Case Summary: Pacifica Hospital of the Valley Chapter 11

Pacifica Hospital of the Valley, a Los Angeles safety-net hospital, filed for Chapter 11 to halt a creditor's contested loan-to-own bid for control and a pending receivership, after a liquidity crisis, pandemic costs, seismic-retrofit fines, and delayed government payments eroded operations.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Sun Valley, CA, Pacifica of the Valley Corporation, doing business as Pacifica Hospital of the Valley (the "Debtor" or the "Hospital"), is an integrated healthcare system that has delivered more than $3.3 billion in care to its patients over three decades.

Approximately 84% of the Debtor's patients live at or below the poverty line, making the Debtor heavily reliant on Medi-Cal, California's Medicaid program. Medi-Cal accounts for roughly 85% of the Debtor's total revenue and patient volume — about half of inpatient revenue comes directly from Medi-Cal, with a substantial additional share through Medi-Cal Managed Care. Medi-Cal patients make up 81% of the Hospital's population, and the Hospital functions as a safety-net provider serving low-income, uninsured, and vulnerable populations in the Sun Valley area.

At the core of the business is a 231-bed acute care hospital that serves a 13-zip-code catchment across the San Fernando Valley and treats more than 50,000 emergency patients a year — among them some of the most seriously ill and injured in Los Angeles. The Hospital offers a full continuum of inpatient and outpatient care, spanning 24/7 emergency and intensive care, a locked behavioral health unit, a distinct-part subacute skilled nursing facility, and outpatient surgery, imaging, and rehabilitation.

Pacifica of the Valley Corporation filed for Chapter 11 protection on July 4, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the District of Delaware, reporting $50 million to $100 million in assets and $100 million to $500 million in liabilities.

Corporate History

Pacifica has served the San Fernando Valley for more than three decades: a privately held safety-net hospital wholly owned by Executive Chairman and sole shareholder Paul R. Tuft, who also serves as Executive Chairman of Scottsdale, AZ-based Southwest Healthcare Services.

2002 Bankruptcy Filing

Pacifica Hospital of the Valley began as a physician-owned hospital in Sun Valley, CA, and passed into the orbit of Paul R. Tuft in 1996, when it was acquired by Doctors Community Healthcare Corporation, Tuft's Scottsdale, AZ hospital company, in a deal in which the sellers were Pacifica's physician owners.

Doctors Community's growth was underwritten by National Century Financial Enterprises (NCFE), a Dublin, OH healthcare-finance firm that advanced hospitals cash against the payments they were still waiting to collect from insurers and Medicare, funding those advances by selling bonds to investors. NCFE was not just Doctors Community's lender but a part-owner of it, and Doctors Community came to owe NCFE more than $400 million. That relationship sat at the center of what became one of the era's largest corporate frauds: as the U.S. Department of Justice later established, NCFE misused investor money to make unsecured loans to providers its own owners had stakes in, hid the shortfalls with falsified records, and ultimately cost investors more than $2 billion; NCFE's CEO was sentenced to 30 years in prison.

Because Doctors Community depended on NCFE's continuous advances for its day-to-day operating cash, NCFE's collapse in November 2002 cut off its lifeline: Doctors Community filed for Chapter 11 that same month, and Pacifica of the Valley Corporation was swept in alongside it as one of the jointly administered co-debtors in that case. That bankruptcy also laid bare how Doctors Community had been run. As The Washington Post reported, Paul Tuft and his executives had drawn lavish pay and placed family members throughout the company while overhead swelled to roughly $21 million a year.

2009 Bankruptcy Filing

Seven years after the 2002 filing, Pacifica of the Valley Corporation filed Chapter 11 on February 17, 2009 in the U.S. Bankruptcy Court for the Central District of California. This time the case was Pacifica's alone rather than a corner of a sprawling multi-hospital collapse: the plan was confirmed on December 27, 2010, and the case closed by final decree on December 7, 2017, following the debtor's discharge on November 28, 2017.

In the 2009 case, Pachulski Stang Ziehl & Jones represented the Official Committee of Unsecured Creditors, with Samuel Maizel among its lawyers before he moved to Dentons in 2015. Both firms now advise the Debtor — the same professionals who once pressed creditors' claims against Pacifica are now guiding its estate.

