Case Summary: GoHealth Chapter 11

GoHealth filed a prepackaged Chapter 11, backed by its first-lien lenders, to restructure its funded debt and transfer ownership to them ahead of the 2026 enrollment season, after a post-IPO debt load, a sharp Non-Agency contraction, and a DOJ kickback suit drove a liquidity crisis.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Chicago, IL, GoHealth, Inc., along with its Debtor⁽¹⁾ and non-Debtor subsidiaries (collectively, "GoHealth" or the "Company"), operates a Medicare-focused, carrier-agnostic digital health insurance marketplace. Its proprietary technology lets consumers compare products offered by large health insurers, including United, Aetna, Anthem, and Humana (the "Carriers"), and supports them during and after enrollment. Medicare Advantage ("MA") plan submissions and renewals are the core business; in response to recent industry challenges, the Company has expanded into enrollment services for other plan types.

GoHealth generates revenue through two models. Under the Agency Business, its agents enroll consumers as "Agent of Record," earning an initial commission and a stream of renewal commissions from the Carriers—renewals that accumulate into the commissions-receivable "Backbook Asset," the estate's principal asset. Under the Non-Agency Business—approximately 15% of FY2025 net revenue—GoHealth qualifies and transfers consumers to Carriers, which complete the enrollment themselves and instead pay upfront marketing and qualification fees.

As of the Petition Date, GoHealth employed approximately 296 full-time employees—239 of them at the Debtors, including 107 internal licensed agents—and used a network of approximately four external partners and their licensed agents to serve Medicare-eligible consumers in all 50 states.

GoHealth, Inc. and certain affiliates filed for Chapter 11 protection on June 7, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the District of Delaware, reporting $917.9 million in assets and $986.7 million in liabilities (as of March 31, 2026).

