Case Summary: GoldenPeaks Poland Chapter 11

GoldenPeaks Poland filed for Chapter 11 to pursue a Brookfield-funded sale process or reorganization plan after the collapse of its in-house operating arm, Polish grid curtailment, and failed financing efforts contributed to a liquidity crisis.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Pieta, Malta, GoldenPeaks Poland Holding Limited ("Debtor TopCo"), along with its Debtor⁽¹⁾ and non-Debtor affiliates (collectively, "GoldenPeaks" or the "Company"), is the holding company for the Polish solar photovoltaic ("PV") and battery energy storage ("BESS") business of GoldenPeaks Capital ("GPC"), a Malta-based renewable-energy independent power producer ("IPP") and trader, and the largest owner of solar photovoltaic assets in Poland.

The Debtors were part of a larger GPC group that handled all operational services — development, construction, financing, energy sales, etc. The entity that provided those services has collapsed. To survive, the Debtors had to break away from the group and stand up as an independent company around their Polish solar assets.

GoldenPeaks Poland Holding Limited and certain affiliates filed for Chapter 11 protection on May 29, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Southern District of Texas, reporting $1 billion to $10 billion in assets and $500 million to $1 billion in liabilities.

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History & Corporate Structure

GPC was founded in 2006 by Adriano Agosti and Daniel Tain to develop, finance, own and operate solar projects in Eastern Europe. The founders built GoldenPeaks to be vertically integrated across the full renewable energy value chain. Since inception, the Company has developed an operational portfolio of 0.7GW of solar photovoltaic power, a further 1.4GW of financed and under construction solar power projects, targeting 2.1GW of solar power generation, and over 1.5GWh of battery energy storage systems with capacity market contracts. Over the course of two decades, GoldenPeaks has become the largest solar photovoltaic owner-operator in Poland with seven operational projects, three partially operational or in-construction projects, and five ready-to-build projects (each, a “Solar Project”).