Southwest Healthcare Services

Following the Doctors Community Healthcare Corporation bankruptcy, Tuft rebuilt his hospital operations around the entities that survived rather than under the old name. In the years that followed, Doctors Community's Washington, D.C. flagships — Greater Southeast Community Hospital and Hadley Memorial Hospital — and most of its portfolio were sold off or closed, while a smaller group of hospitals, including Pacifica of the Valley Corporation, remained under Tuft's control. He later consolidated them under a new vehicle, Southwest Healthcare Services LLC, a company formed around 2010 and based, like Doctors Community before it, in Scottsdale, AZ.

Although the first-day declaration describes the Debtor as wholly owned and controlled by Paul Tuft as its sole shareholder, it does not mention Southwest Healthcare Services — the Tuft-affiliated management company that, according to Becker's Hospital Review in 2023, "currently manages" Pacifica of the Valley Hospital.

Southwest's stewardship of Pacifica has not gone unexamined. When Southwest moved in 2023 to acquire Mad River Community Hospital in Northern California, the Lost Coast Outpost scrutinized the track record of Pacifica's owners and reported a troubling picture. It found that Pacifica carried a one-star federal (CMS) rating, drew state survey deficiencies at roughly double the rate of comparable hospitals over four years, and was repeatedly penalized by Medicare for excessive hospital-acquired conditions and patient readmissions. The article also recounted Pacifica's two settlements over allegations that it had dumped mentally ill patients — a combined $1.5 million, paid without admitting wrongdoing ($500,000 in 2014 and $1 million in 2016). The nurses' union called it alarming that owners with a history of mismanagement and apparent financial problems at Pacifica would seek to acquire yet another facility.

Other Hospital Closures

Other hospitals operated by Tuft have also closed or entered bankruptcy in recent years. In September 2014, Southwest Regional Medical Center in Georgetown, OH — the former Brown County General Hospital — closed abruptly, giving patients and staff roughly two hours' notice after a debt dispute left it unable to make payroll. The following year, FBI agents searched its shuttered offices under a sealed warrant, seizing computers and records. Another hospital, Gulf Coast Medical Center in Wharton, TX, owned by Tuft, stopped accepting ambulances in early 2016, forcing costly diversions on the surrounding county, and closed that November before filing for bankruptcy. The Chief Restructuring Officer for Gulf Coast Medical Center was Alan Tuft, Paul Tuft's brother.