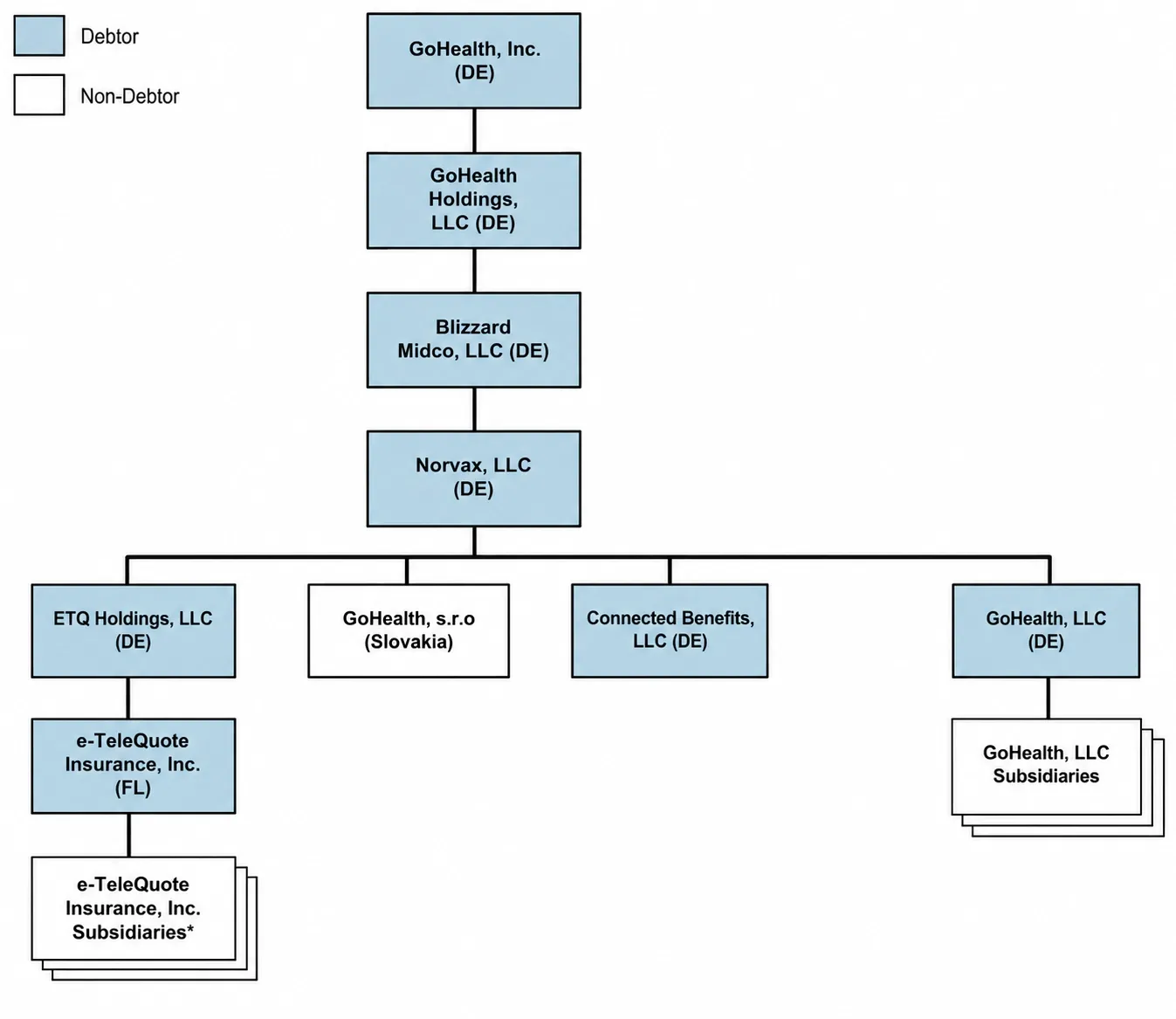

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

GoHealth was founded in Chicago in 2001 as Norvax, Inc. by Brandon Cruz and Clinton Jones, initially providing lead management software, website creation tools, and real-time quoting and enrollment technology to independent health insurance brokers. Over time, the Company shifted from a B2B software model to a direct-to-consumer marketplace — a transition accelerated by the passage of the ACA in 2010 — first as a comparison site and then as a full-service agency offering one-on-one licensed agent consultations beginning in 2008. In 2012, the Company rebranded under the unified "GoHealth" banner, received a $50 million private equity investment, and gained federal government approval as a private health insurance exchange, enabling it in 2013 to become the first private marketplace to enroll consumers in ACA-subsidized plans. The decisive turn came in 2016, when GoHealth entered the Medicare Advantage market directly — having previously served it only through external partners — and MA has remained its primary product focus ever since.

Key Capital Events (2019–2024)

- Centerbridge LBO (2019): Centerbridge Partners acquired a majority stake at a valuation of approximately $1.5 billion—the September 13, 2019 acquisition of Norvax that also dates the First Lien Credit Agreement now at the center of these cases.

- IPO (2020): GoHealth priced its Nasdaq IPO ("GOCO") at $21 per share on July 15, 2020, raising $914 million at a valuation of approximately $6.6 billion—one of the year's largest healthcare IPOs.

- e-TeleQuote (2024): On September 30, 2024, GoHealth acquired Medicare marketplace e-TeleQuote without the transfer of consideration—former parent Primerica, which had bought 80% in 2021 at a reported ~$600 million enterprise value, surrendered its interests to exit senior health—producing an $84.5 million bargain-purchase gain. As part of this acquisition, e-TeleQuote became one of GoHealth’s Downline Partners under GoHealth’s external agent channel, GoPartner Solutions, which allowed e-TeleQuote to continue operating as an independent agency while also having access to GoHealth’s proprietary technology and numerous marketing channels.

Organizational Structure

Operations Overview

GoHealth earns commissions for matching consumers — predominantly Medicare-eligible seniors — with health insurance plans, and collects fees from Carriers for administrative services tied to its MA business. It operates two distinct models, the Agency Business and the Non-Agency Business, through its internal licensed agents and roughly four external Downline Partners.

Agency Business: The Backbook Engine

Under the Agency model, GoHealth's agents guide consumers to the best-suited MA plan through the Company's proprietary Encompass workflow — delivering a "PlanFit Check-Up," a holistic health and benefits assessment that generates a unique PlanFit Score based on over 180 factors — and electronically submit the enrollment forms to the applicable Carrier. As "Agent of Record," GoHealth earns a one-time initial commission on each new enrollment, followed by monthly renewal commissions for as long as the policyholder remains in the same insurance product. The majority of commissions revenue is generated through MA plan enrollment, with a smaller amount deriving from the sale of individual and family plan insurance products.

The Agency Business operates through both Internal Agents and external Downline Partners via GoHealth's GPS Channel — GoPartner Solutions. Under the GPS Channel, Downline Partners source their own consumers through their own marketing efforts but access GoHealth's technology platform, health plan relationships, and support teams to help consumers evaluate their options. When a Downline Partner completes an enrollment, GoHealth becomes the Agent of Record and earns the commission, remitting a contractually agreed portion to the applicable partner. Although Internal Agents generate the majority of GoHealth's revenues, the GPS Channel nevertheless represents a material portion of the Company's annual revenues.

The renewal stream across both Internal Agents and Downline Partners — the constrained lifetime value of commissions on in-force policies — is the "Backbook Asset," and it is, for practical purposes, the entire estate: commissions receivable stood at $852.4 million at March 31, 2026 ($214.6 million current), down from $925.2 million at year-end 2025, and constitutes nearly all of the $917.9 million of petition-date assets. Commissions payable owed to Downline Partners totaled $209.2 million at March 31, 2026 (10-Q (Q1 2026), Condensed Consolidated Balance Sheets) — a material offset against the Backbook Asset in any collateral analysis.

Seasonality and the AEP Cash Lag

Enrollment is concentrated in the 53-day Annual Enrollment Period from October 15 to December 7 each year: submissions land in the fourth quarter, but the resulting revenue does not begin converting into cash until the first quarter of the following year, with renewal commissions providing steadier collections across the cycle. The next-highest enrollment period runs from January 1 through March 31 during the MA open enrollment period, with the second and third quarters being the lowest enrollment periods.

Non-Agency Business

Under the Non-Agency model, GoHealth's Internal Agents or Downline Partners qualify consumers for a particular MA plan through the Encompass workflow and transfer them to the applicable Carrier, which submits the enrollment directly to Medicare and acts as Agent of Record. In most Encompass relationships, Carriers separately retain GoHealth through a business-process-outsourcing arrangement to provide dedicated licensed agents to complete enrollments on their behalf.