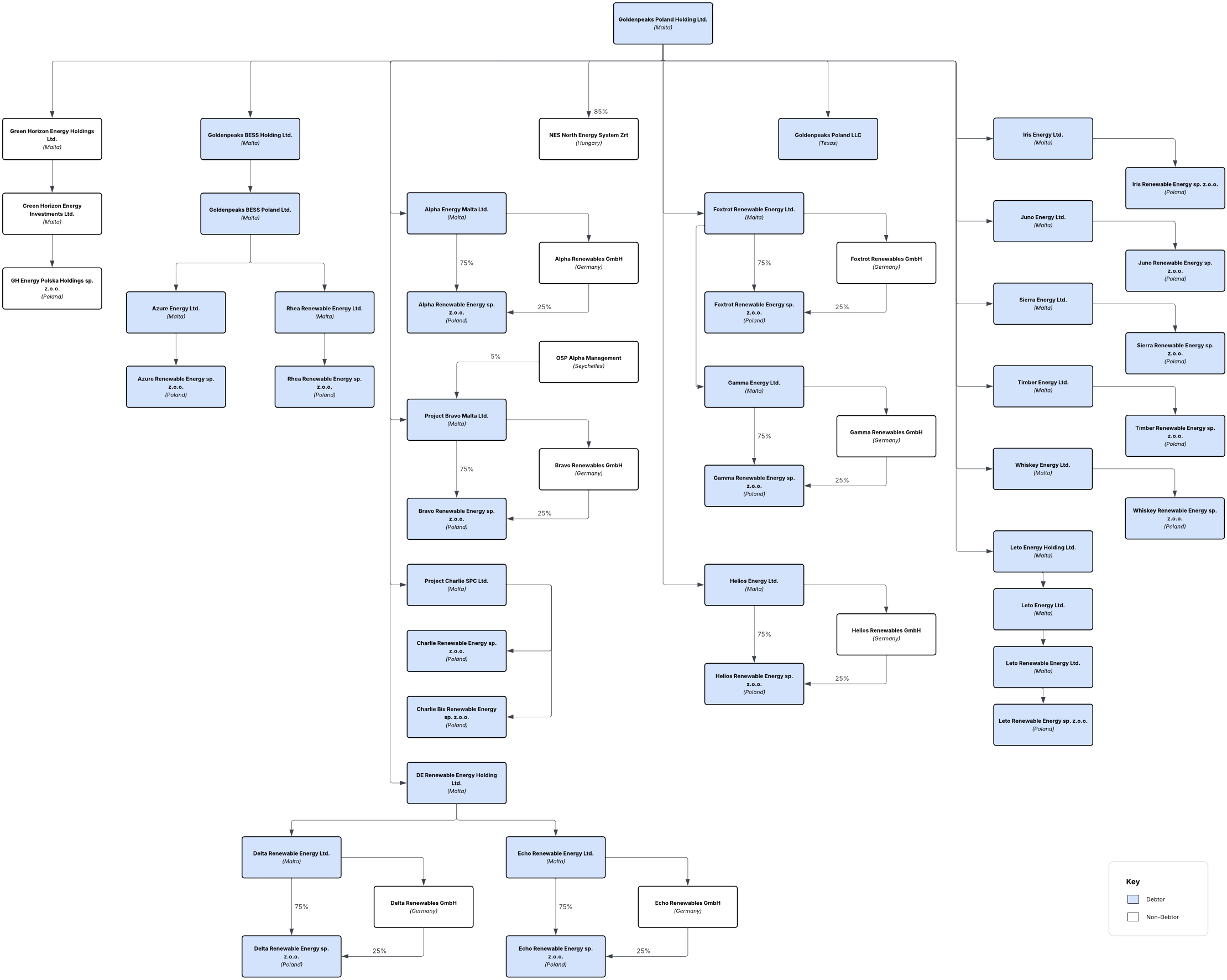

Organizational Structure

The Company has roughly 368 entities in total, of which 40 have filed for Chapter 11. According to the First Day Declaration, the Debtors anticipate more entities may file in the coming days and weeks. The Debtors are incorporated across Malta, Poland, and the United States.

Operational Structure

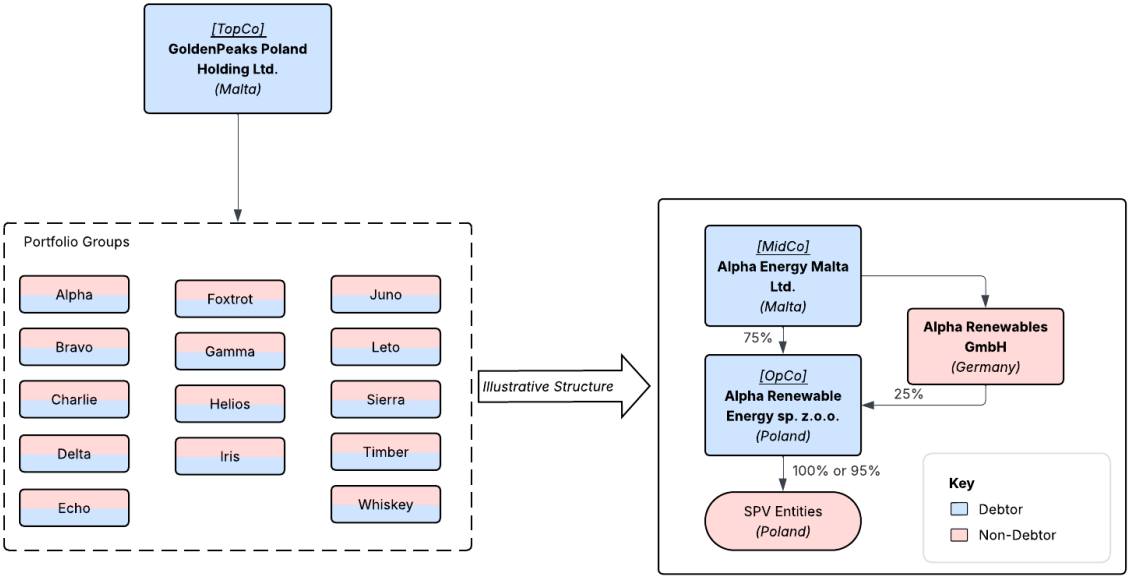

The Debtors' operational assets — the Solar Projects — are organized into 14 sub structures (each, a "Portfolio Group"). The Portfolio Groups sit below Debtor TopCo. Each Portfolio Group follows a consistent three-tier structure: (a) one or more Maltese limited liability companies serving as secondary-level project holding companies ("MidCos"); (b) one or more Polish limited liability companies serving as project-level operating companies ("OpCos"); and (c) between four and twenty Polish limited liability companies serving as special purpose vehicles ("SPVs") that directly hold the individual solar projects. Through the Portfolio Groups, the Debtors’ primary assets are generally the Solar Projects in Poland (the “Poland Portfolio”). The Poland Portfolio today consists of 9 operational Portfolio Groups with 664 MWp of installed capacity, plus 5 additional Portfolio Groups in various stages of development with over 500 MWp in the pipeline. In total, the Poland Portfolio spans 548 individual solar projects held across approximately 136 non-Debtor SPVs, with the underlying solar farms operating under Poland's Renewable Energy Sources regulatory framework.

Operations Overview

GoldenPeaks’ business was designed to provide a full suite of capability through the renewable energy life cycle, including (a) development, (b) engineering, procurement, and construction (“EPC”), (c) offtake (power sales), and until recently (d) operations and maintenance.

The Debtors own assets but employ no one — and with the collapse of Spectris Energy, the group's in-house EPC/O&M arm, the entire 664 MWp operating portfolio now runs on a single asset-management agreement signed sixteen days before the petition.

Project Lifecycle

A depiction of the project life cycle is below, with the key stakeholders representing the non-Debtor affiliates that historically have been responsible for the stage of the life cycle from inception, to Ready-to-Build (“RTB”) to Commercial Operation Date (“COD”).