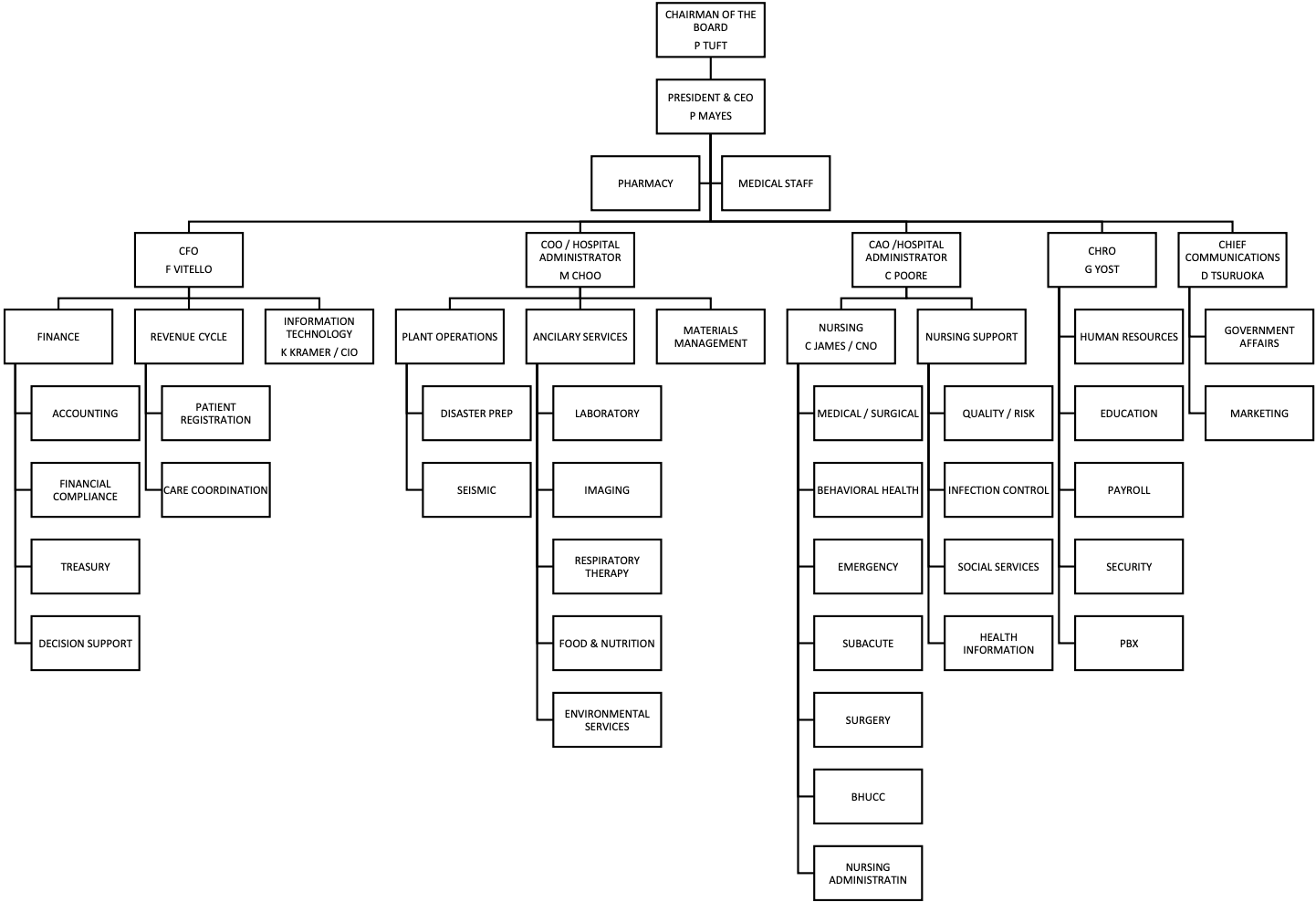

Corporate Structure

Operations Overview

Facilities and Programs

- Hospital — A 231-bed acute care safety-net facility at 9449 San Fernando Road in Sun Valley, CA, serving a catchment area of 13 zip codes. It provides inpatient and outpatient services, including 24-hour emergency care, and reports more than 50,000 emergency visits annually. Outpatient offerings include elective surgery and imaging.

- Subacute SNF Unit — A separately licensed, 98-bed subacute Skilled Nursing Unit (the "SNF Unit") that accepts referrals from distances exceeding 400 miles, including rural areas. It currently averages 60 patients, all of whom require specialized care involving tracheostomy and ventilator support.

- Behavioral Health Urgent Care Clinic — Serves individuals experiencing a mental health crisis that can be stabilized within 24 hours, as well as those who do not meet the level of medical necessity for inpatient care. It is estimated to generate $2.5 million in annual revenue.

- Medical Surgical Program — Utilized for patients requiring minor surgical procedures. Initially comprising 10 beds, it has expanded to 30 beds serving patients with psychiatric conditions recently released from incarceration who require medical release, referred directly by the California Department of Mental Health ("DMH"). The program and its contractual arrangement with DMH are a significant revenue source for the Debtor.

- Organic Farm Produce — The Debtor is taking part in a federal initiative encouraging hospitals to serve fresher, less processed food. To support the effort, it has turned three acres next to the Hospital into a working farm to grow produce for its patients, with a first corn harvest expected in September 2026.

- EmPATH Behavioral Health Urgent Care Clinic — Provides immediate psychiatric evaluation, crisis intervention, and stabilization for acute psychiatric patients for up to 24 hours, as an alternative to the emergency room. The Hospital was one of six acute care hospitals selected in California to operate an EmPATH program. The initiative is supported by a $2.9 million grant the Debtor received in December 2023 from the Mental Health Services Oversight and Accountability Commission ("MHSOAC"), awarded through a competitive procurement process in which the Debtor was among the highest-scoring applicants. The grant runs approximately three years and is distributed across three annual payments.

In addition to the programs above, the Debtor provides a range of ancillary and rehabilitative services, including an intensive care unit, laboratory services, diagnostic imaging, and pulmonary medicine. Its rehabilitation department offers physical, occupational, and speech therapy for conditions such as traumatic brain injury, post-operative orthopedic recovery, neurological disorders, and cancer-related impairments. The Debtor is also pursuing licensure for a new outpatient behavioral health line and plans to expand its outpatient and rehabilitation offerings once approved.

