal was contingent on a companion exchange offer requiring DBS noteholders to accept a principal reduction of at least ~$1.57 billion. The noteholders rejected the exchange, and DirecTV terminated the agreement effective November 22, 2024.

Events Leading to Bankruptcy — DISH Wireless Debtors

The 5G Network Buildout and Spectrum Investment

The larger driver of distress was the wireless business. Having assembled a nationwide spectrum portfolio since 2008 and stepped in as the fourth facilities-based carrier the T-Mobile/Sprint merger required — buying Boost Mobile for $1.4 billion in 2020 — the Company invested more than $46 billion to build its nationwide 5G network: over 144,000 radios across more than 24,000 sites, and a transition from reseller (MVNO) to facilities-based operator (MNO). The FCC's buildout milestones carried forfeiture exposure of up to $2.2 billion, and the Company met each one. To densify its top markets, it obtained an expedited extension — filed September 17 and granted September 20, 2024 — trading seven accelerated commitments (including 80%-plus population coverage by year-end 2024, 24,000 sites by mid-2025, an affordable nationwide 5G plan, and Release 17 upgrades) for extended final deadlines on 1,173 licenses, pushed from June 2025 to December 2026 and ultimately June 2028.

The May 2025 FCC Letter

On April 14, 2025, SpaceX told the FCC that EchoStar used less than 5% of what would be expected from an actual wireless network operator in its 2 GHz spectrum and pressed the agency to open the band to new entrants (as reported by Via Satellite). On May 9, 2025, despite the Company's certified compliance, Chairman Carr wrote to Charlie Ergen directing staff to investigate the Company's buildout, the 2024 extension, and its 2 GHz utilization. Carr's letter took direct aim at the extension, asserting that EchoStar had negotiated behind closed doors during the previous Administration to escape its June 2025 obligations, invoking the company's earlier missed milestones in 2017 and 2018, and noting that Boost Mobile had fewer subscribers than when EchoStar acquired it five years earlier.

In June 2025 meetings, the FCC took the position that EchoStar's spectrum was underutilized and that its continued ownership was inconsistent with the public interest, asserting that the Company needed to exit the terrestrial wireless business. On June 12, 2025, EchoStar representatives met with President Trump, who encouraged an amicable resolution; in a subsequent meeting, the FCC Chairman directed EchoStar to sell a substantial portion of its spectrum licenses on an expedited timeframe, and over the following weeks the FCC pressed the Company to accelerate negotiations and expand the sale, rejecting initial proposals as insufficient.

The FCC-Directed Spectrum Sales

On August 25, 2025, EchoStar and certain non-Debtor affiliates agreed to sell their 3.45–3.55 GHz and 600 MHz spectrum licenses to AT&T — and to grant a 99-year extension of AT&T's exclusive leases on certain Hawaii licenses — for approximately $23 billion in cash, subject to adjustments. EchoStar was not obligated to close if adjustments pushed the price below $18.6 billion, though AT&T could still proceed at that $18.6 billion floor.

Two weeks later, on September 7, 2025, EchoStar agreed to sell its AWS-4 and H-Block spectrum to SpaceX for approximately $17 billion (up to half cash, up to half stock at $212.00 per share); a November 5, 2025 amendment added 15 MHz of AWS spectrum in the 1695–1710 MHz range, lifting the total to about $19 billion, with up to $11 billion payable in SpaceX stock. Combined with the AT&T deal, the two sales represent roughly $42 billion in aggregate consideration. One day after the SpaceX announcement, on September 8, 2025, Chairman Carr closed his investigation — directing staff to dismiss the reconsideration petition, confirm EchoStar's exclusive AWS-4 rights, and find its buildout obligations satisfied.

5G Network Decommissioning

In September 2025, after the AT&T and SpaceX deals sold the spectrum licenses (but none of the network infrastructure) and the FCC closed its investigation, DWLLC began decommissioning the parts of its 5G network not needed for its Hybrid MNO operations — removing software and equipment from cell sites and shutting down connections. Because EchoStar had sold the licenses on which the network depended, DWLLC could no longer operate the network or perform under its related agreements, including tower leases. The DISH Wireless Debtors now intend to sell substantially all remaining assets to EchoStar as stalking horse bidder (subject to higher or better bids) and have filed an emergency motion for approval of the bidding procedures and a sale free and clear of liens and claims.

