Case Summary: Sangamo Therapeutics Chapter 11

Sangamo Therapeutics filed for Chapter 11 after losing its major collaboration revenues and exhausting its liquidity, pursuing a court-supervised sale with stalking-horse bids from Lilly for its core platforms and Astellas for its Fabry program.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Richmond, California, Sangamo Therapeutics, Inc. ("Sangamo," the "Company," or the "Debtor") is a genomic medicine company that translates science into therapies for serious neurological diseases. Genomic medicine refers to therapies that treat disease by directly targeting the genes that cause or drive it, rather than addressing symptoms alone.

In 2023, Sangamo recast itself as a neurology-focused enterprise built on two complementary capabilities:

- Epigenetic regulation therapies, which are precision medicines designed to treat serious neurological diseases; and

- Novel engineered adeno-associated virus (“AAV”) capsids, which are delivery vehicles designed to carry those therapies to the intended neurological targets.

The business rests on three proprietary platforms — the zinc finger protein ("ZFP") platform, the SIFTER AAV capsid engineering platform, and the Modular Integrase ("MINT") genome editing platform — applied across a pipeline of wholly owned and partnered programs targeting diseases with few or no adequate treatments.

Sangamo Therapeutics, Inc. filed for Chapter 11 protection on June 23, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the District of Delaware, reporting $100 million to $500 million in both assets and liabilities.

Corporate History

Sangamo was founded in 1995 as Sangamo BioSciences, Inc. by Edward Lanphier to commercialize zinc finger protein technology, securing an exclusive license to the foundational zinc-finger-nuclease research of Srinivasan Chandrasegaran of Johns Hopkins — who had pioneered the fusion of engineered zinc fingers to the FokI nuclease — supplemented by early licenses from Johns Hopkins, MIT, and The Scripps Research Institute. The Company was incorporated in Delaware in June 1995, and completed its Nasdaq initial public offering in April 2000. In 2017, the Company rebranded from Sangamo BioSciences to Sangamo Therapeutics.

Organizational Structure

Sangamo Therapeutics, Inc. is the sole Debtor in these proceedings. It maintains three wholly owned, non-debtor subsidiaries:

- Sangamo Therapeutics France S.A.S. (formerly TxCell S.A.— majority stake acquired by Sangamo in October 2018);

- Sangamo Therapeutics UK Ltd. (formerly Gendaq Limited, acquired by Sangamo in July 2001); and

- Ceregene, Inc. (Delaware, dormant, acquired by Sangamo in October 2013).

The Debtor funds its two foreign non-debtor subsidiaries — Sangamo France and Sangamo UK — in the ordinary course at roughly $100,000 to $300,000 per month each, subject to an interim cash-management order capping aggregate intercompany transfers at $425,000 and prohibiting intercompany loans absent further order of the Court. Sangamo France is maintained principally to collect approximately €12.5 million in French R&D tax credits, including an approximately €4.7 million tranche expected in October 2026, and to fulfill long-term patient-monitoring obligations, certain of which extend through 2039.

Operations Overview

Sangamo's value rests on three proprietary technology platforms and the clinical- and preclinical-stage pipeline they support. The two stalking-horse sales divide this estate along clear program lines: Lilly takes the platforms, the prion program, the IP, and the outlicensing royalty/milestone streams; Astellas takes the Fabry program. Four programs are excluded and slated for separate marketing.

Technology Platforms

- Zinc Finger Protein ("ZFP") - Naturally occurring human proteins that Sangamo engineers into precision tools that selectively silence or activate a targeted gene.

- SIFTER (AAV capsid engineering) - Sangamo's proprietary AAV capsid engineering platform, designed to identify delivery vehicles with improved ability to reach the brain and central nervous system. The platform screens tens of millions of unique capsid variants through successive rounds of testing to identify those with superior delivery to the brain and spinal cord. This process yielded STAC-BBB, a proprietary capsid that has demonstrated the ability to cross the blood-brain barrier in nonhuman primates and mice after intravenous administration, as well as STAC-102 and STAC-103, designed for alternative central nervous system delivery routes with improved performance compared to existing benchmark capsids.

- MINT - A genome editing platform designed to integrate large DNA sequences into the genome without creating double-stranded DNA breaks, potentially allowing a single medicine to treat patients with different mutations in the same disease-causing gene, and compatible with multiple delivery methods.