Employees

As of July 2026, the Debtor has approximately 697 employees, including registered nurses, technicians, housekeepers, and food-service workers, along with per-diem staff hired as needed. About 597 are represented by two unions — SEIU-121RN and SEIU-UHW — under multiple collective bargaining agreements.

Government Receivables

The Debtor relies on the Hospital Quality Assurance Fee ("HQAF") and Disproportionate Share Hospital ("DSH") programs, along with other government support, to help close the gap between what Medicare and Medi-Cal pay and the actual cost of care — those programs cover only about 80% of that cost.

HQAF, established in 2010, funds supplemental payments to California hospitals that serve Medi-Cal and uninsured patients, while DSH programs provide partial compensation to hospitals treating the most vulnerable patients. Federal DSH allotments have been scheduled for reduction since 2014 under the Affordable Care Act; Congress has repeatedly delayed those cuts, but they remain pending. Both programs have proven difficult to depend on, as payments have been reduced and delayed.

Under HQAF Program 9 (covering calendar year 2025), the Debtor received $7 million and expects approximately $16 million more in the coming months, as these payments are typically made retroactively in quarterly lump sums. The Debtor also projects $10 million from HQAF Program 10 (covering calendar year 2026), though the timing remains uncertain.

Prepetition Obligations

Funded Debt

The Debtor's funded debt consists of a $35 million loan under the Main Street Loan Program established under the CARES Act during the COVID-19 pandemic. On December 10, 2020, the Debtor entered into a Main Street Priority Loan Agreement (the "MSL") with First Western Trust Bank ("First Western") and the Federal Reserve Bank of Boston (the "Federal Reserve"), under which First Western extended a $35 million senior secured loan.

- Security & Guaranty — The $35 million facility is secured by a security interest in the Debtor's personal property under a Pledge and Security Agreement. As additional credit support, Tuft, the Debtor's sole shareholder, executed an unconditional personal guaranty and pledged 100% of his equity interests in the Debtor.

- Payment History, Default & Maturity — Between 2021 and 2024, the Debtor paid $5.1 million in interest and late fees but never applied any payment toward the principal, leaving the full $35 million outstanding as of the Petition Date. After the Debtor failed to timely meet its repayment obligations, the loan was placed in default, and it matured on December 10, 2025 with the entire balance still unpaid.

- The Colorado Action & the Contested Assignment — On May 13, 2025, First Western sued the Debtor and Paul Tuft, in his capacity as guarantor, in Colorado state court for breach of contract arising from the Debtor's failure to repay the loan, as described above (the "Colorado Action"). In November 2025, Axios Capital Solutions, LLC ("Axios") claimed to have purchased the MSL and stepped into First Western's shoes as plaintiff. The validity of that purchase is disputed: the loan agreement permitted First Western to assign its rights, but the Main Street program's terms barred any assignment to the borrower's affiliates or to a natural person, and the Federal Reserve required confirmation that there was no common ownership between buyer and borrower. The Debtor contends that Axios's ultimate owner also holds an interest in the Debtor — a question that, if resolved in the Debtor's favor, would render the assignment invalid.

- Summary Judgment Ruling — On June 26, 2026, the Colorado court denied Axios's motion for summary judgment, finding genuine issues of material fact as to whether Axios validly acquired the loan — specifically, whether common ownership between Axios and the Debtor rendered the assignment invalid — and holding that a jury must first resolve that question before the transfer's validity can be decided.

- Special Monitor & Receivership Motion — On a parallel track, the court on May 15, 2026 appointed Westwood Healthcare Partners, LLC as Special Monitor on the joint motion of Axios, the Debtor, and Mr. Tuft. Axios and the Special Monitor later moved to expand that role into a full receivership; the Debtor and Mr. Tuft opposed, and a hearing on the receivership motion was set for July 8, 2026.

- Scheduled Claim Amount — In the Debtor's list of largest creditors, Axios is scheduled as holding a disputed "Main Street Loan" claim of $44.3 million.

Other Obligations

- $9.5 million Lease Obligations — Since 2013, the Debtor has operated the Hospital, its principal facility, under a long-term Master Lease with four Landlord Entities (Reliq Pacifica LLC, Beverly Gemini Investments, LLC, Taking the 5th, LLC, and Fifth/Arizona Investors, LLC). During the COVID-19 pandemic, the Debtor fell behind on certain lease obligations, and as of the Petition Date it estimates it owes the Landlord Entities approximately $9.5 million in accrued and unpaid rent and other charges. In November 2022, the Landlord Entities filed a UCC-1 financing statement to perfect a lien on all of the Debtor's personal property; that lien is subordinated to First Western's interest (now claimed by Axios) under a Subordination Agreement. The Debtor's investigation of these security interests remains ongoing.