The economics invert the Agency model: Carriers provide upfront marketing funds plus a one-time qualification fee per enrollment — exceeding GoHealth's customer acquisition cost and paid before or shortly after that cost is incurred — but GoHealth receives no renewal commissions and builds no backbook. The Non-Agency Business represented approximately 15% of FY2025 net revenue, down from 27% in 2024 (10-K (FY2025), MD&A).

GoHealth Protect

Launched in the first half of 2025, GoHealth Protect is a suite of life insurance products — beginning with a final expense offering covering funeral and burial costs — designed to provide financial security for consumers concerning end-of-life costs. It offers guaranteed acceptance without a diagnostic medical exam, making it accessible to consumers with pre-existing conditions. GoHealth is not the Agent of Record; its obligation is complete upon the carrier receiving the enrollment, with cash collected at or near the point of sale, in some instances funded in advance of marketing activities. Despite lower per-submission revenue than Medicare products, the line serves three purposes: reducing AEP seasonality by boosting Q2 and Q3 revenue, providing a cushion against fluctuating MA demand, and increasing agent utilization year-round.

Special Needs Plans ("SNPs")

SNPs are condition-specific MA plans for beneficiaries dually eligible for Medicare and Medicaid due to chronic or severe diseases or financial circumstances, with membership limited to individuals with one or more specific traits to ensure each plan is tailored to a specific medical or financial need. Like GoHealth Protect, SNPs boost revenue outside the AEP and improve year-round agent utilization. SNPs are sold through both the Agency and Non-Agency Business.