Tower Lease Litigation and Force Majeure Disputes

Starting in September 2025, DWLLC told its tower lessors and other 5G network counterparties that the FCC's actions and the spectrum sales excused its performance under force majeure, frustration of purpose, and impracticability. It settled with hundreds of claimants, but many contested those defenses, and more than 170 lawsuits followed — seeking unpaid rent, future rent, equipment-removal costs, and possession, with asserted damages exceeding $6 billion. Six suits also name EchoStar for tortious interference. About 85 cases have reached early discovery, and on June 4, 2026 the Judicial Panel on Multidistrict Litigation declined to consolidate ten federal actions, finding them too factually distinct.

The Chapter 11 Filing

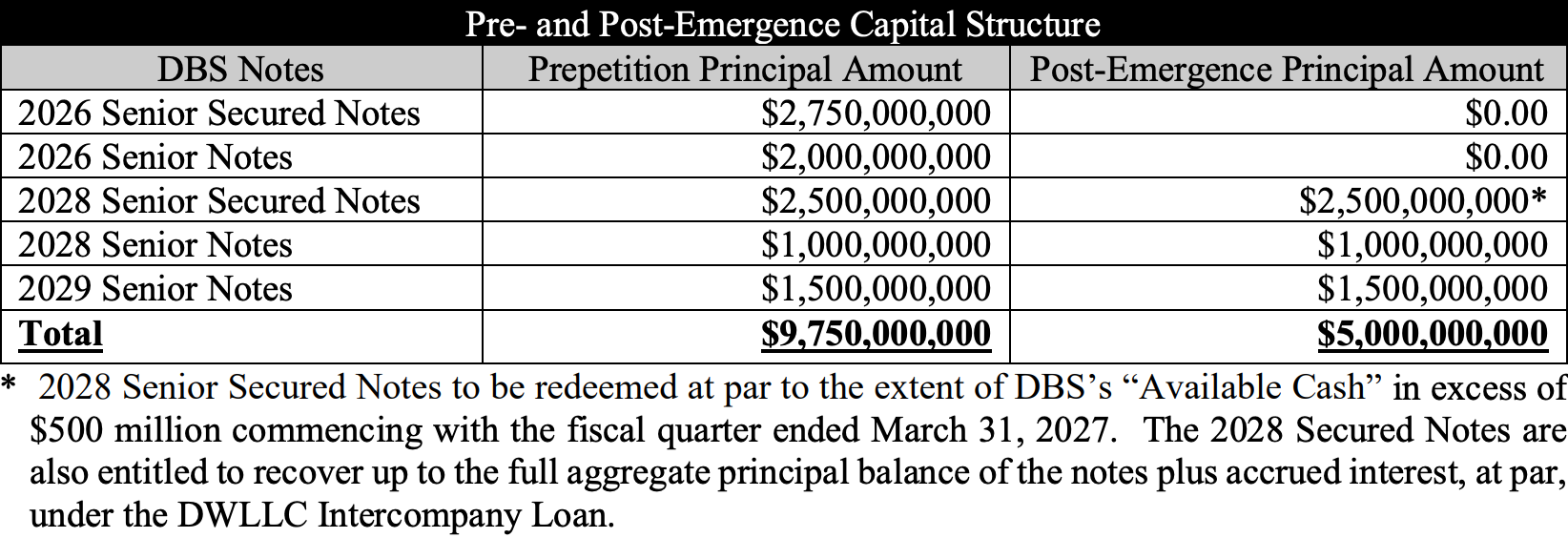

On March 19, 2026, the DBS Debtors and holders of 82% of the DBS Notes — an ad hoc group advised by Milbank and Lazard, with support since rising to approximately 88.3% by the Petition Date — signed a Restructuring Support Agreement that cuts DBS funded debt from $9.75 billion to $5.0 billion without a dollar of principal haircut. The reduction is funded with cash: no series is converted to equity and no principal is written down.

The Plan sorts claims into eighteen classes — ten against DBS (1A–1J), eight against DISH Wireless (2A–2H) — but the economics reduce to two estates. On the DBS side, every class recovers 100% by par payment or reinstatement, and only the five classes of noteholders are impaired. On the Wireless side, the sole impaired, voting class is General Unsecured Claims.

AT&T Transaction Proceeds

At the AT&T Closing Date, the proceeds of the AT&T Transactions are applied across the two estates through several distinct mechanisms fixed by the Plan and the FCC Trust Documents.

- $7.6 billion 2021 Intercompany Loan Payments to DBS (funds the DBS reorganization) — No later than three Business Days after the AT&T Closing Date, DNC pays the $7.6 billion 2021 Intercompany Loan Payments ($4.8 billion on the 2026 Tranche and $2.8 billion on the 2028 Tranche) to DBS, which in turn will be used to fund distributions to noteholders of DBS Debtors.

