Filing Alert: GoHealth Chapter 11

GoHealth Files Chapter 11 in District of Delaware

Update (Jun. 8, 2026): A comprehensive case summary is now available for the Chapter 11 bankruptcy filing of GoHealth, Inc.

GoHealth, Inc. and its debtor affiliates⁽¹⁾, a Chicago, IL-based health insurance marketplace and Medicare-focused digital health company, filed for Chapter 11 protection on Jun. 7 in the U.S. Bankruptcy Court for the District of Delaware.

The company traces its distress to its 2020 NASDAQ IPO (ticker “GOCO”), whose ~$6.6 billion valuation invited new entrants and intensified competition in the Medicare Advantage (“MA”) e-broker space, prompting debt-funded investment in lead acquisition—including a 2021 refinancing and a $200 million incremental revolver—premised on policyholder-retention assumptions that proved overstated. Successive amendments raised pricing and tightened covenants while a post-COVID rise in LIBOR more than doubled the company’s effective interest rate even as funded debt grew. Its Non-Agency Business, stood up in late 2022 to monetize Carrier marketing and one-time qualification fees, subsequently unraveled as rising medical costs outpaced CMS reimbursement, updated condition risk-score rules and continued legal risk tied to historical coding and billing practices eroded Carrier MA profitability, and Carriers curtailed marketing spend and broker distribution—sharply reducing demand for the company’s higher-value offering.

The 2024 AEP skewed toward lower-margin Agency Business, which carries year-one commissions below customer acquisition cost (“CAC”), swelling the company’s renewal-driven “Backbook Asset” while depressing Q1 2025 liquidity and culminating in a going-concern disclosure in the notes to its Q2 2025 Form 10-Q filed May 16, 2025. A May 1, 2025 DOJ Complaint-in-Intervention under the False Claims Act and Anti-Kickback Statute—which the company denies and is defending—further strained constrained liquidity. An August 2025 super-priority financing (a $117 million facility comprising $82 million of new money and a ~$35 million revolver roll-up) paired with the 14th Amendment enabled the Company to secure financial statements free of a going-concern qualification ahead of the 2025 AEP, but a Moelis-led marketing and merger process failed to yield a near-term third-party transaction by late February 2026, prompting a pivot to a lender-led change of control that preserved value for junior stakeholders.

The prepackaged plan—supported by 100% of prepetition lenders, 61% of Class A common holders, and over 99% of GoHealth Holdings interests—transitions ownership to the secured lenders, under which holders of approximately $173.9 million of Super-Priority Loan Claims receive second-out takeback term loans and holders of approximately $598.3 million of First Lien Claims receive approximately $588.3 million of third-out takeback term loans and new common equity, while leaving general unsecured claims and preferred equity unimpaired through reinstatement and funding a $10 million Equity Recovery Pool for common equity holders via a new $20 million exit facility. With no meaningful unencumbered cash, the cases will be funded through the consensual use of cash collateral—projecting a remaining balance of approximately $7 million after four weeks and $6 million after six weeks—and target a combined disclosure statement and confirmation hearing 39 days after the Petition Date to emerge ahead of the August 1 pre-AEP window and the 2026 AEP.

GoHealth, Inc. reports $917.9 million in assets and $986.7 million in liabilities. The filing indicates that there will be funds available for distribution to unsecured creditors. The case number is 26-10914.