- $7.5 million L.A. Care Obligations — The Local Initiative Health Authority for Los Angeles County, operating as L.A. Care Health Plan ("L.A. Care"), filed UCC-1 statements in January 2026 and May 2026 asserting an interest in the future proceeds of certain HQAF funds. These interests arise from agreements under which L.A. Care purchased the Debtor's right to receive future HQAF payments; if that sale is later found not to be a true sale, the agreements grant L.A. Care a Back-Up Security Interest in the Debtor's HQAF receivables. As of the Petition Date, the Debtor estimates it owes L.A. Care approximately $7.5 million under these agreements. The Debtor has not yet determined the validity of L.A. Care's security interests.

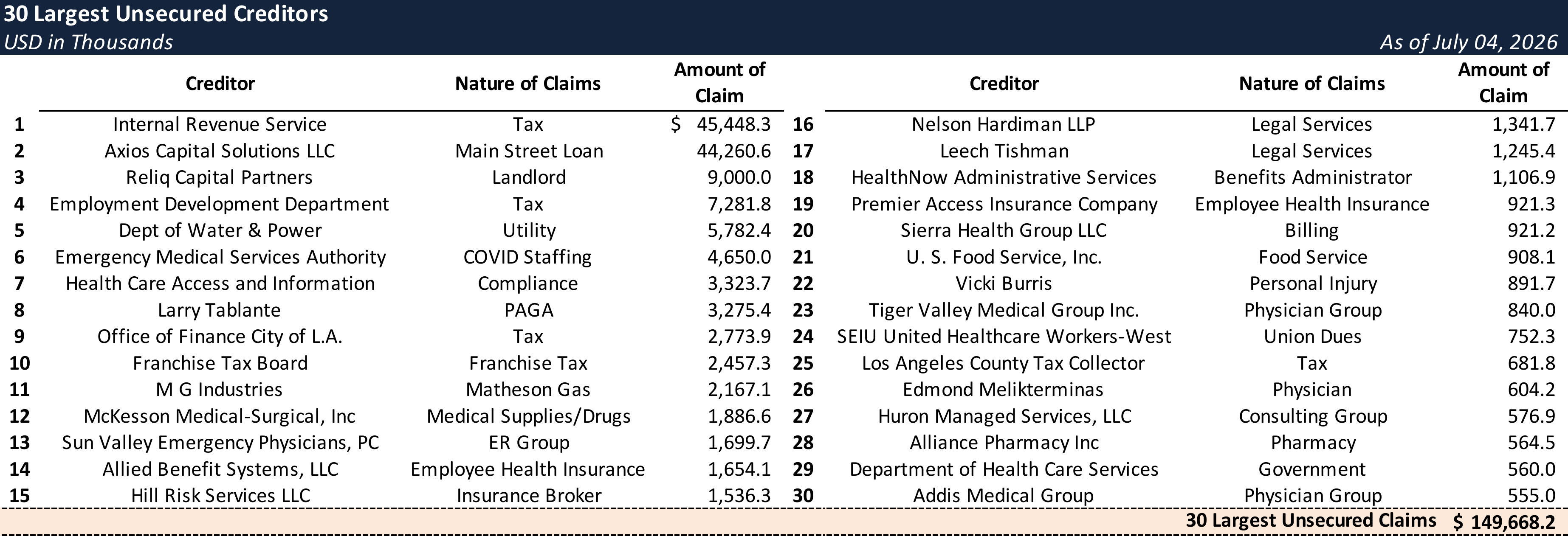

Top Unsecured Claims

Events Leading to Bankruptcy

COVID-19 Pandemic

Acting as a surge center at the State's direction, the Debtor incurred substantial debt for which it received only nominal reimbursement. After the California Department of Public Health's March 2020 directive to convert unoccupied space into critical-care beds, the Debtor added capacity in hallways, closed units, and outdoor areas — expanding its ICU from 7 to 66 beds — and, at the State's request, reopened a shuttered Los Angeles hospital as a satellite surge facility. Persistent staffing shortages forced reliance on high-cost traveling nurses, supplemented by three National Guard strike teams secured in December 2020. The Debtor never fully recovered: a lingering shortage of billing personnel interrupted its billing operations, while an approximately 60% decline in emergency-rate occupancy eroded its future Quality Assurance Fee ("QAF") funding.