- Development — The first phase of a project's life cycle involves identifying suitable land, conducting analyses, and securing land rights, permits, and contractual arrangements. This work is carried out by non-Debtor affiliate Mercer Solar sp. z o.o., which engages contractors and vendors to support land leasing, engineering studies, and environmental due diligence. The development phase also includes project structuring, where the Company enters into power purchase agreements ("PPAs") with corporate offtakers, private companies, and government entities — a function historically performed by non-Debtor affiliate GoldenPeaks Capital Trading. PPA counterparties have included large corporations such as Nestle, Mondelez, and Auchan. The Company also enters into interconnection agreements to connect completed projects to the electrical grid.

- EPC & Construction — Once development is complete, a project enters the EPC phase. The Company historically contracted with China National Building Material Group Corporation ("CNBM") as its third-party EPC provider, with CNBM providing a performance guarantee and receiving milestone-based payments. CNBM would historically subcontract the on-the-ground construction work to non-Debtor affiliate Spectris Energy sp. z o.o. ("Spectris").

- Operations — Once constructed, a project commences commercial operations, generating revenue under its associated PPA, paying project-level operating expenses including O&M and insurance, and servicing project-level debt. The Company may sell a project, or an interest in a project, to a third-party operator with the sale proceeds being used by the Company for development and operation of other projects. In 2025, the Company generated $63 million in revenue from power sales and recorded no project sales during that period.

- Historical Operations & Maintenance — O&M services were historically provided through Spectris. In January 2026, Spectris applied for remedial proceedings in Poland following increases in component costs, higher interest rates, and exchange rate fluctuations. Its bank accounts were subsequently frozen by Polish tax authorities and suppliers ceased doing business with it, rendering Spectris non-functional.

Transition to a Single Operator

Prior to the filing, the Debtors had no independent operational capability. The platform ran entirely on a roster of non-Debtor affiliates: GoldenPeaks Capital Services (Malta) for group accounting, tax, and legal support; GoldenPeaks Advisers (London) for financing and structuring; GoldenPeaks Capital Trading (Switzerland) for PPA negotiations, with approximately 500 MW secured under Polish RES auctions; Mercer Solar (Warsaw) for land leasing, permitting, and entitlement; and Spectris Energy (Warsaw) as the operating backbone, serving as the wholly owned EPC, O&M, and green credit trading business. EPC work was contracted to CNBM, which provided a performance guarantee and historically subcontracted execution to Spectris. The Debtors themselves had no employees and were entirely dependent on this affiliate network to keep the assets running.

The collapse of Spectris — now in Polish remedial restructuring following frozen bank accounts, unpaid tax liabilities, and supplier walkouts — removed the operational infrastructure from beneath the Debtors and served as the proximate trigger of the Chapter 11 filing. With the wider GPC group no longer able to provide critical services, the Debtors had no choice but to separate and establish an independent operating model.

With the support of Brookfield, the Debtors have begun replacing the defunct affiliate network with independent third-party providers. On May 13, 2026, Debtor TopCo entered into an Asset Management Agreement with Ergy sp. z o.o. ("Ergy"), a Polish asset management company, which now serves as the Debtors' sole on-the-ground operational manager for the entire Poland Portfolio. Ergy provides two integrated categories of services: commercial asset management — covering day-to-day portfolio management, financial and operational reporting, contract management, invoice approval, revenue management, and regulatory compliance; and technical asset management — covering SCADA-based performance monitoring, O&M supervision and dispatching, warranty management, and insurance administration. Ergy also serves as the primary point of contact with Polish regulatory authorities, offtakers, grid operators, and service providers, making its role critical to maintaining both the operating performance and regulatory standing of the Poland Portfolio during the pendency of these Chapter 11 Cases. In addition to Ergy, the Debtors are outsourcing the remaining back-office functions, including payment processing and bookkeeping to PricewaterhouseCoopers.

Hedging Agreements

The Debtors' solar projects are financed through project-level debt, which exposes them to interest rate risk relative to the long-term, predictable revenues generated under their PPAs. To manage this risk, the Debtors maintain two categories of hedging instruments.

- Financing Agreements — Derivatives contracts, the majority of which are interest rate swaps, under which the Debtors pay a fixed rate to counterparties calculated on a nominal principal amount corresponding to the applicable project-level debt, and in return receive a variable payment on the same nominal principal. These swaps create long-term cost certainty at the project level, ensuring projects can cover their interest obligations.

- Virtual Power Purchase Agreements ("Virtual PPAs") — A form of derivative contract under which the Debtors sell energy to a local utility at a floating market price. If the market price exceeds the strike price under the Virtual PPA, the buyer receives the difference; if the market price falls below the strike price, the buyer pays the Debtor the difference. In return, buyers receive Guarantees of Origin — certificates confirming that a given quantity of energy was produced from renewable sources — which are referred to in the United States as solar renewable energy credits. The Virtual PPAs reduce the Debtors' exposure to fluctuations in commodity prices, commodity volumes, and interest rates, providing long-term cash flow predictability.

As of the Petition Date, the Debtors have identified approximately $875,000 in prepetition amounts owing to counterparties under these hedging agreements. The First Day Declaration notes that the Chapter 11 filing may constitute an Event of Default under the Hedging Agreements, potentially allowing counterparties to terminate them if they fall within the Bankruptcy Code's safe harbor provisions.