- $2.4 billion FCC Trust Contribution (enterprise level; Wireless-side benefit) — The $2.4 billion FCC Trust Contribution — a condition of the FCC's approval of the spectrum sales — is, per the FCC Trust Agreement, remitted to the Trust directly from the proceeds of the AT&T Transaction upon consummation of the assignment to AT&T, funding Covered Claims of 5G-network claimants, of which $200 million seeds the Type A Claims Reserve.

- $3.5 billion DNC Notes redemption (Wireless side) — The DNC Notes — the $3.5 billion 11.75% senior secured notes due 2027, guaranteed by DWLLC and DISH Wireless Leasing — are redeemed by non-Debtor DNC on the AT&T Closing Date in accordance with the AT&T License Purchase Agreement, satisfying and discharging the Class 2F guarantee with no distribution from any Debtor or Estate.

Two enterprise-level structural terms round out the DBS restructuring: a DBS Cash Sweep redeems the 2028 Senior Secured Notes at par — no premium or penalty — from available cash above $500 million each quarter, beginning the quarter ending March 31, 2027; and the indentures are amended to permit a future DirecTV combination by waiving or amending the Change of Control definition so long as the combined company's total net leverage ratio does not exceed 2.75x at closing.

DWLLC Claims Trust

The DWLLC Claims Trust is an RSA vehicle that routes one large intercompany claim from the Wireless estate to certain DBS noteholders. Its sole asset is the DWLLC $8.8 billion Intercompany Loan — DNC's loans to DWLLC for 5G Covered Activities. Prior to the Petition Date, DNC assigned the loan to DBS, and DBS to the Trust. The Trust holds that ~$8.8 billion as a general unsecured claim against DWLLC for the benefit of the 2028 Senior Secured, 2028 Senior, and 2029 Senior noteholders (Classes 1D, 1F, 1G).

The Trust recovers only from Wireless-side value (DWLLC's estate and the FCC Trust). Recoveries run through the Article VI.E waterfall: Trust fees first; then up to a $300 million cap pro rata to the three classes for optional redemption; then any excess to the 2028 Senior Secured at par; then any residual to the 2028 Senior and 2029 Senior pro rata at par. Any surplus remaining after those notes are redeemed reverts to Reorganized DBS.

Treatment of Claims — DBS Debtors

DBS reorganization is a balance-sheet restructuring aimed squarely at the funded note debt. Every non-note constituency — secured, priority, trade unsecured, intercompany, and equity — is left unimpaired and rides through. The only DBS classes voting are the five note series, and the treatments are as follows:

- Class 1C — 2026 Senior Secured Notes ($2.75 billion) — Amended 2026 Senior Secured Notes at par, plus cash for accrued interest and amounts due; not-yet-due interest rolls to the next semiannual date, not into principal.

- Class 1D — 2028 Senior Secured Notes ($2.5 billion) — Amended 2028 Senior Secured Notes at par, plus cash for accrued interest and amounts due (same mechanic as 1C). These notes also carry a quarterly redemption feature: beginning with the quarter ending March 31, 2027, DBS must redeem them at par, without premium or penalty, from available cash above $500 million each quarter. Holders separately carry a second recovery stream through the DWLLC Claims Trust as described above.

- Class 1E — 2026 Senior Notes ($2.0 billion) — Cash equal to 100% of principal plus all accrued interest, including interest on defaulted interest, through the Effective Date — no make-whole, premium, or penalty; paid via the Indenture Trustee, with unpaid trustee fees for this series paid in cash by DBS.

- Class 1F — 2028 Senior Notes ($1.0 billion) — Amended 2028 Senior Notes at par, plus cash for accrued interest and amounts due (same mechanic as 1C). Holders separately carry a second recovery stream through the DWLLC Claims Trust, as described above.

- Class 1G — 2029 Senior Notes ($1.5 billion) — Amended 2029 Senior Notes at par, plus cash for accrued interest and amounts due (same mechanic as 1C). Holders separately carry a second recovery stream through the DWLLC Claims Trust, as described above.

Treatment of Impaired Claims — DISH Wireless Debtors

On the DISH Wireless side, the only impaired class is Class 2E, DISH Wireless General Unsecured Claims — and it is the sole Wireless class entitled to vote. Every other class is unimpaired and deemed to accept.