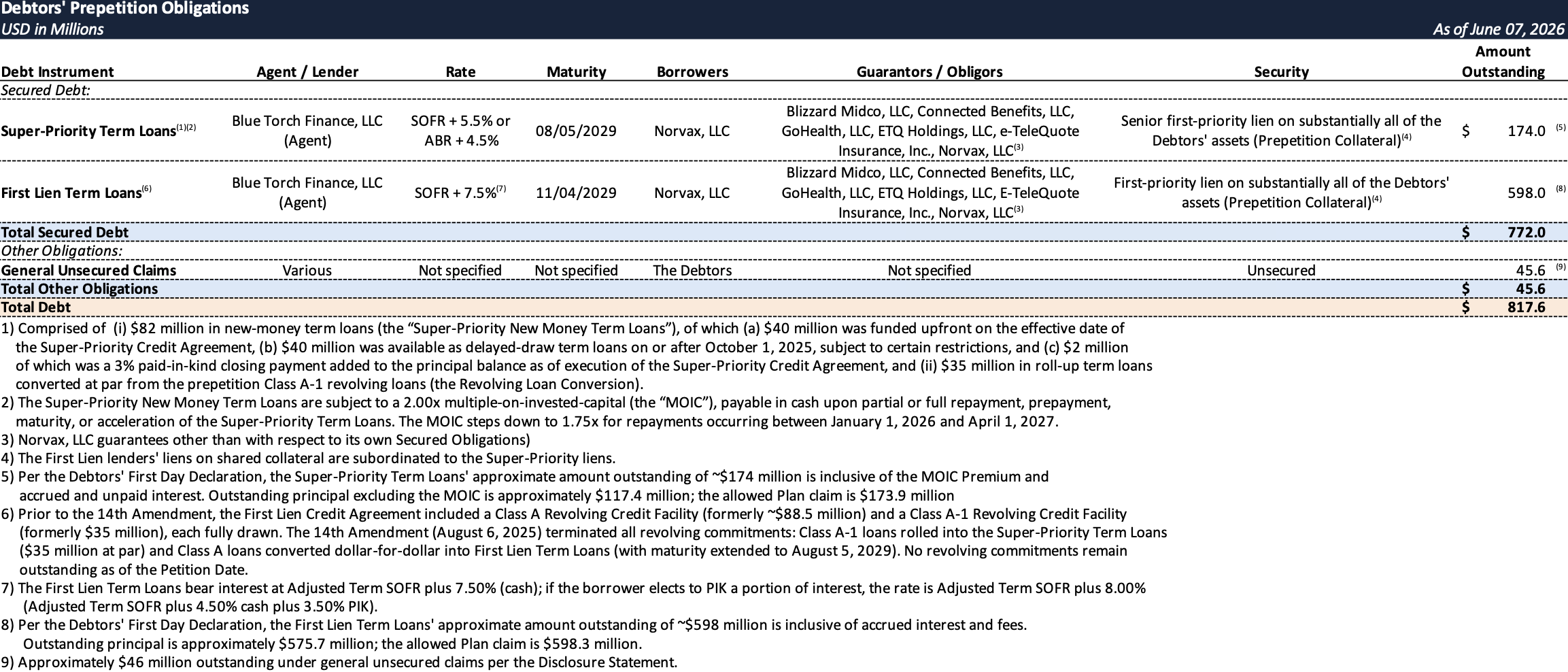

Prepetition Obligations

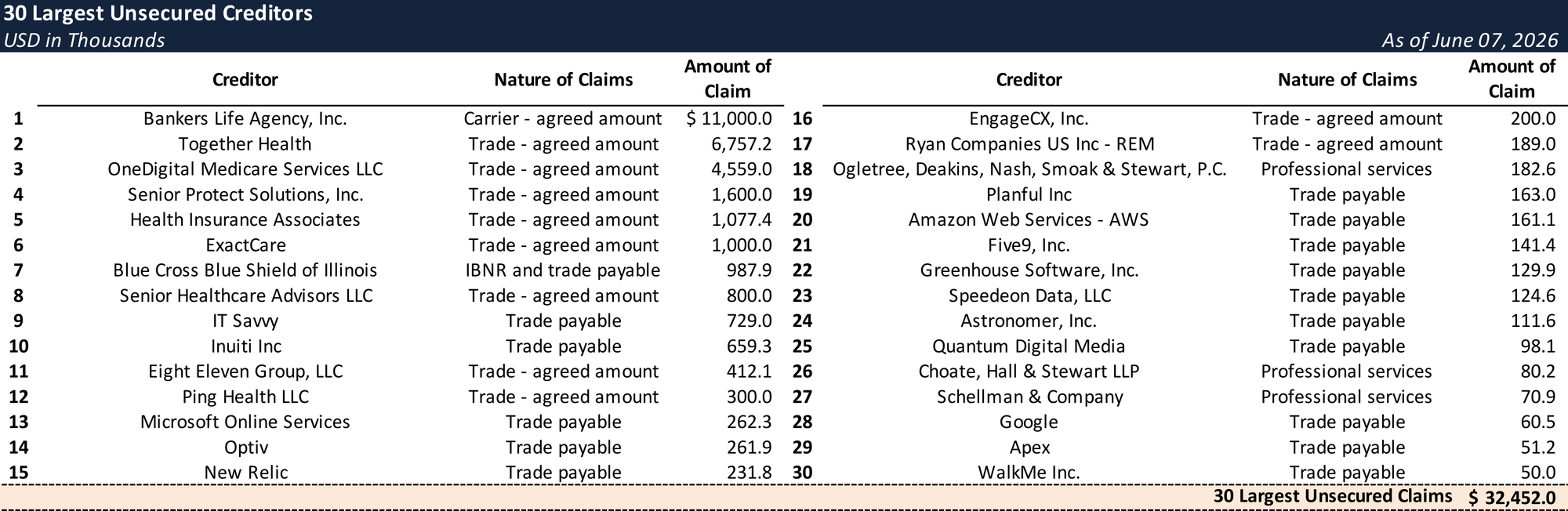

Top Unsecured Claims

Events Leading to Bankruptcy

The IPO and a Mounting Debt Burden

The circumstances giving rise to GoHealth's Chapter 11 filing largely began following the Company's 2020 IPO. Although the IPO was by all measures a success — raising over $900 million at a valuation of approximately $6.6 billion — the Company soon found itself in an increasingly competitive market that required continued investment to stay ahead. According to the CEO, GoHealth's very success was what led to its challenges: the Company's lucrative business model inspired a wave of new entrants into the field, escalating competitive pressure. In 2021, the Company entered into the fifth amendment to the First Lien Credit Agreement, pursuant to which it refinanced its then-outstanding term loan facility and raised $200 million in the form of new revolving commitments. The proceeds were deployed to, among other things, acquire high-quality leads to grow market share in an increasingly competitive healthcare marketplace. The Company's ability to service this increased debt burden was premised on, among other things, certain assumptions regarding the length of time individuals would remain in a given insurance plan. Those assumptions proved incorrect due to unforeseen shifts in the market and consumer behavior, and GoHealth struggled to generate the cash necessary to service its debt.

As a result, GoHealth entered into several amendments with its lenders, which resulted in an increase in the Company's interest rate and tightened covenants. Simultaneously, the increase in LIBOR — which followed general inflationary pressures in the post-COVID environment — further increased the Company's debt service obligations. In the aggregate, these forces resulted in the Company's interest rate more than doubling while its overall funded debt balance significantly increased.

Non-Agency Business Unraveling

Facing mounting debt obligations, GoHealth raised $50 million of preferred equity from Carrier affiliates in September 2022 and, that fall, built the Non-Agency Business as a new revenue engine — earning upfront marketing and administrative fees from Carriers plus a one-time qualification fee per enrollment, both paid before or shortly after CAC was incurred. The model initially worked, generating sufficient cash to fund term loan paydowns in March and October 2024, and GoHealth invested heavily in the model heading into the 2024 AEP.

The model's undoing reflected both company-specific vulnerabilities and a sector-wide deterioration. CMS's v28 risk-model reset — phased in over 2024–2026 — cut Carrier risk-score revenue just as healthcare utilization spiked, compressing Carrier margins at both ends. Carriers responded by retrenching across the board: Humana exited 13 MA markets for 2025, UnitedHealthcare, Humana, and Aetna withdrew from hundreds of counties for 2026, and beginning in late 2024, Aetna, Elevance, Cigna, and later UnitedHealthcare eliminated broker commissions on broad swaths of plans — with some cuts landing mid-AEP during the 2025 enrollment season, drawing state-regulator warnings. For GoHealth specifically, Carriers scaled back Non-Agency arrangements, cut marketing spend, and restricted broker distribution of high-cost plans as their own MA economics deteriorated. Non-Agency revenue fell from 27% of total net revenue in 2024 to 15% in 2025.