Seismic Compliance and Related Costs

California law requires general acute care hospitals to complete seismic evaluations, retrofits, and repairs to meet mandated performance standards. The Debtor's role as a COVID-19 surge center disrupted this work — contractors could not access the site, causing the Debtor to miss construction and seismic milestones and incur fines. The retrofit requirement also took 38 of the Hospital's skilled nursing facility beds out of service, resulting in an estimated $20 million in lost annual revenue; those beds are scheduled to return to operation in January 2027.

After missing its deadlines, the Debtor secured an 18-month extension under Assembly Bill 2404, signed by the Governor on September 27, 2022. That relief proved insufficient: post-pandemic construction costs significantly exceeded pre-COVID estimates, and the resulting cost overruns led to litigation that further delayed the work. The extension expired on January 1, 2025, triggering fines of $15,000 per day, which totaled approximately $9 million through June 2026. The Debtor intends to pursue further legislation to extend its compliance deadline to April 20, 2028 and to abate the daily fines.

On costs, the Debtor had spent $7.8 million and $7.9 million on seismic retrofits as of December 31, 2023 and 2024, respectively. In April 2026, it obtained new retrofit quotes of approximately $6.5 million from a contractor and $650,000 from an architectural firm.

Rising Labor Costs, Working Capital Shortages, and Cyber Attack

Consistent with hospitals nationwide, the Debtor confronted mounting labor costs driven by both statewide and facility-specific factors. Compounding this, its reliance on HQAF, DSH, and other government support to cover the roughly 20% shortfall between Medicare/Medi-Cal reimbursement and the actual cost of care left it acutely exposed when those payments were reduced or delayed — a major driver of the Hospital's distress.

In February 2024, the cyber attack on Change Healthcare — a UnitedHealth Group subsidiary that processes roughly half of all U.S. medical claims — disrupted healthcare operations nationwide. This interrupted operations and cash collections, while also causing data loss for the Debtor.

Axios Litigation

As detailed above in the Prepetition Obligations section, the Debtor's senior secured Main Street loan became the subject of contested enforcement litigation after Axios claimed to have purchased it and stepped into First Western's shoes in the Colorado Action. That litigation was the immediate trigger for the filing: as Axios sought the appointment of a receiver — which would have displaced existing management — the Debtor commenced this Chapter 11 case on July 4, 2026, four days before the scheduled July 8 receivership hearing, invoking the automatic stay to halt the Colorado proceedings. The Debtor disputes the validity of Axios's acquisition of the loan, an issue that remains unresolved.

Chapter 11 Filing

Cash Collateral & Liquidity

On July 7, 2026, the Debtor filed a motion to use cash collateral, supported by the declaration of its Chief Restructuring Officer, Peter Chadwick. The Debtor does not seek DIP financing, but instead proposes to fund operations through the use of cash collateral. Three parties are identified as asserting interests in the Debtor's cash: Axios, the Landlord Entities (Reliq Pacifica LLC, Beverly Gemini Investments, LLC, Taking the 5th, LLC, and Fifth/Arizona Investors, LLC), and L.A. Care (as to certain HQAF proceeds only).

Axios has not consented to the use of cash collateral, so the Debtor seeks authority to use it on a non-consensual basis. The Debtor reserves the right to challenge the validity, perfection, extent, and priority of all three asserted interests, and separately asserts that Axios has not perfected control over the Debtor's deposit accounts and is therefore not perfected in at least a portion of the Debtor's cash.

The proposed interim order authorizes cash-collateral use through August 1, 2026 under a four-week budget, subject to a 20% aggregate, cumulative operating-disbursement variance and weekly variance reporting. Adequate protection consists of replacement liens and section 507(b) superpriority claims that apply only to the extent a party is later determined to hold valid, perfected, and enforceable prepetition liens, and only for any diminution in value; the package does not include any adequate-protection cash or interest payments to Axios or the other secured parties. The CRO must personally authorize every disbursement, and no payment may be made to any director or owner of the Debtor. The Carve-Out covers U.S. Trustee and Clerk fees, up to $25,000 for a chapter 7 trustee, budgeted professional fees, and a $250,000 post-termination cap.

