Case Summary: TPx Communications Chapter 11

TPx Communications filed for Chapter 11 unable to service roughly $1.1B in debt, pursuing an RSA-backed dual-track restructuring — a Section 363 sale or a lender- and sponsor-led reorganization that would leave the managed IT services provider with about $129M of funded debt and preferred equity.

A deck version of this summary is also available HERE.

Business Description

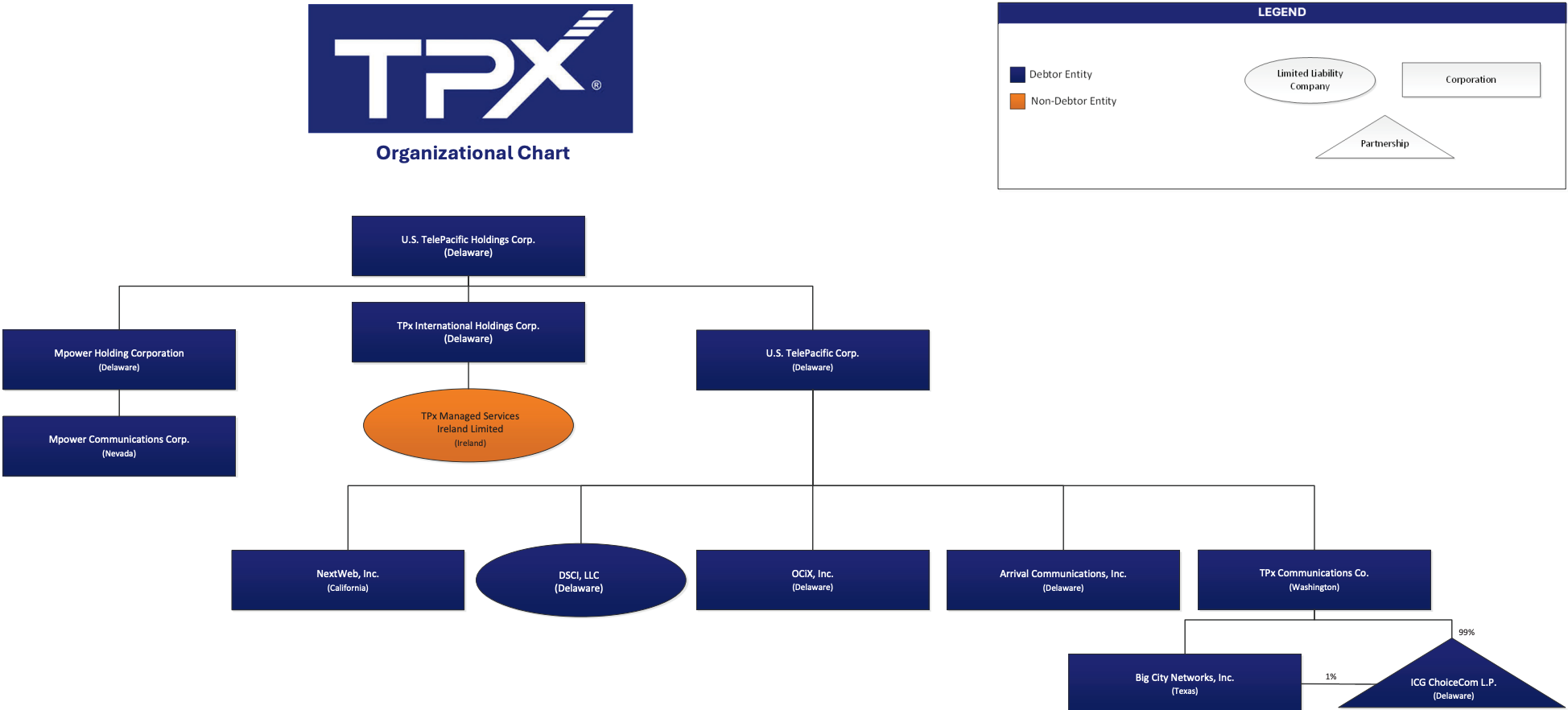

Headquartered in Austin, Texas, U.S. TelePacific Corp. (dba TPx Communications), together with its Debtor⁽¹⁾ and non-Debtor affiliates (the "Company"), operates as a national Managed IT Services Provider ("MSP"), delivering integrated connectivity and networking, cybersecurity, unified communications, and IT infrastructure services to business customers on a recurring-revenue, subscription model. The Company serves approximately 11,000 customers, primarily operating across the fifty states spanning a broad mix of industries — healthcare, financial services, legal, retail, manufacturing, education, government, and non-profit organizations.