Ordinary secured and priority claims (2A, 2B) are paid in full or reinstated in the ordinary course. The $75 million Prepetition Secured Loan (2C) — owed to DBS — is paid from the §363 sale proceeds at closing. Secured Type A Claims (2D), the small 5G-network claims of $100,000 or less, are paid in full from the FCC Trust's $200 million Type A Reserve. The $3.5 billion DNC Notes guarantee claims (2F) are satisfied with nothing from the estate at all — non-Debtor DNC redeems those notes at the AT&T closing, discharging the guarantee. Intercompany claims and equity interests (2G, 2H) are reinstated or adjusted at the Debtors' discretion within the wind-down.

Class 2E, DISH Wireless General Unsecured Claims, is the only impaired class on the Wireless side and the sole Wireless class entitled to vote. Holders receive a pro rata share of DISH Wireless Distributable Value — net §363 sale proceeds plus Effective-Date cash, after transaction costs, senior claims (DIP, the Prepetition Secured Loan, and other priority claims), and the funded Wind-Down Amount. The class is large and contested, housing the tower-lease and 5G-network claims (170-plus lawsuits, aggregate asserted damages over $6 billion, all disputed) plus a ~$8.8 billion intercompany claim (the DWLLC Intercompany Loan, now held by the DWLLC Claims Trust for the benefit of certain DBS noteholders — see DBS notes treatment in the summary table above). This large claim base against limited sale proceeds is why projected recovery is only about 1.4%–2.2% — a figure that reflects DISH Wireless Distributable Value alone and excludes any additional recovery a holder may obtain from the FCC Trust under the FCC Trust Election.

- Class 2E holders with eligible 5G-network Covered Claims have two mutually exclusive options. The FCC Trust Election lets a holder recover from the FCC Trust outside the Plan, but any Plan distribution then counts as a Third-Party Payment reducing the Trust recovery dollar-for-dollar, and submission requires an irrevocable release of other claims against the EchoStar parties. The Type A Convenience Claim Election lets a holder of a claim over $100,000 reduce it to $100,000 for payment from the FCC Trust's Type A Reserve as a Secured Type A Claim. The deadline is the August 7, 2026 Voting Deadline; no holder may make both elections for the same claim.

Post-Emergence Capital Structure

DISH Wireless Wind-Down

The DISH Wireless wind-down runs through a §363 sale anchored by a stalking horse bid from parent EchoStar, which is also funding the estate with an up-to-$85 million DIP.

The Section 363 Sale to EchoStar

EchoStar (advised by Morris, Nichols, Arsht & Tunnell), DISH Wireless's non-Debtor parent, is stalking horse for substantially all Wireless assets under an APA negotiated by the DWLLC Special Committee, not management. The purchase price is $300 million in cash less the DIP amount — EchoStar's DIP obligations offset the price rather than fund cash — and the ~$75 million secured DBS loan is repaid off the top before the remainder flows into the Class 2E distributable value. (The $300 million price is distinct from the like-sized $300 million DWLLC Recovery Cap.) The APA carries no bid protections — no break-up fee, termination fee, or expense reimbursement.

This is a monetization, not a going-concern sale: the decommissioned network — equipment, inventory, permits, and owned IP — plus, critically, the estate's own causes of action against EchoStar and its insiders, including chapter-5 avoidance, fraudulent-transfer, breach-of-fiduciary-duty, and alter-ego/veil-piercing claims. Excluded are all cash and all tower and real-property leases, leaving the multi-billion-dollar lease liabilities in the estate as rejection-damages claims. The market check is thin and largely post-petition — FTI Capital Advisors was retained just thirteen days before filing — and prepetition marketing drew pennies on the dollar: the October 2025 RFP returned bids of 5–18% of inventory cost, the December round no actionable proposal, and the entire generator inventory a single $850,000 offer.

The sale runs on a compressed timeline. The bid deadline is August 10, 2026, with qualified bids designated the following day and an auction, if competing bids emerge, on August 12. The sale hearing is set for August 17 — the same hearing at which the court will consider the disclosure statement and plan confirmation — with objections due August 14. Closing must occur within 80 days of the petition date, subject to limited extension rights, and the Special Committee retains a fiduciary out to pursue a superior transaction throughout.