The 2024 AEP delivered a structurally adverse outcome: volume came in, but overwhelmingly as Agency Business rather than Non-Agency — meaning GoHealth incurred its full CAC while receiving only the much lower year-one Agency commission, with fewer Carriers providing sufficient marketing dollars to offset the gap. The Backbook Asset swelled while projected Q1 2025 liquidity — when year-one AEP commissions are actually paid — came in significantly below forecast, producing a liquidity crisis.

Going Concern and the DOJ Complaint

Two blows landed in the first half of May 2025. On May 1, 2025, the DOJ filed its Complaint-in-Intervention under the False Claims Act and Anti-Kickback Statute, naming the three largest MA insurers—Aetna/CVS, Elevance Health (Anthem), and Humana—and the three largest brokers: eHealth, GoHealth, and SelectQuote. The complaint alleges the insurers paid hundreds of millions of dollars in illegal kickbacks disguised as marketing, co-op, or sponsorship payments from 2016 through at least 2021—including more than $230 million paid to GoHealth by Anthem alone over 2017–2021 — and that Aetna and Humana conspired with the brokers to discriminate against disabled Medicare beneficiaries under 65. GoHealth denies the allegations; defending them has steadily drained its constrained liquidity.

On May 16, the Company's Form 10-Q for the quarter ended March 31, 2025 disclosed "substantial doubt about the Company's ability to continue as a going concern." According to the First Day Declaration, certain Carriers expressed serious concern about GoHealth's ability to write new business in the 2025 AEP — a particularly acute risk given that Carrier contract terminations would have been financially and reputationally devastating. In response, the Company explored various financing opportunities including a securitization of its Backbook Asset, all of which proved unsuccessful.

Prepetition Restructuring Efforts

- Credit Facility Amendments — With its revolving credit facility maturing June 30, 2025, the Company retained Kirkland & Ellis and Alvarez & Marsal in June 2025 to address its strained liquidity position and growing marketplace uncertainty. Negotiations with lenders produced the 13th Amendment, which extended the revolver maturity to September 30, 2025 and provided covenant relief — buying the Company, according to the CEO, only some but not much time to pursue strategic alternatives. The 13th Amendment also permitted a securitization of the Backbook Asset; the Company invested meaningful time and resources pursuing the transaction, which ultimately proved unactionable. With the short-term extension exhausted and the securitization off the table, the Company and its lenders closed the August 2025 Transactions on August 6, 2025 — a $117 million super-priority credit agreement providing $82 million of new capital and rolling up approximately $35 million of outstanding revolver loans, paired with the 14th Amendment terminating all revolving commitments, extending maturities to August 5, 2029, adding a PIK toggle on interest, waiving amortization through December 31, 2026, and providing various forms of covenant relief.

- Governance Changes & Sale Efforts — Concurrent with closing the Super-Priority Term Loan Facility, GoHealth appointed three new independent directors — Alan Carr, Timothy Pohl, and William Transier — and established a four-member Transformation Committee with exclusive authority to evaluate, negotiate, and recommend strategic alternatives to the Board, including potential refinancings, securitizations, mergers, acquisitions, and restructurings. On September 27, 2025, the Company engaged Moelis & Company as investment banker, and shortly thereafter launched a formal process to explore potential merger options with select counterparties — a process monitored by the Transformation Committee that would ultimately fail to produce a viable out-of-court third-party transaction.

- Operational Changes — While the merger process ran in the background, the Company's operating position continued to deteriorate. With Carrier marketing spend expected to remain modest and the Non-Agency Business unlikely to contribute meaningfully to the 2025 AEP, GoHealth shifted focus toward reducing customer acquisition costs, expanding into Special Needs Plans and final expense insurance, and dedicating resources to retaining existing policies underlying the Backbook Asset. The Company launched GoHealth Protect and initiated several reductions in force; however, new product investments had not yet grown sufficiently to offset the impact of declining MA demand on revenues and cash.

The Prepackaged Plan

With no viable third-party transaction materializing and its liquidity position continuing to deteriorate, GoHealth exhausted its strategic alternatives and ultimately determined that a prepackaged Chapter 11 restructuring was the best path forward to deliver a comprehensive solution — one that could preserve enterprise value, protect critical Carrier relationships, and position the Company for the 2026 AEP ahead of the August 1 pre-AEP period.