The Company employs approximately 573 people (162 hourly, 411 salaried), supplemented by an estimated 300 to 500 independent contractors and roughly 130 third-party sales firms and agents for sales services, plus approximately 50 employees of TPx Managed Services Ireland Limited, a non-Debtor Irish affiliate that provides back-office customer and IT support.

U.S. TelePacific Corp. and certain affiliates filed for Chapter 11 protection on June 28, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Southern District of Texas, reporting $100 million to $500 million in assets and $1 billion to $10 billion in liabilities.

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

Founded in 1998 in California as TelePacific Communications, the Company began as a Competitive Local Exchange Carrier ("CLEC") serving small and mid-sized business customers. The 2006 acquisition of Mpower Communications was the Company's first major move beyond California, extending into Nevada and Chicago. In 2011, the Company completed its acquisition of NextWeb Inc. (dba Covad Wireless), adding fixed wireless network infrastructure and approximately 3,500 business customers. That same year, the Company further expanded geographically through its acquisition of Tel West Communications, which established a presence in Texas and added thousands of small and mid-sized business customers in that market. In 2016, the Company acquired DSCI, a Massachusetts-based managed services provider, expanding its customer base in the Northeast and adding unified communications and managed IT capabilities.

In 2017, following its 2016 acquisition of DSCI, the Company rebranded from TelePacific Communications to TPx Communications, reflecting its pivot from regional carrier to integrated managed-services provider.

On February 12, 2020, affiliates of Siris Capital Group, LLC — a technology- and telecom-focused private equity firm — acquired the Company from investors including affiliates of Investcorp and Clarity Partners. Siris controls the Company through Tango Private Holdings II, LLC — the sole direct equity holder, held via Tango Private Investments, LLC and ultimately owned by the Siris Partners III and IV funds.

Organizational Structure

Operations Overview

The Company’s business is built around four core service categories:

- Managed Connectivity & Networking — largest and most business-critical service portfolio. It provides the underlying infrastructure delivering business internet and networking to customer offices, supporting business applications, employee devices, and cloud applications. Services include software-defined wide area networking ("SD-WAN," a technology that uses software to manage and direct network traffic across an organization's network locations), dedicated internet access, Ethernet transport services, private networking solutions, and other enterprise-grade connectivity offerings. The Company designs, deploys, and manages networks linking multiple customer locations, supporting work-from-home employees, and delivering secure access to cloud-based systems and applications, along with ongoing monitoring, optimization, and troubleshooting to ensure uptime, performance, and reliability. These services form a critical backbone of the Company's platform and frequently serve as the foundational layer for its other managed services.

- Cybersecurity Services — Protect customer networks, systems, and data from cyber threats. These include Secure Access Service Edge ("SASE"), managed firewall and network security, endpoint protection, email and web security, threat monitoring, and incident detection and response. The Company also provides security awareness training and compliance support to help customers meet regulatory and data protection requirements. These offerings integrate with the Company's connectivity and IT management platforms, enabling continuous monitoring and real-time threat response, and represent an essential and differentiating component of its managed services portfolio.

- Unified Communications — Cloud-based unified communications services integrating voice, messaging, video, conferencing, and collaboration tools into a single platform accessible across devices and locations. These include hosted VoIP telephony, video conferencing, team collaboration applications, and cloud-based contact center functionality, enabling customers to replace on-premises phone systems with cloud-delivered platforms supporting hybrid and remote work. The Company also provides call center and contact center capabilities for multi-modal sales, support, and service via phone, SMS, and chat. These offerings represent a foundational component of the Company's portfolio and a key driver of long-term customer relationships.

- Managed Infrastructure & IT — Support customers' core technology environments, including monitoring and management of internet and network infrastructure, server and endpoint management, device lifecycle management, cloud migration and management, backup and disaster recovery, and remote help desk support, along with deployment and administration of platforms such as Microsoft 365. For many small and mid-sized customers lacking internal IT resources, the Company functions as an outsourced IT department, providing proactive monitoring, technical support, and system administration. These services are central to the Company's strategy of delivering fully integrated technology management rather than standalone communications offerings.