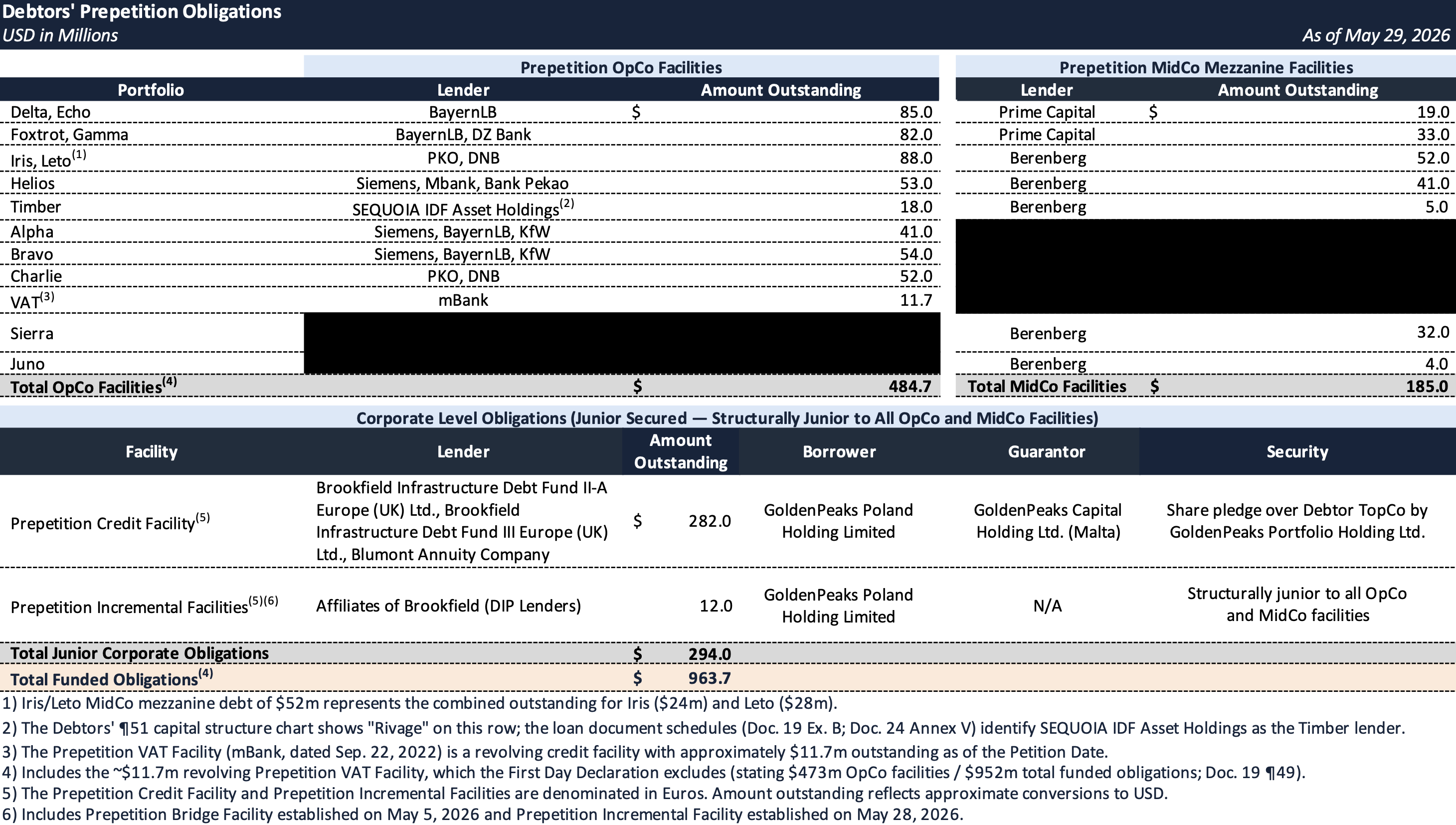

Prepetition Obligations

As of the Petition Date, the Debtors carried approximately $964 million in total funded obligations including accrued and unpaid interest, organized across three structural tiers ranked by proximity to the cash-generating solar assets.

- Senior Secured — OpCo-Level Facilities — Project-level debt advanced directly to the Polish OpCos, secured by the assets of the applicable OpCo Debtors including their equity interests in the non-Debtor SPVs. The lender group is dominated by European project finance banks. No guarantors are named at this tier in the Declaration.