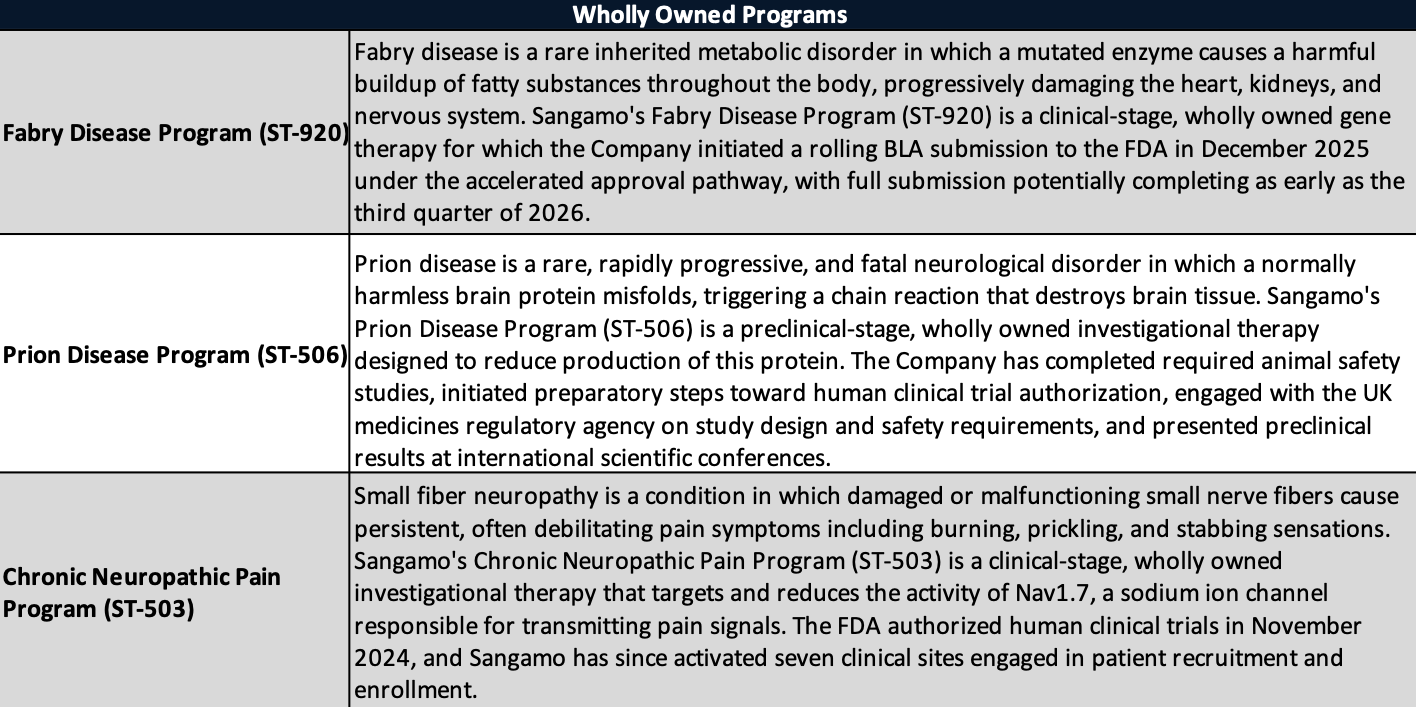

Wholly Owned Programs

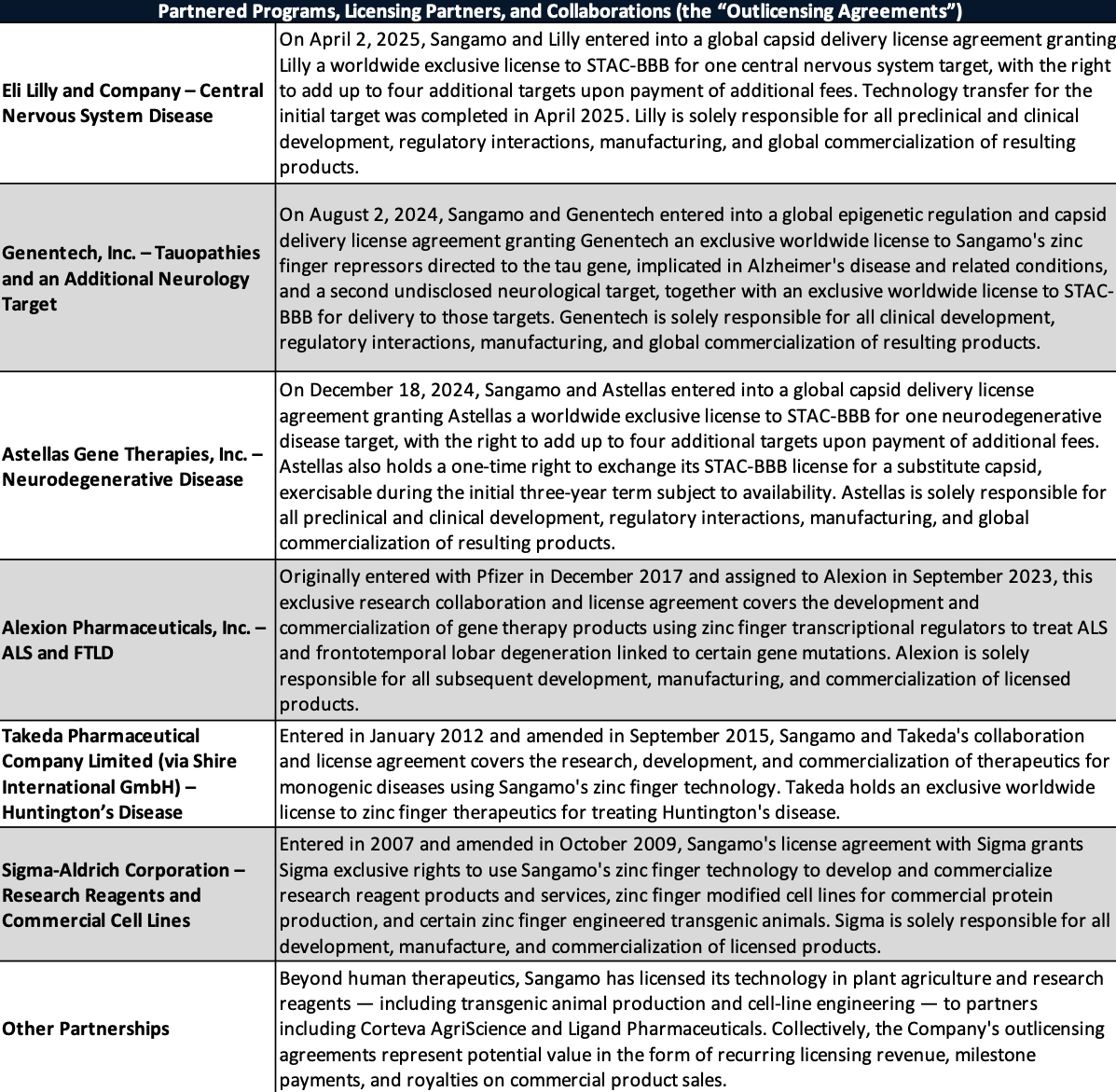

Partnered Programs, Licensing Partners, and Collaborations (the “Outlicensing Agreements”)

Other Programs

- Hemophilia A Program (SB-525) — A clinical-stage, liver-directed AAV gene therapy for severe Hemophilia A, an inherited bleeding disorder in which insufficient blood-clotting protein causes prolonged bleeding following injury and, in severe cases, spontaneous internal bleeding. Previously developed in partnership with Pfizer under a 2017 collaboration agreement, Pfizer terminated the arrangement for convenience effective April 2025. Upon termination, Sangamo received an exclusive worldwide royalty-bearing sublicensable license from Pfizer to continue development and commercialization, and has since been seeking a new commercialization partner.

- Sickle Cell Disease Program (BIVV003) — A clinical-stage investigational gene therapy candidate designed to treat sickle cell disease, a serious, inherited blood disorder in which abnormal hemoglobin causes red blood cells to become rigid and sickle-shaped, leading to episodes of pain, organ damage, and other severe complications.

- Tregs Platform — Consists of a clinical-stage program and two early-stage development programs focused on the development of regulatory T cell (Treg)-based therapeutics for the treatment of autoimmune and inflammatory conditions.

Intellectual Property