Regulated Telecommunications Footprint

Despite its evolution into a national managed IT services provider, TPx retains an active regulated telecommunications business, reflected in the scale of statutory fees it collects from customers and remits to government authorities. In 2025 alone, the Company collected and remitted approximately $23 million in Regulatory Passthrough Taxes and Fees — comprising Federal and State Universal Service Fund contributions, emergency 911 (E-911) fees, and Public Utility Commission regulatory charges — to the relevant federal, state, and local Taxing Authorities. As of the Petition Date, the Company estimated that an additional $5.8 million of such fees had accrued but not yet been remitted.

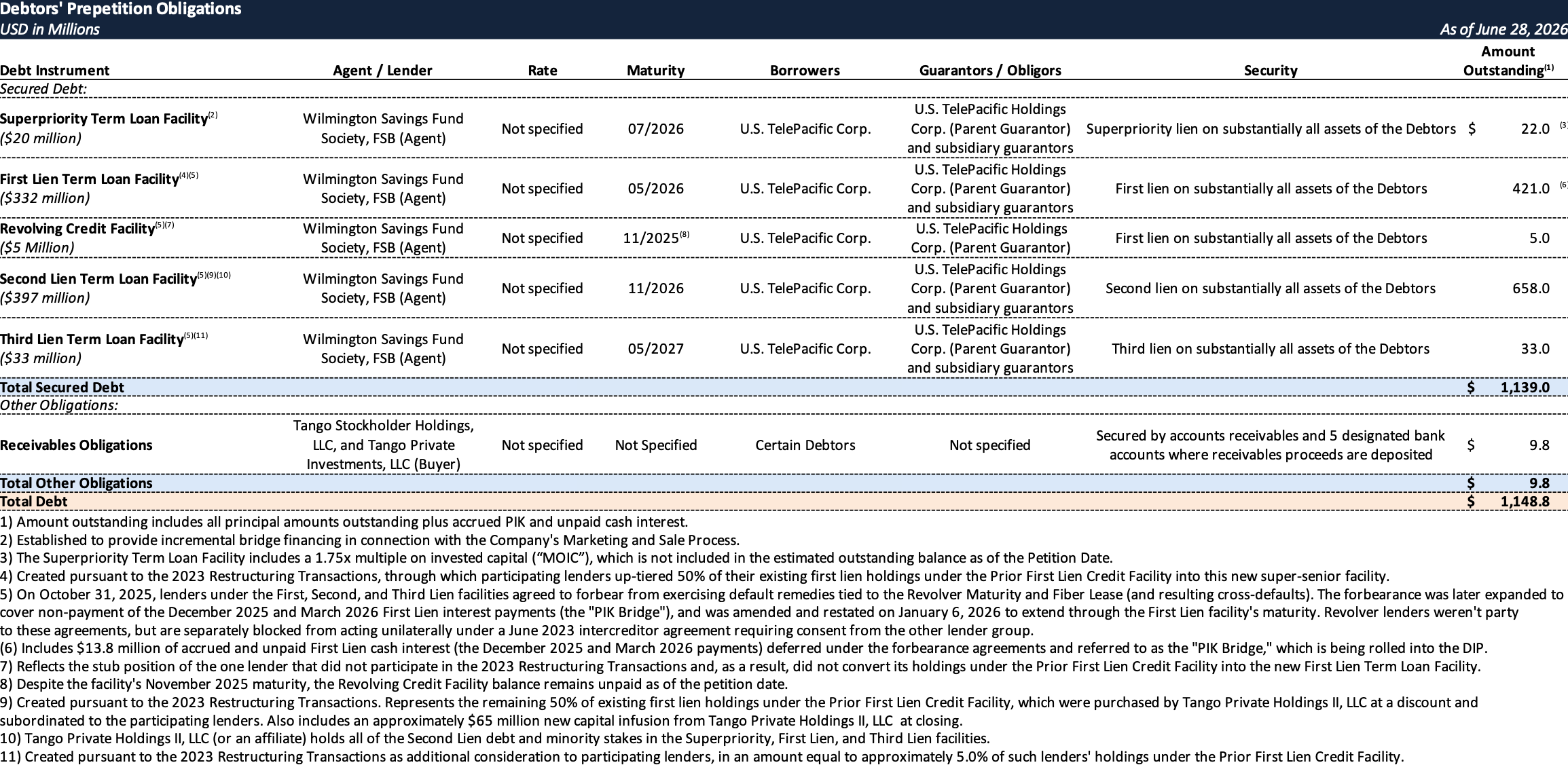

Prepetition Obligations

Top Unsecured Claims

Events Leading to Bankruptcy

The Company entered Chapter 11 carrying a restructured capital structure it could not service. Since closing its most recent out-of-court restructuring, the Company has remained a going concern and generated positive adjusted EBITDA, but its revenue growth and scale have not been sufficient to service its funded debt.