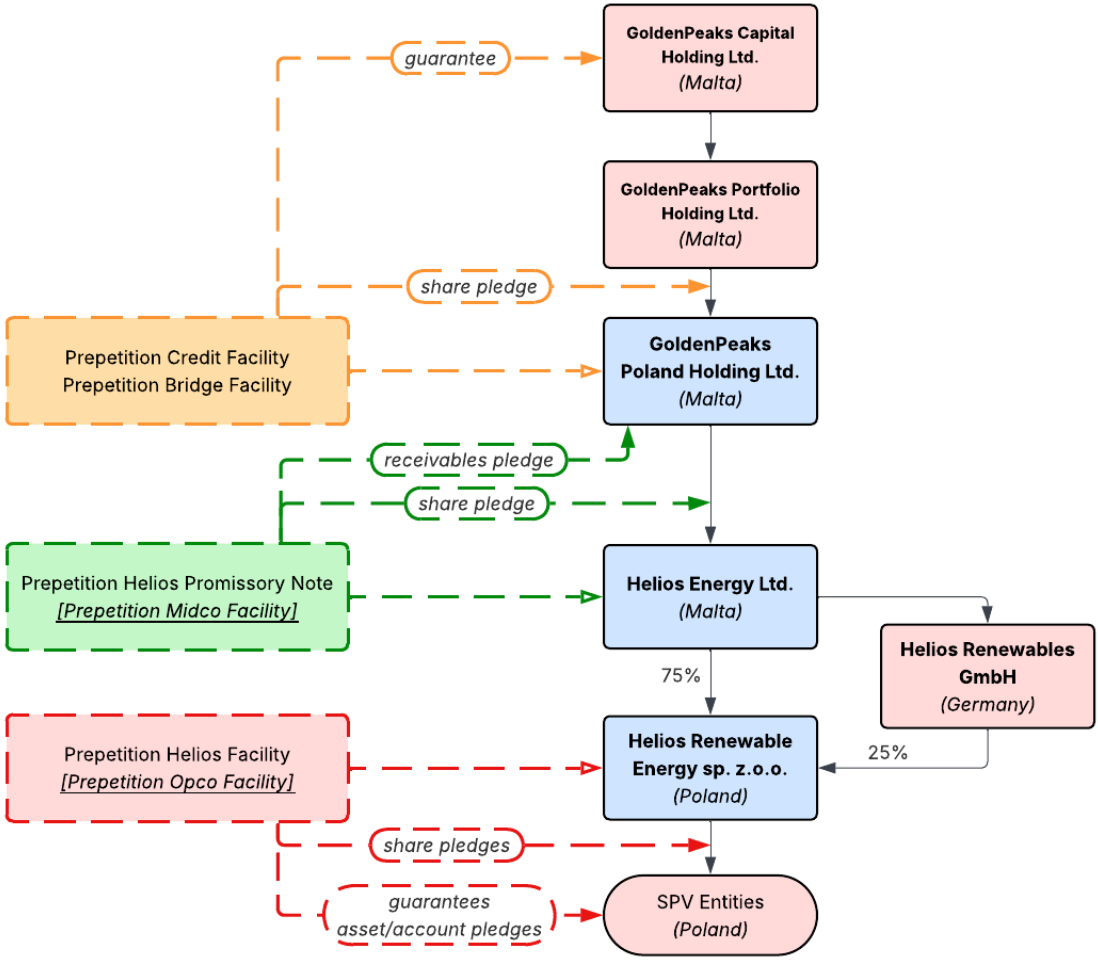

- Mezzanine Secured — MidCo-Level Facilities — Debt advanced to the Maltese MidCos, secured primarily by each MidCo borrower's equity interests in its corresponding Debtor and non-Debtor subsidiaries — mezzanine lenders can only reach project-level value after OpCo debt is fully satisfied. GoldenPeaks Capital acts as sponsor across all Berenberg Schuldschein facilities. Berenberg holds promissory notes against Helios Energy Limited ($41 million), Iris Energy Limited ($24 million), Leto Renewable Energy Limited ($28 million), Sierra Energy Limited ($32 million), Juno Energy Limited ($4 million), and Timber Energy Limited ($5 million). Prime Capital holds subscription agreements against Foxtrot Renewable Energy Limited ($33 million) and DE Renewable Energy Holding Limited ($19 million). No guarantors are named at this tier in the Declaration.

- Junior Secured — Corporate-Level Facilities — Corporate-level debt advanced directly to Debtor TopCo, structurally subordinate to all OpCo and MidCo facilities. The Prepetition Credit Facility ($282 million outstanding) is provided by Brookfield Infrastructure Debt Fund II-A Europe (UK) Limited, Brookfield Infrastructure Debt Fund III Europe (UK) Limited, and Blumont Annuity Company. Security consists of a share pledge over Debtor TopCo granted by GoldenPeaks Portfolio Holding Limited and a receivables pledge from Debtor TopCo; GoldenPeaks Capital Holding Limited provides a guarantee. The Prepetition Incremental Facilities were funded on May 6 and May 28, 2026 by the same Brookfield entities.