Sangamo protects its proprietary rights through a combination of patents, copyrights, trademarks, trade secrets, proprietary know-how, and confidentiality, materials transfer, research, and licensing agreements. Its portfolio comprises approximately 90 patent families directed to the design, composition, and use of zinc finger proteins and other technologies underlying its programs.

The Company is also licensor under numerous out-license agreements to third-party collaborators. These include exclusive worldwide licenses to STAC-BBB granted to Genentech, Astellas, and Lilly, each for defined fields of use, exclusive worldwide licenses to zinc finger repressors directed to specific neurological targets granted to Genentech, and an exclusive worldwide license to zinc finger therapeutics for Huntington's disease granted to Takeda.

Manufacturing

Sangamo relies primarily on contract manufacturing organizations ("CMOs") to produce preclinical and clinical supply for its pipeline, and intends to continue using third parties for later-stage clinical trials and commercial-scale manufacturing. The Company maintains a technical operations staff across process development, analytical development, quality control, quality assurance, supply chain, project management, and external manufacturing to oversee its CMOs, support regulatory filings, and supply clinical trials. This reliance on external manufacturers follows the closure of the Valbonne, France facility and the anticipated closure of the Brisbane Facility as part of the Company's restructuring initiatives.

Real Property Leases

As of the Petition Date, the Debtor is party to three California real property leases:

- Corporate headquarters at 501 Canal Blvd., Suite A100, Richmond, California, comprising approximately 59,485 square feet of research and office space.