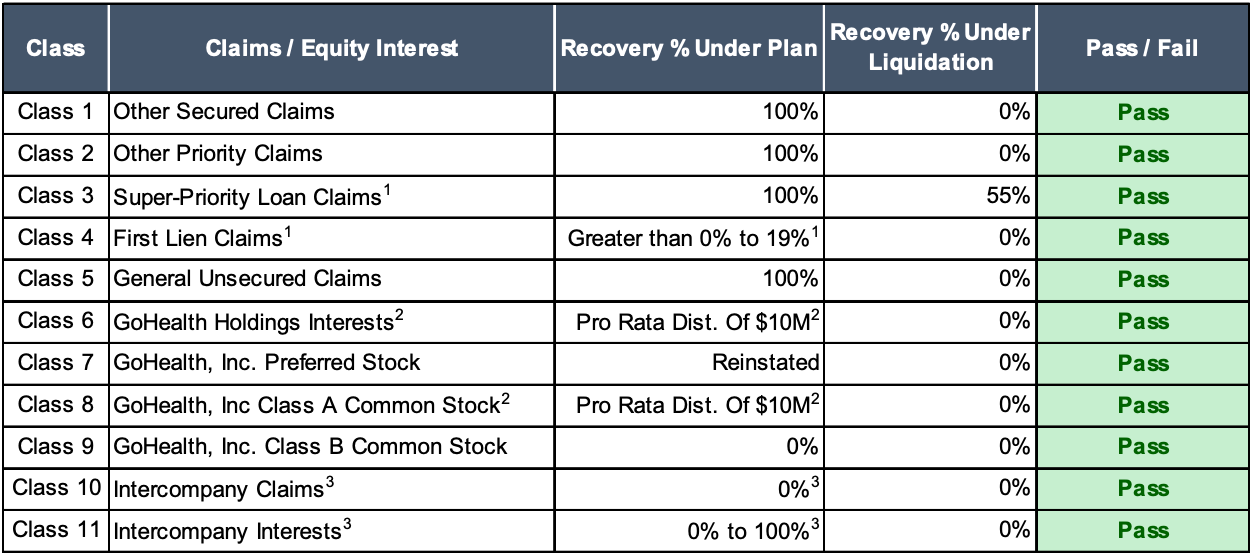

The Plan arrived with support from 100% of prepetition lenders, 61% of the Class A common stockholders, and holders of 99.45% of the GoHealth Holdings units. It hands the First Lien lenders 100% of the new common equity (subject only to MIP dilution) and converts the entire funded stack into a three-tranche exit structure maturing July 17, 2031: a $20 million first-out new-money facility (Term SOFR + 550 cash pay, 2.0x MOIC) that funds the $10 million Equity Recovery Pool; a $173.9 million cash-pay second-out tranche for Super-Priority lenders; and a ~$588.3 million PIK third-out tranche for First Lien lenders—all amortizing through a monthly sweep of cash above $10 million plus one month of expenses. The junior-stakeholder architecture is deliberate. The Series A preferred—held 70% by Anthem (Elevance)—rides through reinstated as preferred LLC interests, underscoring how the Plan protects the Carrier relationships on which the run-off depends.