Illustrative Debt and Security Structure — Helios Portfolio Group

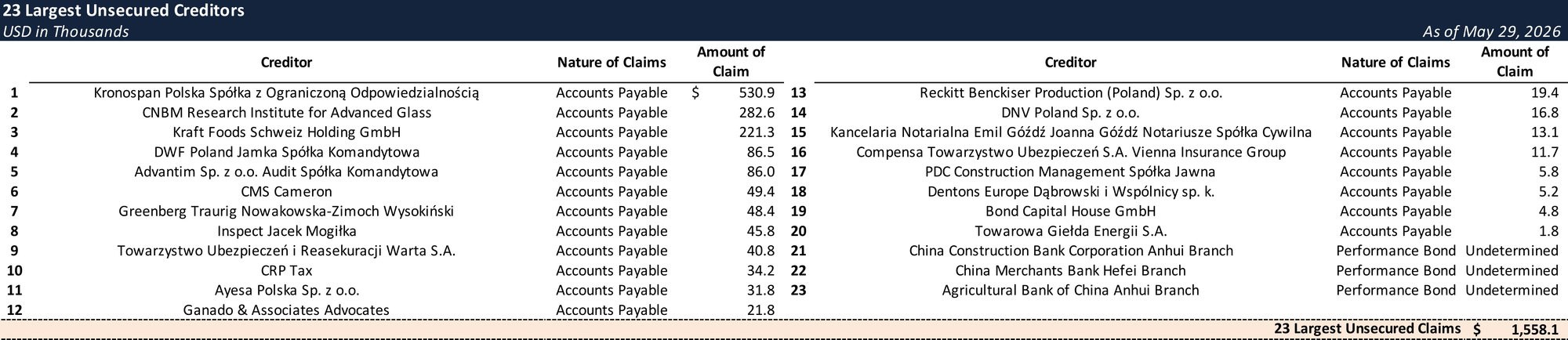

Top Unsecured Claims

Events Leading to Bankruptcy

GoldenPeaks did not fail one project at a time — between April and late May 2026, the platform unwound wholesale. The First Day Declaration attributes the collapse to four pressures: Polish grid curtailments, construction challenges and delays, a lack of equity funding and overhead out of line with revenue. In the First Day Declaration, A&M states that it has not been able to determine the full causes of the distress, given the absence of standalone Debtor financials.

Governance and Financial Control Failures

The foundation of GoldenPeaks' distress was a chronic failure of financial governance that predated the filing by years. The Company operated with multiple Chief Financial Officers holding overlapping mandates, decentralized and fragmented financial controls, no standalone financial statements for any Debtor entity, and a complete absence of budget reporting and construction cost supervision. Accounting ledgers had not been closed since December 2025 and fiscal year 2025 accounts remained unsigned as of the Petition Date. These deficiencies left the Company unable to identify or respond to escalating financial and operational stress in a timely manner, and ultimately contributed directly to the cascade of defaults that precipitated the Chapter 11 Cases. A&M has noted that, given the compressed timeframe in which the Chapter 11 Cases were commenced and the absence of reliable historical financial information, it has not yet been able to determine the full and true cause of the Company's sudden and significant distress.

Defaults Cascade

The financial and operational constraints described above triggered events of default under nearly all of the Company's 20-plus financial facilities. Outstanding payment defaults exceeded $25 million across 9 separate financial facilities. Beyond payment defaults, the Debtors incurred events of default for: failure to timely submit operating reports, budgets, and compliance certificates; commencement of insolvency proceedings by Spectris; failure to achieve project completion milestones; failure to resize certain financial facilities; financial covenant defaults including debt service coverage ratio breaches; and failure to achieve certain revenue targets under applicable PPAs.

Spectris Collapse

Spectris Energy sp. z o.o. was a wholly owned non-Debtor affiliate of GoldenPeaks and served as the operational backbone of the entire platform. It performed two critical functions simultaneously. First, it acted as the EPC subcontractor to CNBM — the Company's primary third-party EPC provider — handling the on-the-ground construction work across the Poland Portfolio. CNBM held the formal EPC contracts with the project owners, provided performance guarantees, and received milestone-based payments, but historically subcontracted the actual construction execution to Spectris. Second, Spectris operated the Company's O&M business, managing the day-to-day technical operations and maintenance of all operational solar projects across the Poland Portfolio. In short, Spectris was responsible for both building the assets and keeping them running once built.

In January 2026, Spectris applied for remedial proceedings in the District Court of Warsaw, Poland. According to the First Day Declaration, the following factors contributed to Spectris's financial distress: increases in component costs, higher interest rates, and exchange rate fluctuations. These pressures, compounded by material unpaid tax liabilities, rendered Spectris unable to continue operating. As a direct consequence of its financial distress, suppliers ceased doing business with Spectris and its bank accounts were frozen by Polish tax authorities — effectively shutting it down entirely.

The commencement of insolvency proceedings by Spectris was itself an explicit event of default under the Debtors' financing facilities. With Spectris non-functional, the Debtors were left without both an EPC subcontractor and an O&M provider — the two functions essential to completing projects under construction and maintaining operational projects. The Declaration states that the corporate entity providing those critical services was "now defunct" and could "no longer provide those critical services to preserve the Debtors' value".

Prepetition Restructuring Efforts

Faced with mounting financial and operational challenges, the Company pursued three parallel tracks during the second half of 2025 and into the first quarter of 2026 in an attempt to avoid insolvency: equity raises, strategic asset sales, and a full debt refinancing.