- A separate office lease at 1003 West Cutting Boulevard, Richmond, California, comprising approximately 7,700 square feet.

- A research and development laboratory and office facility at 7000 Marina Boulevard, Brisbane, California, comprising approximately 103,089 square feet.

The Brisbane facility has been in very limited use since early 2024, when the Company commenced efforts to close it and began marketing it extensively for sublease. Under a lease amendment entered August 25, 2025, the landlord was authorized to draw on an existing $1.5 million letter of credit to offset rent between September and November 2025, with the Company obligated to reinstate the letter of credit to its full $1.5 million face amount by December 31, 2026. The amendment also deferred 90% of monthly base rent between December 2025 and December 2026 on an interest-free basis, with the full deferred amount payable by January 5, 2027.

Employees and Workforce Reductions

Sangamo has undergone a series of significant workforce reductions in recent years. The April 2023, November 2023, and France restructurings collectively eliminated approximately 365 roles. In March 2026, the Company executed a further reduction in force eliminating approximately 22 roles and furloughing 14 employees as part of its ongoing efforts to reduce operating expenses and preserve liquidity.

In connection with its Chapter 11 filing and proposed sale transactions, the Company executed an additional reduction in force in June 2026, reducing its workforce from 128 full-time employees to 77. Certain employees affected by the June reduction agreed to transition from full-time employment to part-time independent contractor arrangements to continue providing services on a limited basis during the pendency of the proceedings.

Following the June reduction, the remaining workforce consists solely of employees specifically identified and selected by Lilly and Astellas in connection with their respective sale transactions, together with those employees and independent contractors identified as necessary to assist with administration of the Chapter 11 case.

Prepetition Obligations

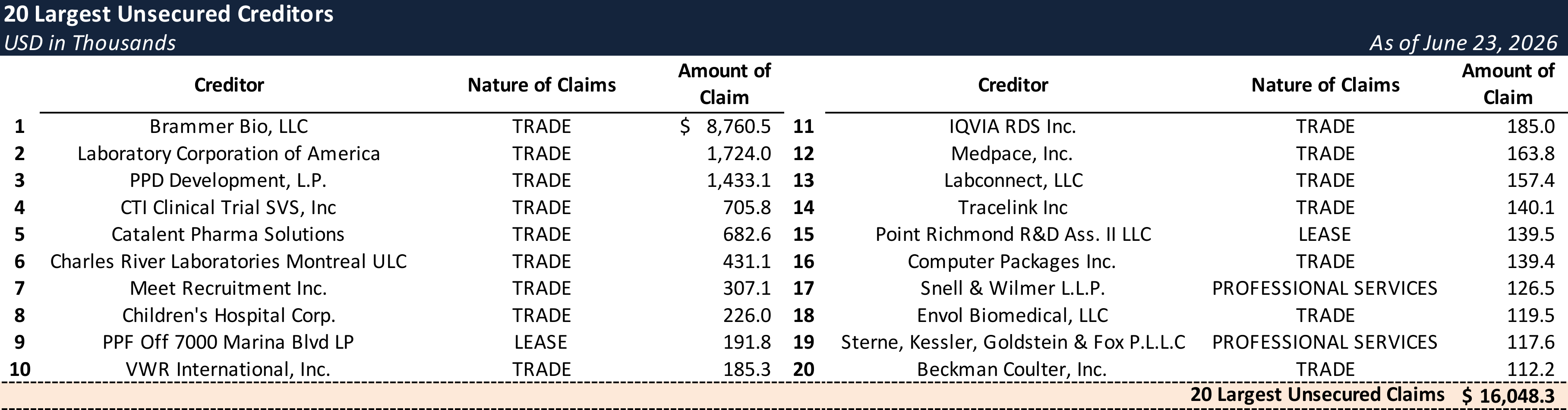

As of the Petition Date, the Debtor has no funded debt obligations, including no prepetition secured debt, unsecured notes, or credit facility obligations. The Debtor’s outstanding general unsecured prepetition obligations as of the Petition Date primarily consist of trade payables, lease obligations, and employee obligations totaling $39.5 million.

The General Unsecured Claims Pool (~$39.5 Million)

- Trade payables — Approximately $19.2 million, owed largely to CMOs and R&D service providers. The single largest creditor is Brammer Bio, LLC (a Thermo Fisher contract manufacturer) at approximately $8.76 million — by itself nearly half the trade pool — followed by Laboratory Corporation of America (~$1.72M), PPD Development (~$1.43M), CTI Clinical Trial Services (~$0.71M), Catalent Pharma Solutions (~$0.68M), and Charles River Laboratories (~$0.43M).

- Lease obligations — Approximately $4.0 million, including deferred rent accrued under the Brisbane Lease Amendment.