2022 Growth Equity Raise

In February 2022, the Company announced a $70 million growth equity investment led by Siris Capital Group, LLC, a private equity firm (the "2022 Transaction"). The investment was intended to support the Company's growth strategy and technology transformation. In connection with the 2022 Transaction, the Company also refinanced its senior debt obligations on more favorable terms, including a multi-year extension of maturities. Although the 2022 Transaction provided incremental capital and extended the Company’s liquidity runway, the Company’s business remained subject to significant funded debt obligations.

2023 Restructuring Transaction

In 2023, the Company and certain of its lenders, including an ad hoc group of certain of the current first lien and third lien term loan lenders (the "Ad Hoc Group"), completed a further out-of-court restructuring transaction (the "2023 Restructuring Transactions") designed to provide additional runway and operational flexibility through new capital and extended maturities (to 2026 and 2027).

Prior to the 2023 Restructuring Transactions, the Company's funded debt consisted of a single first lien credit facility (the "Prior First Lien Credit Facility"), comprising a $580 million term loan facility ("Term Loan Facility") and a $25 million revolving credit facility ("RCF").

The 2023 Restructuring Transactions split the single Prior First Lien Credit Facility into four newly created or continued instruments:

- First Lien Term Loan Facility — 50% of existing first lien holdings were up-tiered by participating lenders into this new, super-senior facility.

- Second Lien Term Loan Facility — The remaining 50% of existing first lien holdings were purchased at a discount by the Company's sole direct equity holder, Tango Private Holdings II, LLC (the "Consenting Investor"), and subordinated to the First Lien Term Loan Facility. This facility also included an approximately $65 million new capital infusion from the Consenting Investor at closing.

- Third Lien Term Loan Facility (new) — Created as additional consideration for participating lenders, on top of their First Lien Term Loan Facility allocation, in an amount equal to approximately 5% of their original holdings under the Prior First Lien Credit Facility.

- Revolving Credit Facility (continued, stub position) — One lender did not participate in the 2023 Restructuring Transactions. That lender's holdings remained outstanding, unconverted, in a stub position under what is now the Revolving Credit Facility.

Strategic Alternatives

In early 2025, the Company engaged its advisors and initiated discussions with the Ad Hoc Group and the Consenting Investor regarding potential transactions to align its capital structure with its operating profile. Management evaluated a range of alternatives, including refinancing transactions, consensual equitization or liability management transactions, incremental capital raises, and a potential sale of the business. On October 1, 2025, Bloomberg reported that the Company had told investors debt negotiations had ended after it swapped proposals with an ad hoc creditor group including Apollo Global on a confidential basis but failed to reach a deal.

In parallel, the Company assessed several significant upcoming liquidity events: the November 2025 maturity of the Revolving Credit Facility (the "Revolver Maturity"), a fourth-quarter payment obligation tied to fiber leases no longer in use (the "Fiber Lease"), and a substantial December 2025 cash interest payment under the First Lien Term Loan Facility (the "December Interest Payment"). The Company determined that satisfying all of these obligations in the ordinary course would significantly impair operating liquidity, risk covenant breaches, and impact its evaluation of strategic alternatives.

Contemporaneously, the Company concluded that a court-supervised marketing and sale process would offer the best opportunity to canvas the market and maximize the value of its assets. The Company formally launched its Marketing and Sale Process in early December 2025.

Forbearance Agreements

To preserve liquidity and provide a stable backdrop for the Marketing and Sale Process, the Company entered into a series of forbearance agreements with the Ad Hoc Group and the Consenting Investor, who together hold supermajorities under the First Lien, Second Lien, and Third Lien Term Loan Facilities.

On October 31, 2025, lenders under the First, Second, and Third lien agreements agreed to forbear from exercising default-related remedies tied primarily to the looming Revolver Maturity and a Fiber Lease obligation, along with the cross-defaults either would trigger elsewhere in the capital structure (the "Initial Forbearance Agreements"). Revolving Credit Facility lenders were not party to this agreement but were separately restrained from acting unilaterally under a June 2023 intercreditor agreement, absent consent of the lender group under the First, Second, and Third Lien debt facilities.

The agreement was later expanded to cover the Company's anticipated inability to make its December 2025 cash interest payment on the First Lien Term Loan Facility. Rather than triggering a default, lenders allowed the payment to go unpaid and accrue instead, with the resulting deferred amount referred to as the "PIK Bridge."