- Equity Raises & Asset Sales — The Company commenced three equity raise efforts in the second half of 2025. In July 2025, the Company entered into discussions for the sale of all or a portion of the business, though no formal sale process was run. Despite receiving indications of interest from at least one credible Middle East-based investor, the process was unsuccessful. Between September 2025 and February 2026, the Company explored multiple debt-to-equity solutions with a number of parties, which also proved unsuccessful. Finally, with the support of a global investment bank — which notably did not sign a formal engagement agreement — the Company launched a broad formal equity raise process targeting the sale of up to 50% of the Company's equity to a wide range of potential investors. This process was paused in the first quarter of 2026 due to an absence of material progress.

- Refinancing Efforts — In June 2025, the Company simultaneously commenced a refinancing process targeting all junior and senior debt positions across its asset portfolio, contemplating that a single institution or syndicate would refinance the full debt stack. Banks received an initial request for proposal in June 2025 and a preferred bidder was selected in September 2025. While that bidder subsequently required an additional syndicating party, a number of credit approval stages were completed successfully in the first quarter of 2026. Ultimately, however, the refinancing failed given the overall level of distress across the business.

Emergency Bridge Financing

Shortly after A&M's engagement, it became clear the Company faced severe liquidity constraints, with insufficient cash to cover salaries, IT, rent, and taxes. Vendors were owed more than $81 million — including $1 million for critical leases — and construction projects were on hold. By April 15, 2026, the Company held less than €1.1 million of unencumbered cash – insufficient to cover overhead expenses or the mounting defaults cascading across its financing facilities.

The Company sought emergency liquidity from existing junior creditors. Ultimately, Brookfield was the only party willing to provide financing, executing the Prepetition Bridge Facility on May 5, 2026. Brookfield and certain Prepetition MidCo Lenders entered into a standstill agreement in connection with the Prepetition Bridge Facility, expiring May 31, 2026. The proceeds covered past-due salaries, restructuring advisory fees, and overhead, but were insufficient to fund another month of operations.

On May 16, 2026, Brookfield confirmed it would no longer fund non-Debtor expenses, prompting certain Prepetition Lenders to commence insolvency proceedings against non-Debtor entities in local European jurisdictions. Brookfield separately confirmed its willingness to fund the Debtors on a standalone basis, but the Prepetition MidCo Lenders refused to extend the standstill beyond May 31, 2026. On May 28, 2026 — one day before the Petition Date — Brookfield provided an additional Prepetition Incremental Facility, the obligations of which are proposed to be rolled up into the DIP Facility.

Nexus to the United States and Texas

Neither Poland nor Malta offered a viable restructuring path. Poland's superpriority financing mechanism has never been deployed at this scale and, critically, does not stay out-of-court enforcement by secured creditors — leaving lenders free to seize pledged shares in the project companies notwithstanding any proceeding. Malta's Pre-Insolvency Act, in force only since December 2022 and used just once, offered no meaningful precedent. Chapter 11 was the only framework capable of simultaneously delivering the automatic stay, DIP financing, and value-preservation tools the situation demanded.

To establish US nexus, each Debtor shares a JPMorgan Chase escrow account in Houston (~$35,000 aggregate), a $100,000 retainer was funded to bankruptcy counsel at Wells Fargo in Houston, and Debtor TopCo formed GoldenPeaks Poland LLC — a Texas LLC maintaining an office at 801 Louisiana Street, Suite 368, Houston — prior to filing.

DIP Financing

On June 3, 2026, the Debtors filed their emergency motion seeking approval of a $162.8 million junior secured superpriority delayed-draw DIP term loan provided by Brookfield-managed funds, comprising up to $150.7 million of new money and an approximately $12.1 million cashless roll-up of the Prepetition Bridge and Incremental Facilities, with BID Administrator LLC — a Brookfield affiliate — acting as DIP Administrative Agent. The DIP Facility further entrenches Brookfield's position across every layer of the capital structure: most junior prepetition lender (~$294 million), bridge and incremental lender, DIP lender and agent, holder of two of five board seats, and prospective credit-bid acquirer.

- Committed Liquidity: Of the $150.7 million in new money commitments, $92.9 million constitutes "Discretionary Delayed Draws" available solely for construction and development expenses and only with the prior written consent of the Required DIP Lenders. Stripping out the discretionary tranche, committed new money is approximately $57.8 million, with $34.8 million available on the interim order and $23.0 million on the final order.

- Loan Parties: Debtor TopCo (GoldenPeaks Poland Holding Limited) is not a DIP Loan Party and receives no DIP liens or proceeds. The 18 DIP Loan Parties consist of the 17 Polish OpCo Debtors and GoldenPeaks Poland LLC, the Texas subsidiary.

- Economics: The DIP Facility carries 13.00% PIK interest, plus a 3.00% default rate upon an Event of Default. Additional economics include a 5.00% original issue discount fully earned on the first draw, a 6.50% PIK ticking fee on all committed and undrawn amounts, and a 1.75x Prepayment Multiple — a MOIC-style mechanism fully earned as of the date of the first drawing. A 5.00% Exit Premium is also payable, which, in the event of a credit bid by a DIP party, shall be applied to such credit bid rather than paid in cash. The DIP Facility matures three months from the closing date.