- Employee obligations — Approximately $16.3 million: roughly $9.4 million in unpaid annual performance bonuses for fiscal years 2024 and 2025; approximately $3.7 million in severance obligations to employees terminated in connection with the March and June reductions in force; approximately $2.3 million in accrued but unfunded merit-based salary increases for fiscal year 2025; and approximately $900,000 in accrued but unpaid COBRA benefits following employee terminations.

As of the Petition Date, the Debtor has approximately $5.5 million in cash on hand.

Top Unsecured Claims

Events Leading to Bankruptcy

Sangamo's path to Chapter 11 is a study in mistimed transformation. In 2023, Sangamo repositioned itself as a neurology-focused genomic medicine company centered on epigenetic regulation therapies and engineered AAV capsid delivery technology. The transformation coincided with the loss of each of the Company's principal collaboration revenue streams — from Biogen, Novartis, Kite, and Pfizer — alongside a broader post-COVID biotech investment contraction that reduced publicly available capital. The resulting financial pressure was compounded by the Company's inability to secure a commercialization partner for the Fabry Disease Program outside of a court-supervised process, causing liquidity to deteriorate with each successive quarter.

The 2023 Restructurings

In April 2023, Sangamo executed its first restructuring, eliminating approximately 110 roles — split evenly between full-time and contracted employees — representing approximately 23% of the U.S. workforce. The reduction was intended to concentrate resources on the preclinical neurology epigenetic regulation portfolio, preparations for a potential Phase 3 Fabry trial, and an ongoing renal transplant rejection study, and was expected to generate annualized savings of approximately $31 million together with other cost reduction initiatives.

The cuts proved insufficient. On October 11, 2023, the Board approved a second restructuring, eliminating a further 162 U.S. roles — 108 full-time and 54 contracted employees — representing approximately 40% of the U.S. workforce at the time. In connection with this second restructuring, the Company commenced the process of closing its Brisbane Facility, which had served as its primary internal manufacturing facility, and transitioned its headquarters to Richmond, California effective January 1, 2024. The Company subsequently entered into a lease amendment for the Brisbane Facility in August 2025.

Wind Down of French Operations

Beginning in mid-2023, the Company sought additional investors and collaboration partners for its cell therapy programs in Valbonne, France. Despite extensive outreach efforts, the Company was unable to identify a transaction on acceptable terms.

On March 1, 2024, the Board approved the wind-down of all French research and development activities and the closure of the Valbonne cell therapy manufacturing facility and research laboratories, eliminating all 93 roles in France and representing a reduction of approximately 24% of the Company's total global workforce.

Termination of Major Collaboration Agreements

As the Company pursued its strategic transformation, it simultaneously lost each of its major collaboration agreements that had historically driven its revenues.

- In February 2020, Biogen Inc. entered into a global licensing collaboration with Sangamo covering gene regulation therapies for tauopathies including Alzheimer's disease, synucleinopathies including Parkinson's disease, a neuromuscular target, and up to nine additional neurological targets, under which Sangamo received $350 million upfront — comprising a $125 million license fee and $225 million in equity investment — and became eligible to earn up to $2.37 billion in development and commercial milestones plus tiered royalties.

- In July 2020, Novartis Institutes for BioMedical Research, Inc. entered into a separate global licensing collaboration covering three neurodevelopmental targets, including genes linked to autism spectrum disorder, under which Sangamo received a $75 million upfront license fee and became eligible to earn up to $720 million in milestones plus tiered royalties.

In June 2023, both Biogen and Novartis terminated their respective collaboration agreements for convenience following internal strategic reviews, extinguishing the Company's entitlement to milestone payments and royalties and ending each counterparty's development and reimbursement obligations. The collaboration agreement with Kite Pharma, Inc. expired by its terms in April 2024 and was not renewed.

The combined financial impact was severe. Revenues fell from $176.2 million in 2023 to $57.8 million in 2024, a decline of $118.4 million driven primarily by the elimination of collaboration revenues previously generated under the Biogen, Novartis, and Kite agreements.

The pressure intensified in December 2024, when Pfizer Inc. notified Sangamo of its termination for convenience of their collaboration agreement, following Pfizer's decision not to seek regulatory approval or commercialization of the Hemophilia A gene therapy that was ready for submission to regulatory authorities. The termination extinguished all licenses and rights previously granted to Pfizer and eliminated the Company's entitlement to future royalties and milestones — including $220 million in milestone payments the Company had anticipated would fund its neurology pipeline. The announcement triggered an approximately 50% decline in the Company's stock price in the days immediately following, effectively foreclosing equity financing as a meaningful source of capital.