On January 6, 2026, forbearance was extended through the First Lien Term Loan Facility's maturity and broadened to cover the March 2026 interest payment, which together with the December shortfall comprises the "Rolled PIK Bridge." That same day, the Company, the Consenting Investor, and the Ad Hoc Group entered into a Restructuring Support Agreement establishing a framework for a comprehensive restructuring.

Independent Governance

On September 30, 2025, TPx Holdings appointed James Gillis and Anthony Horton as independent directors (the "Initial Independent Directors") to its board. On October 27, 2025, the board established a Special Committee, comprised of the Initial Independent Directors, to investigate potential claims against related parties (the "Independent Investigation") and evaluate strategic alternatives. As of February 19, 2026, the Special Committee directed the engagement of Katten Muchin Rosenman LLP as independent counsel to assist with the Independent Investigation.

On January 6, 2026, TPx Holdings appointed David Aloise and Lloyd Sprung as additional independent directors (the "Subsequent Independent Directors") and established a Transaction Committee, comprised of all four independent directors, to oversee the Marketing and Sale Process. On April 24, 2026, the Subsequent Independent Directors were also added to the Special Committee. The Independent Investigation has been ongoing since February 2026 and remained ongoing as of the Petition Date.

Prepetition Marketing Process

On December 4, 2025, the Company, with the assistance of PJT Partners, launched the Marketing and Sale Process. PJT contacted 65 potential buyers, comprising both strategic partners and financial sponsors, of which 33 signed non-disclosure agreements and received data room access. Management and PJT engaged in 26 diligence sessions and other transaction-related conversations, including 9 management presentations with potential buyers.

Ultimately, the Company received 9 bids, none of which reflected terms sufficiently developed to proceed on an actionable basis. The Company determined that continuing the process in a court-supervised environment would maximize value and provide additional time and flexibility to solicit better bids. Accordingly, the Ad Hoc Group and the Consenting Investor provided the $20 million Superpriority Term Loan Facility to fund the continuation of the process and other operational expenses.

The Chapter 11 Filing

Restructuring Support Agreement and Dual-Track

The cases are anchored by a Restructuring Support Agreement (the "RSA"), first executed on January 6, 2026, amended and restated on March 18, 2026, and further amended on June 28, 2026. The RSA commands near-unanimous creditor support, backed by the Consenting Investor (Siris), 100% of superpriority lenders, approximately 98% of first lien lenders, 100% of second lien lenders, approximately 88% of third lien lenders, and 100% of accounts-receivable purchasers (collectively, the "Consenting Stakeholders"). It establishes a dual-track structure: a value-maximizing Section 363 sale if the marketing process produces an actionable bid meeting the Minimum Bid Requirements, or, failing that, a Reorganization Transaction recapitalizing the Company with its existing lenders and the Consenting Investor through a Chapter 11 Plan.