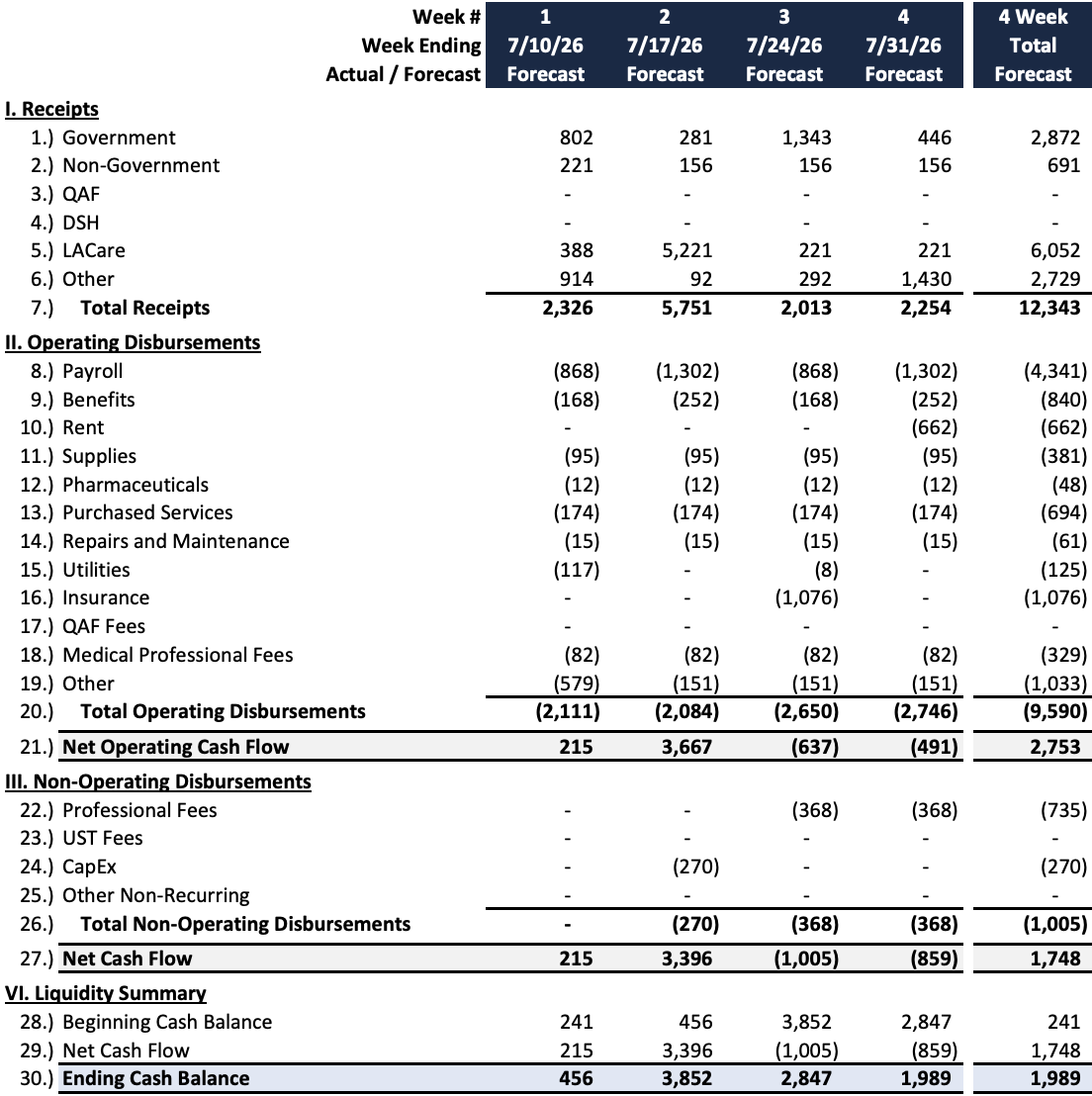

Cash Flow Forecast

The four-week budget projects total receipts of approximately $12.3 million against operating disbursements of approximately $9.6 million, with payroll of approximately $4.3 million as the largest disbursement and a projected ending cash balance of approximately $2.0 million at July 31, 2026. The largest projected receipt is approximately $6.05 million from L.A. Care, while no receipts are projected from QAF or DSH during the 4-week period.