Equity Raises and Licensing Transactions

To extend its cash runway, Sangamo pursued a dual-track strategy of dilutive equity raises and non-dilutive technology licensing. On the equity side, the Company raised approximately $15.1 million under its at-the-market program in 2023, approximately $21.9 million in a March 2024 registered direct offering, and an aggregate of approximately $100.1 million across at-the-market sales and two underwritten public offerings between 2025 and early 2026.

In parallel, the Company monetized its capsid platform through a series of STAC-BBB license agreements — with Genentech in August 2024 for $40.0 million upfront plus a $10.0 million technology-transfer milestone, with Astellas in December 2024 for $20.0 million upfront, and with Lilly in April 2025 for $18.0 million upfront — generating approximately $88 million in near-term proceeds against billions in back-loaded development and commercial milestones.

Notwithstanding the cumulative scale of these efforts, none of the transactions provided upfront proceeds sufficient to resolve the Company's long-term liquidity challenges. Each successive raise and licensing transaction provided temporary relief while the underlying deterioration continued.

The Fabry Commercialization-Partner Search

Beginning in 2022, Sangamo undertook a multi-year effort to secure a commercialization partner for its Fabry Disease Program, pursuing a dual-track strategy of advancing its patient study to generate clinical data while simultaneously seeking regulatory clarity in the United States and Europe.

The marketing process was extensive but ultimately unsuccessful. Bank of America conducted outreach from 2022 to 2024, presenting the program to five companies, of which one advanced to formal diligence but ultimately withdrew. Evercore expanded the effort from 2024 to 2026, contacting more than twenty parties — resulting in nine management presentations, seven formal diligence processes, and three term sheets. No deal closed. One party could not meet the requested economic terms; another was acquired during the process and withdrew; and the party that progressed furthest withdrew prior to signing over board-level concerns that the FDA might require an entirely new, large-scale clinical trial as a precondition to approval — a concern that reflected broader regulatory uncertainty in the gene therapy landscape at the time.

Sangamo made significant progress on regulatory clarity, but timing proved too late. October 2024 FDA written minutes confirmed the Company's existing patient study could serve as the primary basis for marketing approval, accelerating the anticipated approval timeline by approximately three years. A second FDA meeting in October 2025 reaffirmed the accelerated approval pathway in writing. The Company began a rolling BLA submission in December 2025 and presented patient study results across four presentations at the 22nd Annual WORLDSymposium in early 2026.

Recognizing that residual partner concerns over a potential new trial persisted despite the two FDA confirmations, the Company retained First Principles Strategies and regulatory counsel Frank Sasinowski of Hyman, Phelps & McNamara, P.C., submitting formal correspondence to the FDA in April 2026 seeking express written confirmation. In May 2026, the Acting Director of the FDA's Office of Therapeutic Products confirmed in writing that no separate large-scale clinical trial would be required as a precondition to approval — directly resolving the concern that had driven multiple prospective partners away. Although the confirmation arrived too late to address the Company's liquidity needs outside of a court-supervised process, it proved instrumental in re-engaging Astellas as the stalking horse bidder for the Fabry Disease Program.

Liquidity Deterioration and Nasdaq Delisting

Across fiscal years 2023 through 2025, Sangamo absorbed aggregate net losses exceeding $478 million as revenues declined more than 77%, from $176.2 million in 2023 to $39.6 million in 2025. Cash, equivalents, and marketable securities collapsed from $307.5 million at year-end 2022 to $20.9 million at year-end 2025, and every annual and quarterly report through the period carried a going-concern qualification.

On April 28, 2026, Nasdaq notified Sangamo of its determination to delist the Company's common stock; trading was suspended and the shares commenced trading on the OTCQB Venture Market under the ticker symbol "SGMO" on May 5, 2026.

With no out-of-court path to its liquidity needs, the Board on June 18, 2026 determined that a court-supervised Chapter 11 sale process was the best available means to maximize value — the subject of the filing detailed below.

The Chapter 11 Filing

Sangamo filed for Chapter 11 with two stalking horse asset purchase agreements already executed — one with Eli Lilly and Company, through its wholly owned subsidiary Merope Acquisition Sub, LLC, for the Lilly Assets and one with Astellas Gene Therapies, Inc. for the Fabry Disease Program.

Lilly Stalking Horse Sale (Platform Sale)

Merope Acquisition Sub, LLC, with Eli Lilly and Company as guarantor of payment and performance on a primary-obligor basis, agreed to acquire substantially all of Sangamo's core technology assets — referred to in the Declaration as the "Lilly Assets" and in the asset purchase agreement as the "Merope Assets" — for $50 million cash plus assumption of only post-closing obligations under the acquired contracts. The acquired assets span the SIFTER, MINT, and ZFP technology platforms; all proprietary capsids including STAC-BBB, STAC-150, and next-generation variants; the proprietary capsid receptors and related technology; the Prion Disease Program (ST-506); all related intellectual property; and the right to receive future milestone and royalty streams under the outlicensing agreements — including those with Genentech, Takeda, Alexion, and the December 2024 Astellas capsid license — to the extent those streams relate to the acquired technology.