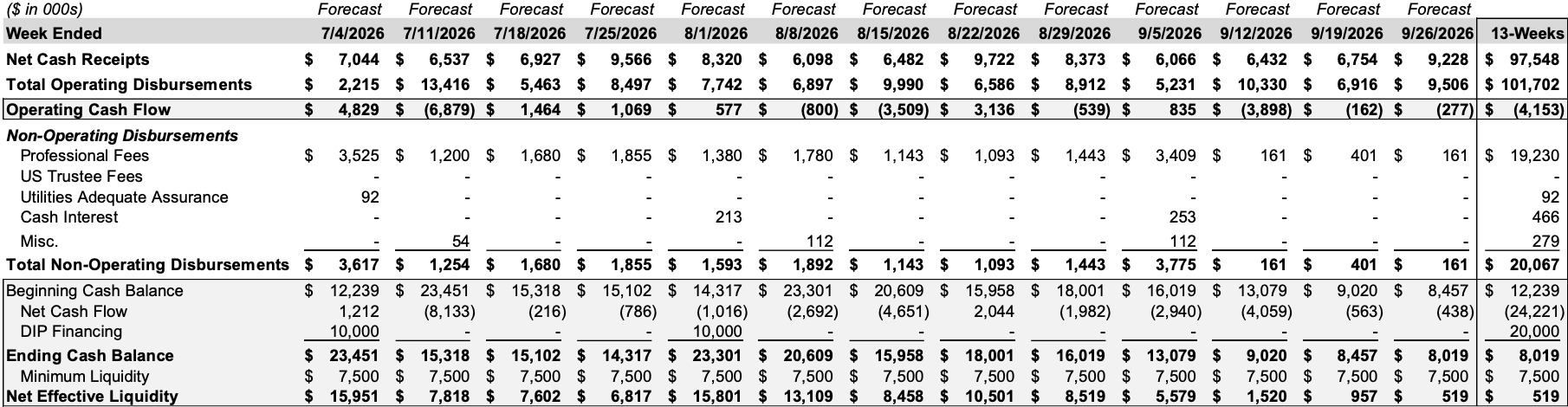

DIP Financing

The Debtors entered Chapter 11 with approximately $16.4 million of unrestricted cash against roughly $35 million of average monthly receipts. Participating first lien lenders, including the Consenting Investor, committed a $73.55 million priming, superpriority DIP, with WSFS serving as administrative and collateral agent. Of that total, $20 million is new money, funded in two $10 million tranches upon entry of the Interim and Final Orders. The remaining $53.5 million represents a roll-up of prepetition debt: $34.7 million of Superpriority Term Loan Facility obligations, inclusive of the 1.75x MOIC negotiated in that facility (the "Rolled Bridge Facility"); $13.8 million of unpaid First Lien interest from the deferred December 2025 and March 2026 payments (the "Rolled PIK Bridge"); and $5 million of additional First Lien Term Loan Facility principal (the "Pari Rolled Debt"). Pricing on the DIP is as follows:

- Premiums / MOICs: The $20 million New Money tranche carries a 2.00% commitment premium, paid in kind, plus a 1.25x MOIC payable upon repayment in full of the New Money tranche. Separately, the $34.7 million Rolled Bridge tranche carries a 1.75x MOIC, carried over from the Prepetition Superpriority Credit Agreement.

- Maturity: The DIP Facility matures December 31, 2026, with the Borrower able to extend the maturity date up to three times, in three-month increments, subject to the consent of the Ad Hoc Group.

The 1.75x bridge MOIC crystallizes an approximately $13 million premium for the bridge lenders (the Ad Hoc Group and the Consenting Investor), converting their roughly $20 million March 2026 bridge facility into priming DIP debt that itself can accrue PIK interest of up to 10%. The DIP liens prime all prepetition liens, subject only to a professional-fee carve-out of $1 million for Debtor professionals and $50,000 for Creditors' Committee professionals. Any challenge to the stipulated prepetition obligations of roughly $1.1 billion faces a tight 60-day window and a $25,000 investigation budget.