The $35 Million Main Street Loan Dispute

- The Loan Ownership — The central issue in the case is who holds the Debtor's senior debt. Axios claims to have acquired the MSL and asserts that it is the Debtor's sole secured lender. It bought the loan at a steep discount: the Debtor states that Axios paid approximately $1.95 million for debt with a $35 million principal balance plus interest — under six cents on the dollar. The Debtor characterizes the purchase as a takeover strategy by Dr. Ehab Yacoub, a Los Angeles–area psychiatrist affiliated with the Brain Health USA network, who it contends stands on both sides of the transaction: as the ultimate owner of Axios (the buyer) and as a holder of an interest in Pacifica (the borrower). That distinction is significant because the Main Street program barred assignments to a borrower's affiliates, so the validity of Axios's claim turns on a single factual question — whether Yacoub owns or controls Pacifica. The Colorado court has reserved that question for a jury, and until it is resolved, whether Axios holds the senior claim at all remains undetermined.

- Prior Litigation — The conflict predates the loan purchase: in December 2023, Yacoub sued Tuft and the Debtor's CEO, Precious Mayes, for contractual fraud (Ehab Yacoub, M.D., et al. v. Paul Tuft, et al., No. 23SMCV06029). The Debtor cites that suit — in which Yacoub alleged he provided $5 million in funding to Tuft — together with an Institutional Affiliation Agreement between Brain Health and Pacifica, as evidence that Yacoub holds an interest in the hospital, the same common-ownership question that will determine whether Axios's purchase of the loan was valid.

- Capital Structure Implications — The outcome of the assignment dispute will significantly affect the capital structure. If the assignment is voided, Axios's disputed $44.3 million claim falls away — removing both its lien and its position over the case, though the underlying debt may revert to the original lenders rather than be extinguished. If the assignment is upheld, Axios, which the Debtor states paid roughly $1.95 million for the loan, would hold the senior secured position in the Hospital. The Debtor also disputes whether Axios is secured at all: it schedules the full $44.3 million as disputed and unsecured and asserts that Axios never perfected control over the Debtor's deposit accounts, leaving its interest in at least a portion of the Debtor's cash unperfected. The near-term issue is the Debtor's use of cash collateral, to which Axios has not consented.

Potential Issues to Consider

- Insider Relationships — The Debtor is wholly owned by Paul Tuft and, according to Becker's Hospital Review, managed by his affiliated company, Southwest Healthcare Services; the first-day declaration also notes that members of the executive team have personally lent funds to the Debtor. The interim cash-collateral order's prohibition on payments to any director or owner, together with the CRO's exclusive authority over disbursements, reflects a general sensitivity to insider-transaction risk. Whether any payments to Tuft, Southwest, or other insiders actually occurred within the relevant look-back period is not disclosed in the current record. As background only — and not as an allegation against this estate — Tuft's earlier hospital company, Doctors Community Healthcare Corporation, drew scrutiny in its own 2002 bankruptcy for employing family members, and Tuft's brother later served as an officer of another Tuft-affiliated hospital.

- The L.A. Care HQAF Monetization — The Debtor transferred its rights to future HQAF payments to L.A. Care, a public health plan, in exchange for cash upfront, and owes L.A. Care approximately $7.5 million under those agreements. The agreements are structured as a true sale but include a Back-Up Security Interest that applies only if the transfer is later found not to be a true sale, and the Debtor states that it has not yet determined the validity of L.A. Care's interests. If the arrangement is a true sale, the HQAF payments belong to L.A. Care and fall outside the estate; if it is recharacterized as a secured financing, the payments remain property of the estate, subject to L.A. Care's lien. The distinction bears directly on liquidity, as the four-week budget projects roughly $6 million of HQAF-related receipts from L.A. Care in mid-July. L.A. Care perfected its asserted interest through UCC-1 filings in January and May 2026 — the May filing falling within the 90-day period before the petition. As a result, if the transaction is treated as a financing, the timing of that perfection could expose the lien to challenge as a preference.

Path Forward

The early posture suggests a contested, litigate-the-lien reorganization rather than a lender-driven sale. The absence of milestones commits the Debtor to neither a fixed timeline nor a transaction; and while the July 2 board resolutions authorize a section 363 process, no investment banker had been retained and no sale process had launched as of the first-day filings, leaving a sale available as a fallback rather than the primary path. The Debtor's stated objective is to use the automatic stay and incoming government receivables to pursue a resolution of the Axios dispute and a value-maximizing restructuring free from further disruption.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.