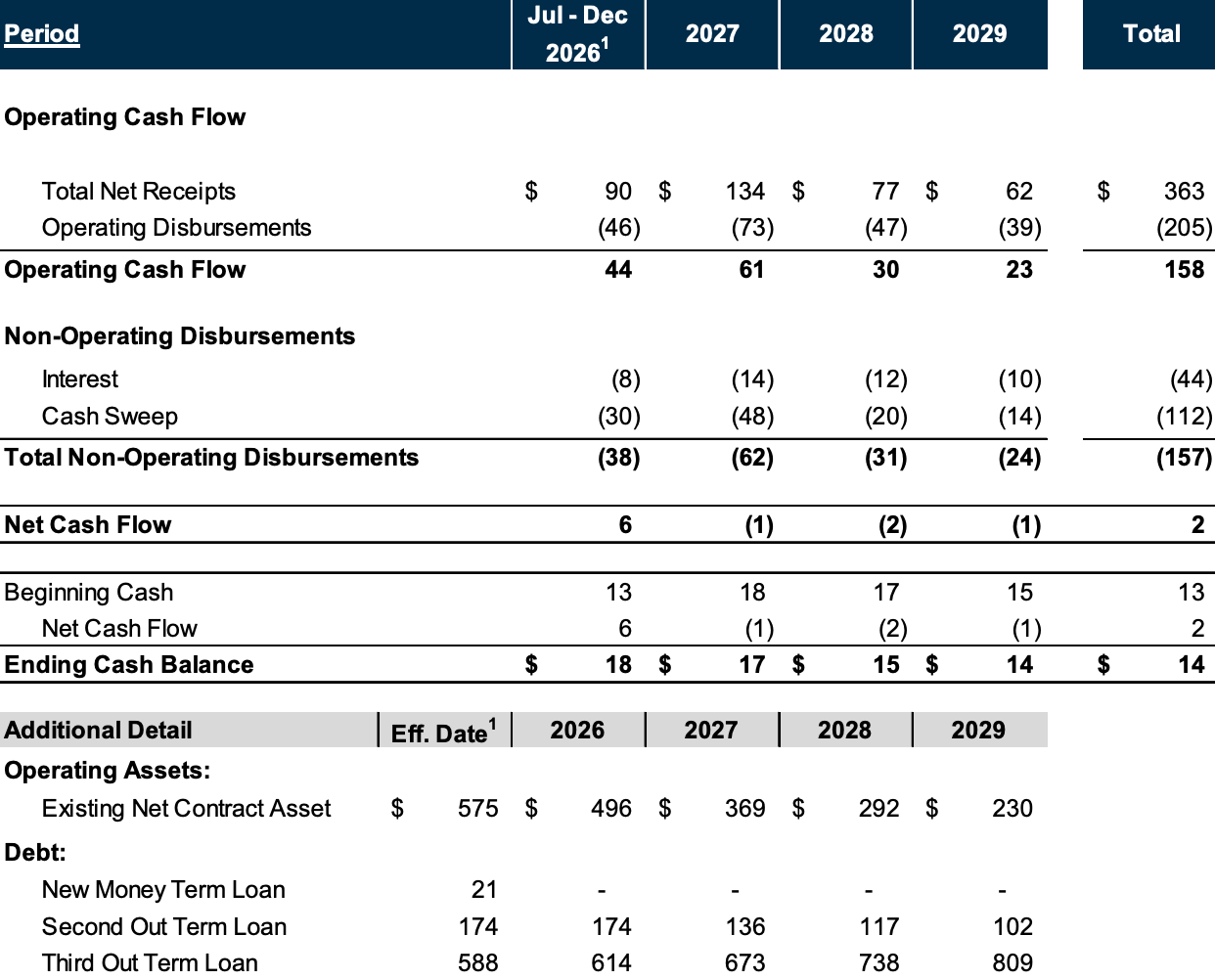

The Disclosure Statement's projections are the case's most consequential strategic disclosure — and the clearest signal of what Reorganized GoHealth actually is. The base case is not a turnaround; it is a harvest. The projections assume no new sales and no growth — simply the systematic collection of renewal commissions on existing policies until the book runs off. Starting from a $575 million Existing Net Contract Asset at emergence, the backbook declines to roughly $230 million by year-end 2029, generating $363 million of net receipts against $205 million of disbursements over that period, with servicing outsourced to a third party from July 2027. At that point Reorganized GoHealth becomes less an operating company than a passive collection vehicle for a depreciating asset.

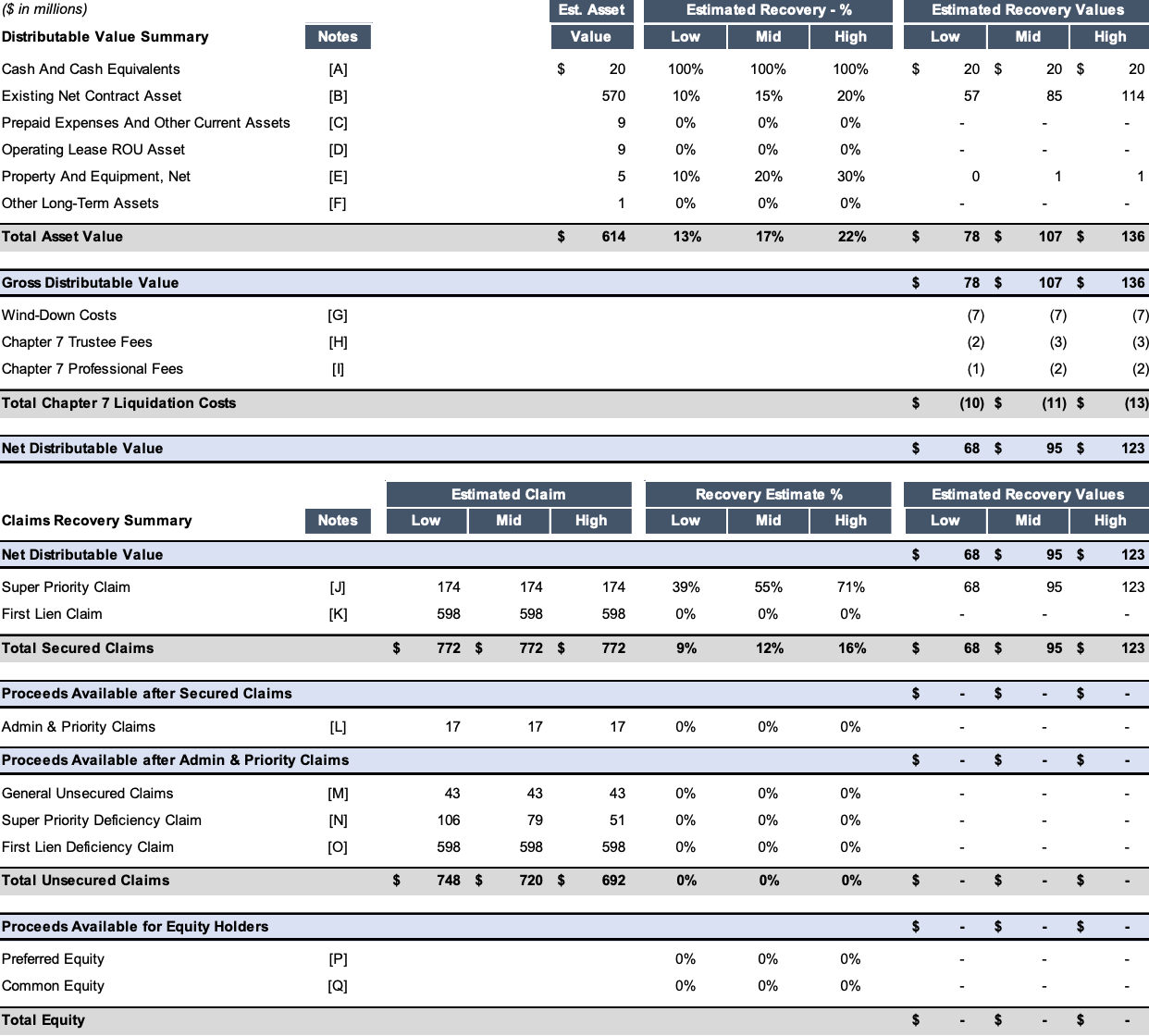

Illustrative Liquidation Analysis

The liquidation analysis frames the lenders' implicit justification for the deal: a forced Chapter 7 sale of the backbook would fetch only 10–20% of the Existing Net Contract Asset value (estimated at ~$570 million at the Sale Date), leaving Super-Priority recovering 39–71 cents on the dollar and every junior class at zero.