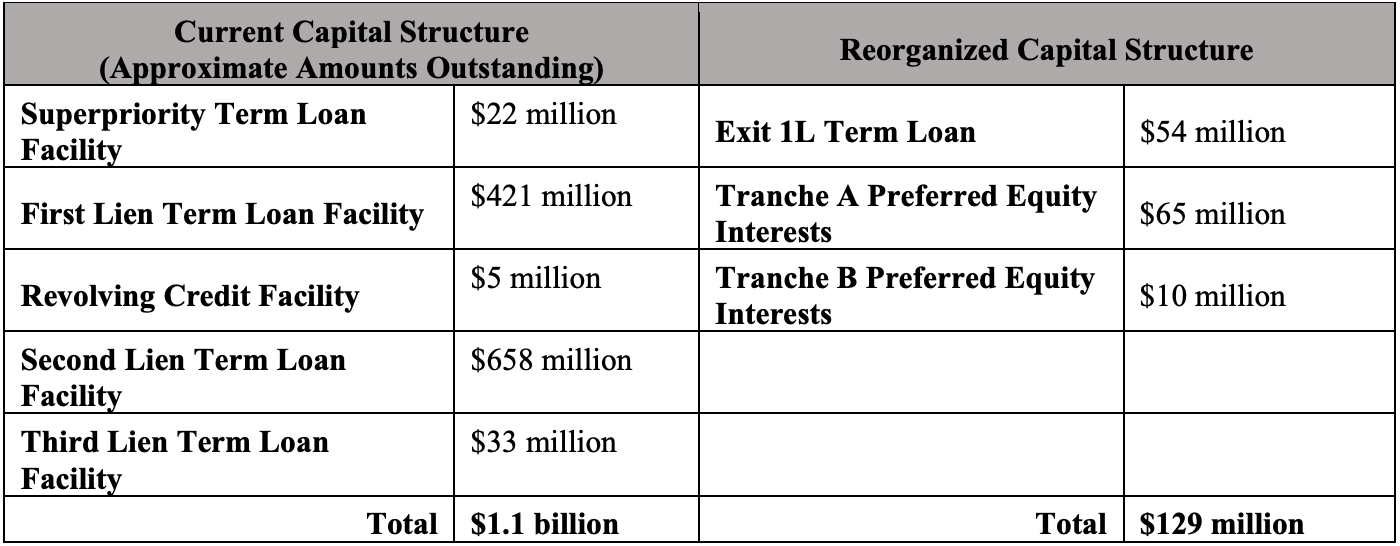

Illustrative Reorganized Capital Structure

A Reorganization de-levers the Company from approximately $1.1 billion of funded debt to approximately $129 million of total reorganized capitalization, comprising a ~$54 million Exit 1L Term Loan, ~$65 million of Tranche A Preferred Equity, and ~$10 million of Tranche B Preferred Equity. Class 3 (First Lien/Revolver lenders) receives the new common equity; Class 4 (Second Lien lenders) receives 5.94% warrants.

- The 1L Exit Facility is estimated at approximately $54.1 million in aggregate principal as of the Petition Date, comprising the converted New Money Term Loan Advances, the Pari Rolled Debt, and — to the extent the relevant lenders elect exit debt rather than cash — the Rolled Bridge Facility. This figure is explicitly flagged in the Plan as subject to change based on the actual DIP Facility balances outstanding at emergence, since the final conversion mix depends on which Rolled Bridge Facility lenders elect cash versus 1L Exit Facility debt.

- Tranche A Preferred Equity is funded by certain of the Consenting Stakeholders — a group that includes the Consenting Creditors (Superpriority, First Lien, Second Lien, and Third Lien lenders who signed the Restructuring Support Agreement) and the Sponsor, Siris Capital Group, LLC and its affiliates — through $51.6 million of new cash, a $3.7 million in-kind commitment premium paid to those same funding parties, and $9.3 million of Rolled PIK Bridge debt (previously unpaid First Lien interest) converting into equity rather than into the Exit 1L Term Loan.

- Tranche B Preferred Equity is funded by the RPA Purchasers' contribution of $9.8 million of accounts-receivable obligations back to the Company.