The EchoStar DIP Facility

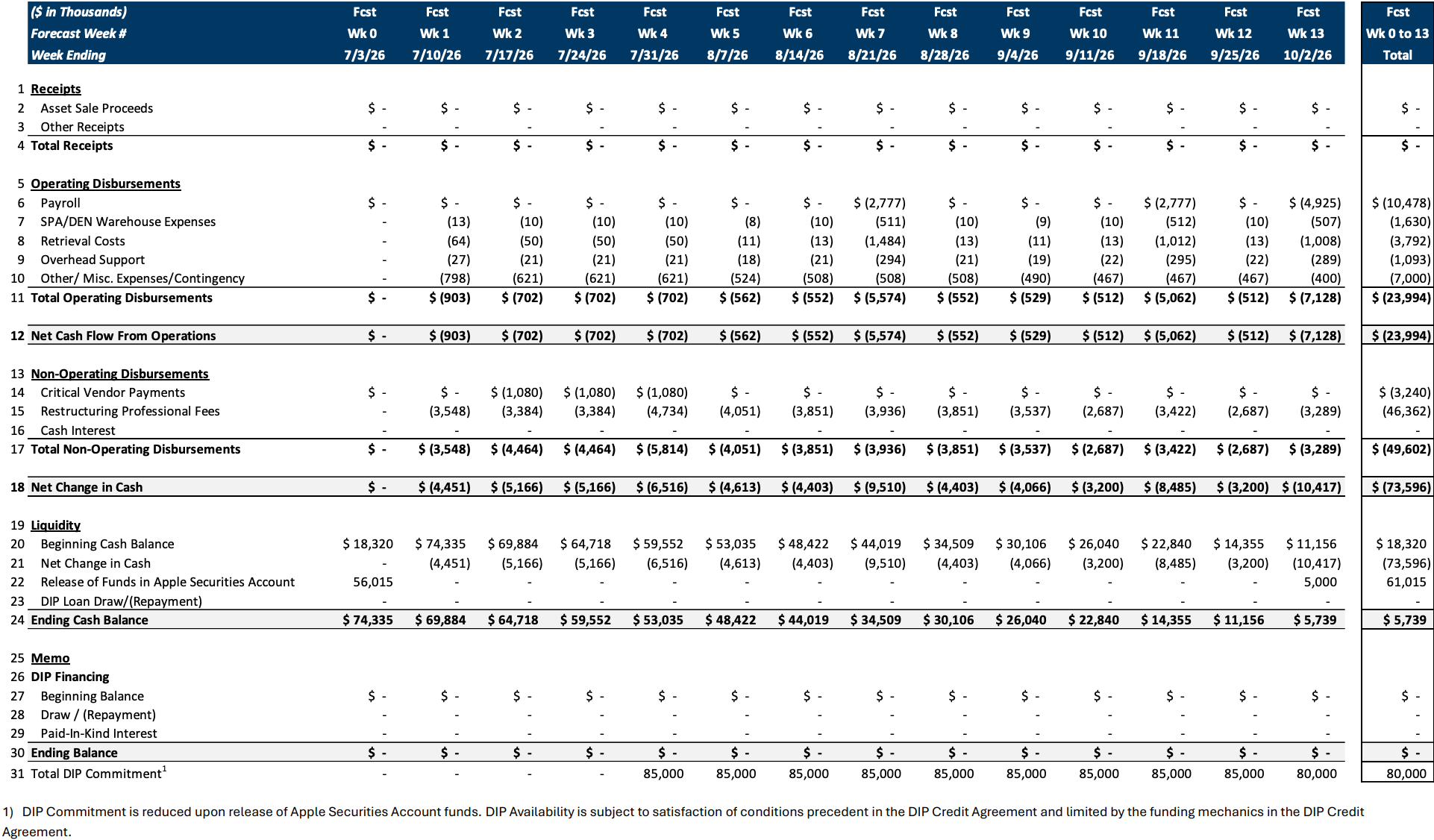

EchoStar is also providing the Wireless Debtors an up-to-$85 million multi-draw DIP term loan at 11.50% PIK, maturing December 31, 2026, with no upfront or commitment fees. One wrinkle sits upstream of it: DWLLC had pledged a securities account to Apple, Inc. as collateral for certain obligations owed to Apple, and one day before filing roughly $56 million was released from that account to DWLLC — enough near-term liquidity to let the Debtors seek the DIP on a final rather than emergency basis. Though labeled junior, the DIP's liens are subordinated only to the Carve-Out and the $75 million prepetition DBS loan (whose liens prime the DIP on the shared collateral); the Apple securities account is carved out of the DIP collateral entirely, so the DIP's juniority there is claim-level — its superpriority claim is junior to Apple's — not a lien subordination. Its §364(c)(1) superpriority claim otherwise outranks the estate's unsecured claims, including the ~$8.8 billion DWLLC intercompany loan. Notably, its Avoidance Actions collateral is defined to exclude claims against EchoStar and its affiliates — walling the estate's potential parent claims off from the lender.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.