Those payment rights transfer to Lilly either through assumption and assignment of the underlying agreements or through rejection coupled with court findings that the noncompete provisions in those agreements are not binding on Merope or its affiliates post-closing. Obtaining those findings — or negotiating acceptable new or amended license agreements with the relevant outbound licensees — is a hard closing condition; Merope is not obligated to close without it.

All cure costs, prepetition employee, WARN, COBRA, tax, lease, and litigation liabilities remain with the estate. The sale is on an as-is, where-is basis, no buyer deposit is required, and the outside date is September 30, 2026.

Astellas Stalking Horse Sale (Fabry Program Sale)

Astellas Gene Therapies, Inc. agreed to acquire substantially all assets of the Fabry Disease Program — principally isaralgagene civaparvovec (ST-920), its IND and rolling BLA submission, STAAR study data, related intellectual property, and inventory — for $25 million cash at closing plus up to $25 million in contingent milestone payments.

The milestone consideration is structured as two equal $12.5 million tranches. The first, the Accelerated Milestone, is triggered by the first FDA accelerated approval of the U.S. Fabry BLA based on the STAAR Studies. The second, the Full Milestone, is triggered by first full approval or conversion from accelerated approval. Both tranches exclude approvals requiring a new pivotal study beyond the STAAR Studies or carrying a Boxed Warning, a Risk Evaluation and Mitigation Strategy, or a second-line-only restriction. The structure is buyer-favorable: Astellas owes no affirmative duty to pursue either milestone beyond an obligation not to delay the full-approval submission in bad faith, rendering the contingent $25 million back-loaded and uncertain.

Closing is conditioned on retention of at least 80% of identified key personnel immediately prior to closing. All cure costs, prepetition employee, WARN, COBRA, tax, lease, and litigation liabilities remain with the estate, consistent with the Lilly sale structure. No buyer deposit is required and the outside date is September 15, 2026.

At closing, Astellas grants the estate a non-exclusive, perpetual, royalty-free license back under certain acquired intellectual property, including rights to STAC-BBB and the Hemophilia A program, preserving the excluded assets and the technology transferred to Lilly under the Merope sale.

Bid Protections and Auction Timeline

Each stalking horse holds bid protections treated as superpriority administrative expense claims senior to all other administrative expenses, including those arising under the DIP facility.

For the Lilly sale, Merope is entitled to a $1.5 million break-up fee representing 3% of the $50 million purchase price, plus up to $500,000 in expense reimbursement representing 1%. The break-up fee is credit-biddable by Merope at any subsequent auction. For the Astellas sale, Astellas is entitled to a $1.0 million termination fee representing 4% of the $25 million closing consideration, plus up to $500,000 in expense reimbursement. The termination fee is payable only upon specified termination events and solely from the proceeds of a competing transaction at closing; the expense reimbursement is payable on a broader set of termination events.

To submit a Qualified Bid, a competing bidder must beat the applicable stalking horse consideration plus its bid protections plus a $250,000 initial overbid increment — implying a minimum of approximately $52.25 million cash to top Lilly and approximately $26.75 million to top Astellas — with subsequent overbids in minimum $100,000 increments. Each competing bidder must post a good faith deposit equal to 10% of the cash portion of its bid, submit a marked-up asset purchase agreement with committed financing and board authorization, and bid without financing, diligence, or internal-approval conditions.

The Debtor is also seeking authority to designate additional stalking horse bidders for the Remaining Assets — the Chronic Neuropathic Pain Program, Hemophilia A Program, Sickle Cell Disease Program, and Tregs Platform — with any associated bid protections capped at 3% of the applicable purchase price.

The proposed sale calendar, subject to court approval, is as follows:

- Bid Deadline July 25, 2026;

- Qualified Bid designation July 29;

- Sale Objection deadline July 31;

- Auction August 4, 2026;

- Sale Hearing on or about August 11;

- Sale Order entry August 14;

- Outside closing date August 29, 2026, with contractual outside dates of September 15, 2026 under the Astellas APA and September 30, 2026 under the Lilly APA if closing slips.