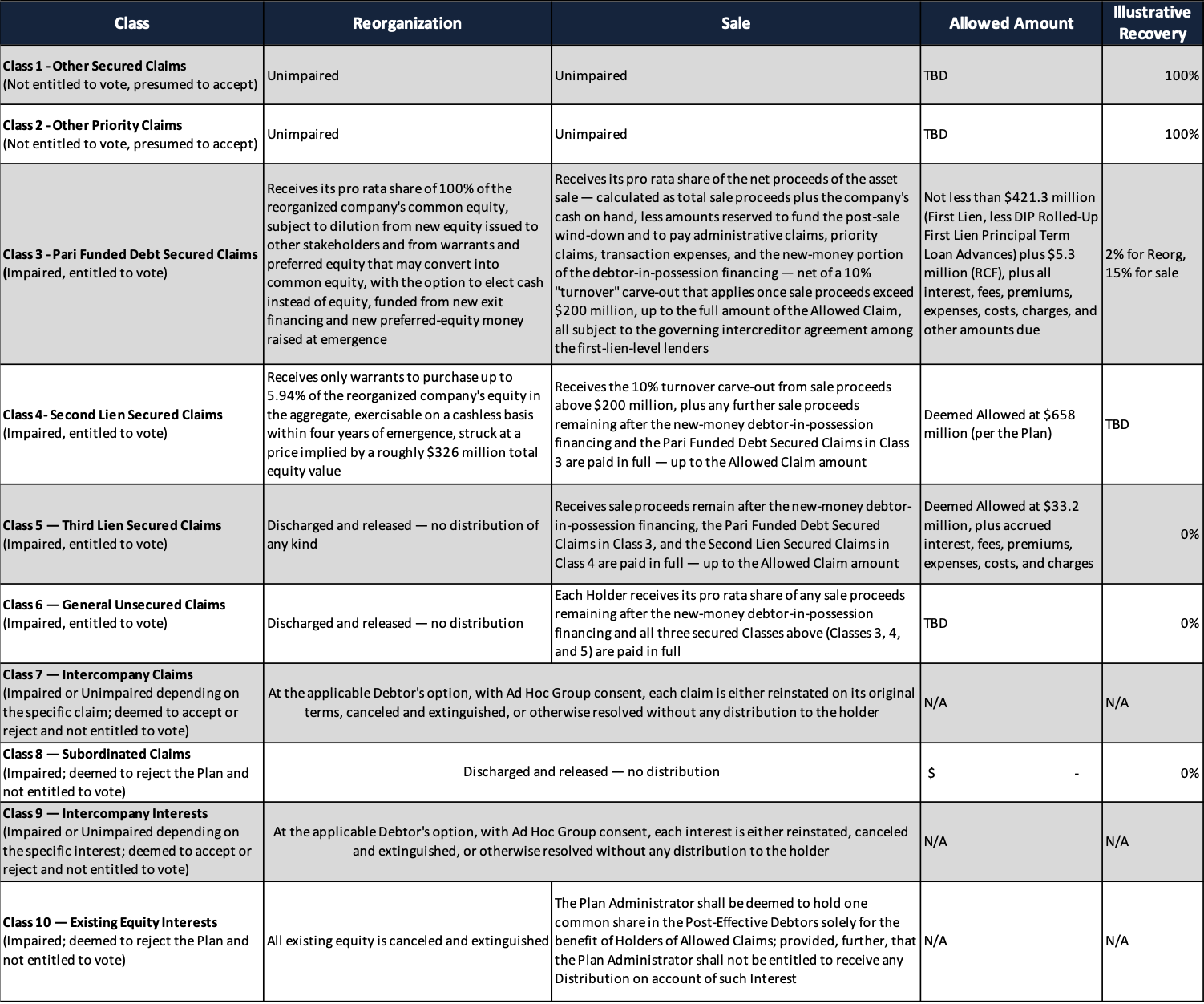

Treatment of Claims

Under a Sale Transaction, all DIP Claims are paid in full in Cash on the Effective Date, sitting ahead of essentially every other Class in the distribution waterfall — they must be satisfied before any sale proceeds reach the Pari Funded Debt Secured Claims in Class 3.

Under a Reorganization Transaction, treatment varies by component:

- Holders of the $20 million New Money Term Loan Advances and the $5 million Pari Rolled Debt — Receive new first-lien exit term loans on a dollar-for-dollar basis.

- Holders of the $34.7 million Rolled Bridge Facility — Paid in full in Cash, or if they also fund their pro rata share of the new exit financing as a Funding Consenting Lender — receive new first-lien exit term loans on a dollar-for-dollar basis instead.

- Holders of the $13.8 million Rolled PIK Bridge — Paid in full in Cash, or if they qualify as a Funding Consenting Lender — receive Tranche A Preferred Equity Interests in the reorganized company instead, including a separate exchange premium paid in additional preferred equity.

A summary table for treatment of claims is below.

Bid Procedures

The Debtors' prepetition marketing process did not yield a stalking horse bid. The Debtors received final approval of the bidding procedures motion, seeking the authority to designate one going forward — exercised in their discretion and in consultation with the Consultation Parties, with no obligation to do so. The Consultation Parties comprise the Ad Hoc Group (the Consenting Superpriority, First Lien, and Third Lien Lenders) and any statutory committee appointed in the case; the Prepetition Second Lien Lenders are expressly excluded from Consultation Party status in any capacity.

Minimum purchase price is set at $175 million, with cash and non-cash components identified separately. Bid deadline is set on August 7 with an auction set on August 12, which will be held only if the Debtors receive at least two Qualified Bids; absent that, the bid procedures instead serve as a market test informing the Reorganization Transaction.

The stalking horse break-up fee is capped at 3% of the purchase price (including assumed liabilities), with any expense reimbursement subject to a separate reasonable cap, and is payable only if a stalking horse bidder is in fact designated. The DIP Lenders and Prepetition First Lien Lenders may credit bid without first paying senior claims in full; all other secured parties may credit bid only if claims senior to their liens are paid in full in cash at closing.

Confirmation Timeline & Key Milestones

The Debtors are pursuing an expedited, RSA-driven timeline of roughly 80 days, with the Sale Hearing procedurally welded to confirmation:

- June 28, 2026 — Petition Date

- June 29, 2026 — First-day hearing; entry of the Interim DIP Order.

- Aug. 7, 2026 — Bid Deadline.

- Aug. 12, 2026 — Auction, only if at least two Qualified Bids are received.

- Aug. 17, 2026 — Plan Supplement (liquidation analysis, financial projections, Schedule of Retained Causes of Action).

- Aug. 26, 2026 — Voting, plan/disclosure objection, and third-party release opt-out deadlines.

- Sept. 2, 2026 — Combined confirmation and Sale Hearing.

- Effective Date — targeted ~80 days from filing, subject to the required FCC and state regulatory approvals, which may extend closing beyond confirmation.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.