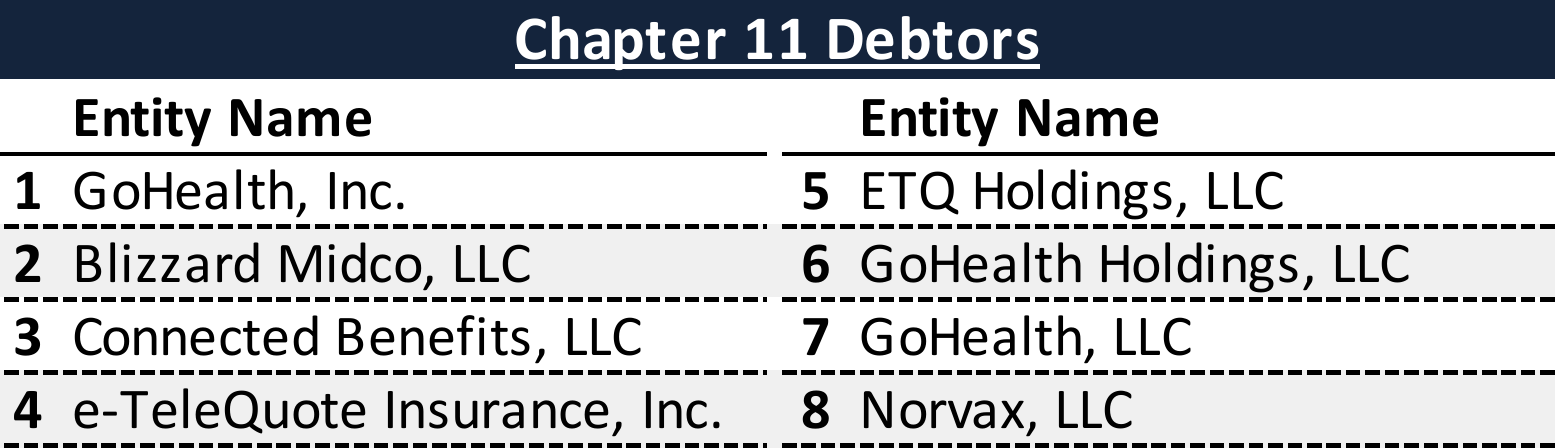

⁽¹⁾ For a complete list of debtor entities, see the Chapter 11 Debtors table.

Chapter 11 Debtors

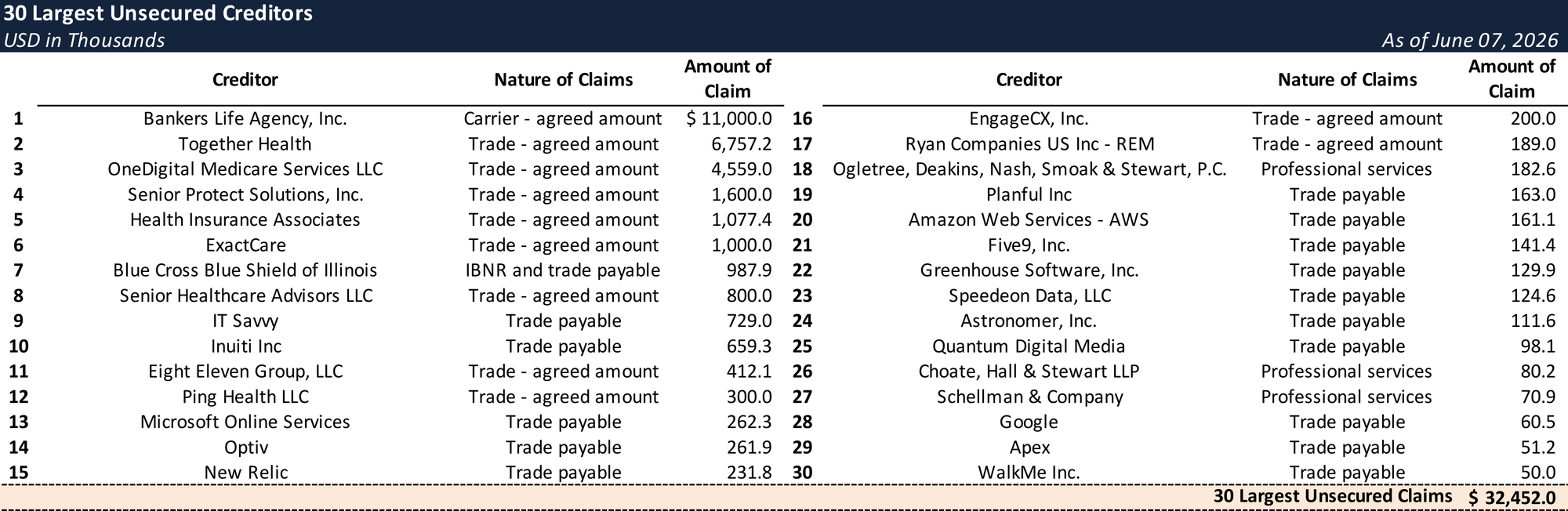

Top Unsecured Claims

Key Parties

Local Counsel:

- Laura Davis Jones

Pachulski Stang Ziehl & Jones LLP

Email: ljones@pszjlaw.com

Restructuring Counsel:

- Kirkland & Ellis LLP

- Kirkland & Ellis International LLP

Financial Advisor:

- Alvarez & Marsal North America, LLC

Signatories:

- Vijay Kotte – Authorized Signatory

Claims Agent:

- Donlin, Recano & Company, Inc.

Equity Security Holders:

- CB Blizzard Lower Holdings A, L.P. – Class A Common: 16.3%

- PSP Investments Credit USA LLC – Class A Common: 10.1%

- CB Blizzard Holdings C, L.P. – Class A Common: 8.8%

- Blue Torch Credit Opportunities Fund III LP and affiliated funds – Class A Common: 8.7%

- Vijay Kotte – Class A Common: 5.7%

- Redwood Master Fund Ltd. and affiliated funds – Class A Common: 5.5%

- NVX Holdings, Inc. – Class A Common: <1.0%; Class B Common: 49.0%

- CB Blizzard Lower Holdings B, L.P. – Class B Common: 42.7%

- Blizzard Management Feeder, LLC – Class B Common: 7.9%

- Anthem Insurance Companies, Inc. – Series A Preferred: 70.0%

- GH 22 Holdings, Inc. – Series A Preferred: 30.0%

Bondoro Insights is continuing to monitor this case and will provide further coverage as appropriate.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.