Recoveries Against Hypothetical Chapter 7 Liquidation

Case Timeline, Financing, and First Days

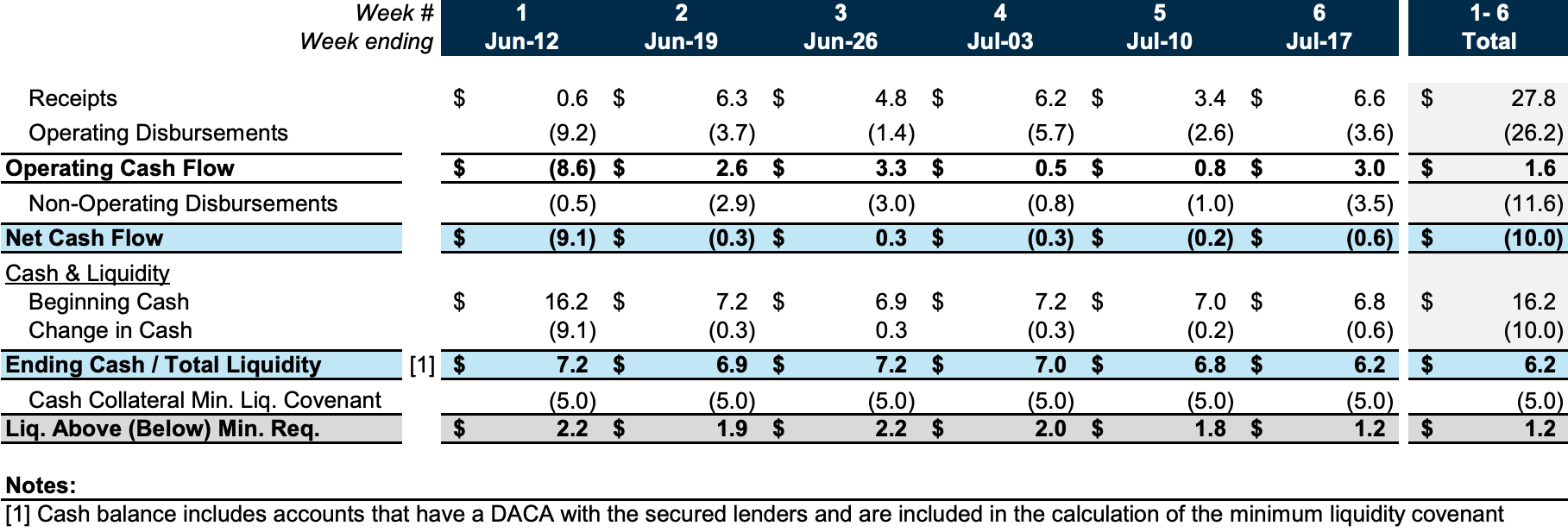

There is no DIP. The Debtors entered Chapter 11 with approximately $17.7 million of cash — all encumbered — and are funding the case through consensual cash collateral use with 100% lender consent. The six-week budget projects beginning cash of $16.2 million declining to roughly $6.2 million at the week-six trough against a $5.0 million minimum-liquidity covenant — approximately $1.2 million of headroom at the trough — subject to weekly variance tests requiring receipts of at least 90% and disbursements no greater than 110% of budget. Adequate protection comprises replacement liens, section 507(b) superpriority claims, and lender professional fees, but no cash interest.

The entire case is engineered around a single operational constraint: emergence before the pre-AEP ramp that begins August 1. Equity voting, release opt-ins, and plan objections are due July 8; the combined disclosure statement and confirmation hearing is set for July 16 — 39 days after filing — with a targeted Effective Date of July 17. Cash collateral milestones supply the timeline discipline: interim order within three business days of filing, final cash collateral order by July 17, confirmation order by July 27, and effectiveness by July 31, extendable 60 days at the Required Lenders' option.

The first-day program reflects the prepack's ride-through design. Judge Horan's June 9 hearing ran approximately 48 minutes with no objections from the U.S. Trustee or any other party, and all motions went forward on an interim or final basis. Relief is unusually creditor-friendly: rather than a capped critical-vendor program, the Debtors sought authority to pay all approximately $46 million of prepetition trade claims in full in the ordinary course, and a carrier-programs motion modifies the automatic stay to allow the approximately 10 Carriers representing over 95% of revenue to continue netting chargebacks against ongoing commission payments — protecting the backbook's gross-to-net spread on which the entire run-off thesis depends.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.