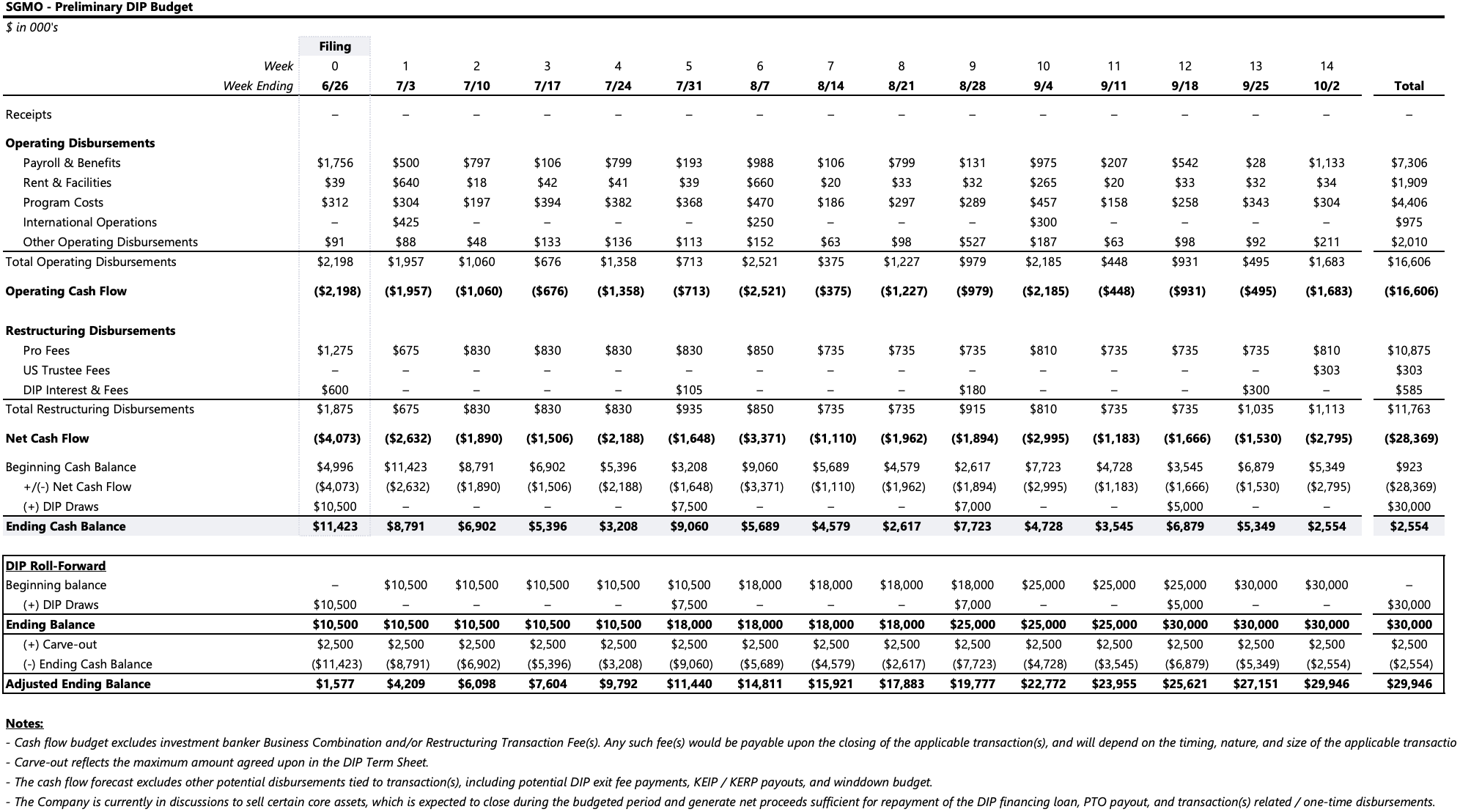

DIP Financing

The case is financed by a $30 million senior secured superpriority new-money term loan from Northridge ATM, LLC, with no roll-up and no adequate-protection package — the estate carries no prepetition secured debt. Up to $10.5 million is available on the interim order, with the balance available upon entry of the final order, in each case drawn against a 13-week budget. Pricing includes 12% cash interest (plus 2% on default), a 2% commitment fee and 5% exit fee each calculated on the full $30 million commitment and fully earned upon entry of the interim order regardless of amounts drawn, and a $75,000 prepetition work fee paid June 15, 2026.

Avoidance actions are pledged as collateral — section 549 claims upon the interim order, all remaining chapter 5 claims upon the final order — and Northridge holds an unqualified right to credit-bid the full DIP balance at any sale. Budget compliance is enforced through a 15% cumulative net-operating-variance ceiling. Continued access to funding is conditioned on the stalking horse agreements remaining in effect and unamended without the lender's consent; termination of either agreement is independently an event of default.

The Carve-Out preserves U.S. Trustee and Clerk fees, up to $50,000 in chapter 7 trustee fees if applicable, budgeted prepetition professional fees, and a $2.5 million post-trigger professional fee cap. Maturity is the earliest of December 30, 2026, a plan effective date, a sale of substantially all assets (individual Lilly and Astellas closings excluded), an event of default, dismissal or conversion, or 35 days post-petition absent a final order.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.