- Non-priming: The DIP Facility is non-priming. DIP liens are expressly junior to the Prepetition OpCo Facilities, take first-priority only on unencumbered assets of the DIP Loan Parties, and prime only intercompany and affiliate liens. The senior project finance lenders — BayernLB, Siemens Bank, DNB, PKO, mBank, Bank Pekao, and others — retain their structural priority ahead of the DIP in all respects.

- Sale Milestones: The DIP Facility includes sale milestones exercisable at Brookfield's option. If elected by the Required DIP Lenders, the Debtors must obtain a Bidding Procedures Order within 15 days of entry of the Interim Order, and a Sale Order within 30 days of entry of the Bidding Procedures Order. A qualifying sale must generate net cash proceeds sufficient to repay all DIP Loans and other DIP obligations in full (an "Acceptable Sale"). Failure to meet any milestone constitutes a "Milestone Event of Default," which automatically suspends all remaining DIP commitments and triggers a mandatory expedited-sale track.

- Credit Bid: The DIP Administrative Agent holds the right to credit bid up to the full amount of the DIP obligations in any sale of DIP collateral, without the need for further court order. The credit bid right is subject to one constraint: the Incremental Roll-Up Loans may not be included in a credit bid unless all allowed unsecured claims against the applicable Debtor are paid in full.

- Challenge Dynamics: The Debtors stipulate to the validity and enforceability of the Brookfield prepetition debt and release the Brookfield Secured Parties upon entry of the Interim Order, subject to challenge windows of 60 days for any Creditors' Committee (running from committee appointment) and 75 days for all other parties in interest (running from entry of the Interim Order). The committee's investigation budget is capped at $25,000. The DIP Orders also provide for waivers of the Debtors' rights under Bankruptcy Code sections 506(c) and 552(b) and the equitable doctrine of marshaling; at the interim stage, these waivers apply only as against the DIP collateral and the DIP Secured Parties, with the 552(b) and marshaling waivers as to the Brookfield prepetition secured parties — and the 506(c) waiver as to the Prepetition Collateral — becoming effective only upon entry of the Final Order.

- Adequate protection: The DIP papers leave adequate protection "provided, if any, subject to ongoing diligence and negotiation", with no replacement liens or superpriority claims under section 507(b) granted at the interim stage, and any such protection gated behind the consent of the Required DIP Lenders. This leaves the structurally senior, non-Brookfield secured parties — the Prepetition OpCo lenders ($473 million) and Prepetition MidCo/Mezzanine lenders ($185 million) — without resolved adequate protection as of the filing date. While the DIP does not prime their liens, the absence of agreed adequate protection terms is arguably the largest open economic issue in the case.

Prime Capital Settlement and DEFG DIP Terms

At the June 3 first day hearing, Brookfield and Prime Capital reached a settlement — announced on the record before the DIP presentation proceeded — creating a separate sub-facility within the broader DIP covering the Delta, Echo, Foxtrot, and Gamma OpCos, the four Polish operating companies where Prime holds mezzanine debt at the MidCo level. The settlement was negotiated over the course of the hearing itself and read into the record by Evan Fleck of Milbank on behalf of Brookfield, and confirmed by David Turetsky of White & Case on behalf of Prime Capital. The DEFG DIP carves out $33 million from the $92.9 million discretionary delayed draw tranche of the broader DIP — it is not additional new money on top of the $162.8 million facility, but a ring-fenced allocation within the existing discretionary pool. Brookfield funds the full $33 million upfront upon court approval. Prime then has five business days to reimburse up to $10 million by taking a silent sub-participation in Brookfield's position — Prime is not a named lender on the face of the facility; its relationship is with Brookfield, not the Debtors. If actual borrowings at the four entities fall below $33 million, Prime's entitlement scales down proportionally. Key structural and economic terms of the DEFG DIP are as follows:

- Funded at the OpCo level; junior to existing OpCo lenders; not cross-collateralized to any other OpCo Debtors

- 12.5% interest rate (vs. 13.0% under the broader DIP)

- 1.5x MOIC (vs. 1.75x under the broader DIP)

- No OID, no ticking fee, no exit premium, no roll-up

- Terms carry through into an exit facility on the same basis

Berenberg Reservation of Rights

Berenberg, the German mezzanine lender holding promissory notes against six MidCo entities, emerged as the most adversarial creditor at the June 3 hearing. Berenberg's counsel — retained that same day — confirmed Berenberg received no advance notice of the DIP terms, reserved all rights including jurisdiction and venue challenges, and flagged several DIP provisions as impairing its position: structural subordination to the DIP, the Brookfield roll-up, cross-collateralization without a Prime-style carve-out, and no adequate protection. Debtors' counsel further disclosed a potential automatic stay violation by Berenberg in the days following the petition, and described the Berenberg projects as the most distressed in the portfolio. With no settlement reached and adequate protection terms entirely unresolved, Berenberg's objections are expected to crystallize at the June 30 final hearing.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.