Case Summary: Hallmark Financial Chapter 11

Hallmark Financial filed Chapter 11 to sell its business or swap controlling creditor Hildene's debt for equity, after reserve failures, a lost reinsurance arbitration, and a ratings collapse gutted its equity—tripping a senior-note covenant Hildene wouldn't waive, foreclosing an out-of-court fix.

Business Description

Headquartered in Dallas, TX, Hallmark Financial Services, Inc. ("Hallmark" or the "Debtor") is a diversified property and casualty insurance holding company that, through its operating subsidiaries, underwrites, markets, and distributes specialty and niche products nationwide on an admitted basis. Hallmark's business is conducted entirely through two classes of non-debtor operating subsidiaries: licensed insurance carriers (the "Insurance Subsidiaries") and managing general agents (the "MGA Subsidiaries"). As of the Petition Date, those subsidiaries hold admitted carrier licenses in 49 states, MGA licenses in 48 states, and excess and surplus carrier eligibility in 44 states, with active business operations across 48 states.

The parent entity — the sole debtor in this case — generates revenue through management fees and commissions earned by its MGA Subsidiaries in exchange for services rendered to the Insurance Subsidiaries. The licensed insurance carriers and managing general agents continue operating in the ordinary course while their parent completes a balance-sheet restructuring through these proceedings.

Hallmark Financial Services, Inc. filed for Chapter 11 protection on June 15, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Northern District of Texas (Dallas Division), reporting approximately $10 million to $50 million in assets and $100 million to $500 million in liabilities.

Corporate History

Founded in 1987 and incorporated in Nevada, Hallmark evolved over nearly four decades from a Texas-only non-standard automobile insurer and premium-finance company into a diversified specialty property and casualty insurer writing specialty commercial, standard commercial, and personal lines across the United States. Hallmark was a publicly listed corporation with its common stock trading on the Nasdaq under the ticker symbol HALL, until it voluntarily delisted on January 5, 2024 and terminated its SEC registration on January 16, 2024, citing adverse market conditions and other factors.

Strategic Exits and Divestitures

- Workers' Compensation Exit (effective July 1, 2015) — Ceased marketing or retaining any risk on new or renewal workers' compensation policies, placing the business unit into run-off administered by an independent third party.

- Occupational Accident Exit (effective June 1, 2016) — Ceased marketing new or renewal occupational accident policies, which had been offered through the Commercial Accounts business unit via a specialized underwriting agency in Texas.

- Contract Binding Primary Commercial Automobile Exit (February 2020) — Hallmark exited the contract binding line of its primary commercial automobile business, citing increasing claim severity and limited opportunity for meaningful rate increases. Non-renewal of in-force policies and transition to run-off commenced in accordance with state regulatory guidelines. This line had produced $115.0 million in gross premiums written during 2019, representing 56% of the Commercial Auto business unit's total primary automobile premium volume.

- Specialty Commercial / E&S Operations Sale (effective September 30, 2022; closed October 7, 2022) — Sold substantially all of its excess and surplus lines operations — comprising nine business units within the Specialty Commercial segment, including the agency subsidiary Heath XS, LLC — to an affiliate of Core Specialty Insurance Holdings, Inc. for $40.0 million in cash consideration plus approximately $19.9 million for net unearned premium reserves. Approximately 200 employees transitioned to Core Specialty at closing. Unassumed claims were placed into run-off.

- Aviation MGA Subsidiary Sale (effective June 30, 2025) — Sold Aerospace Insurance Managers, a wholly owned managing general agent subsidiary specializing in aviation insurance, to Bishop Street Underwriters, generating net proceeds of approximately $30.9 million after fees and expenses.

Leadership and Governance

Hallmark Financial Services is governed by a four-member board of directors chaired by Mark E. Schwarz, alongside directors Scott Berlin, Mark Pape, and Doug Slape. Christopher J. Kenney serves as President, Chief Executive Officer, and Chief Financial Officer, and signed the Chapter 11 petition in that capacity. William Snyder of Oliver Wyman was appointed Chief Restructuring Officer effective June 11, 2026, pursuant to board resolution adopted that date, reporting directly to the board.

Equity ownership is concentrated and layered. Three holders of record own 10% or more of the Debtor's equity: Raymond James & Associates, Inc. (36.29%), Charles Schwab & Co., Inc. (13.6%), and NFS LLC c/o Cede & Co. (11.5%). However, Raymond James holds its 36.29% block solely in a custodian and nominee capacity on behalf of three beneficial owners: Chairman Schwarz, who owns approximately 66% of that block; Hallmark Financial Services, Inc. itself, which owns approximately 33%; and other parties collectively holding less than 1%. Raymond James receives no economic benefit tied to those positions beyond customary custodial and account-related fees, and the personnel associated with those accounts are not involved in Raymond James's engagement as investment banker to the Debtor.

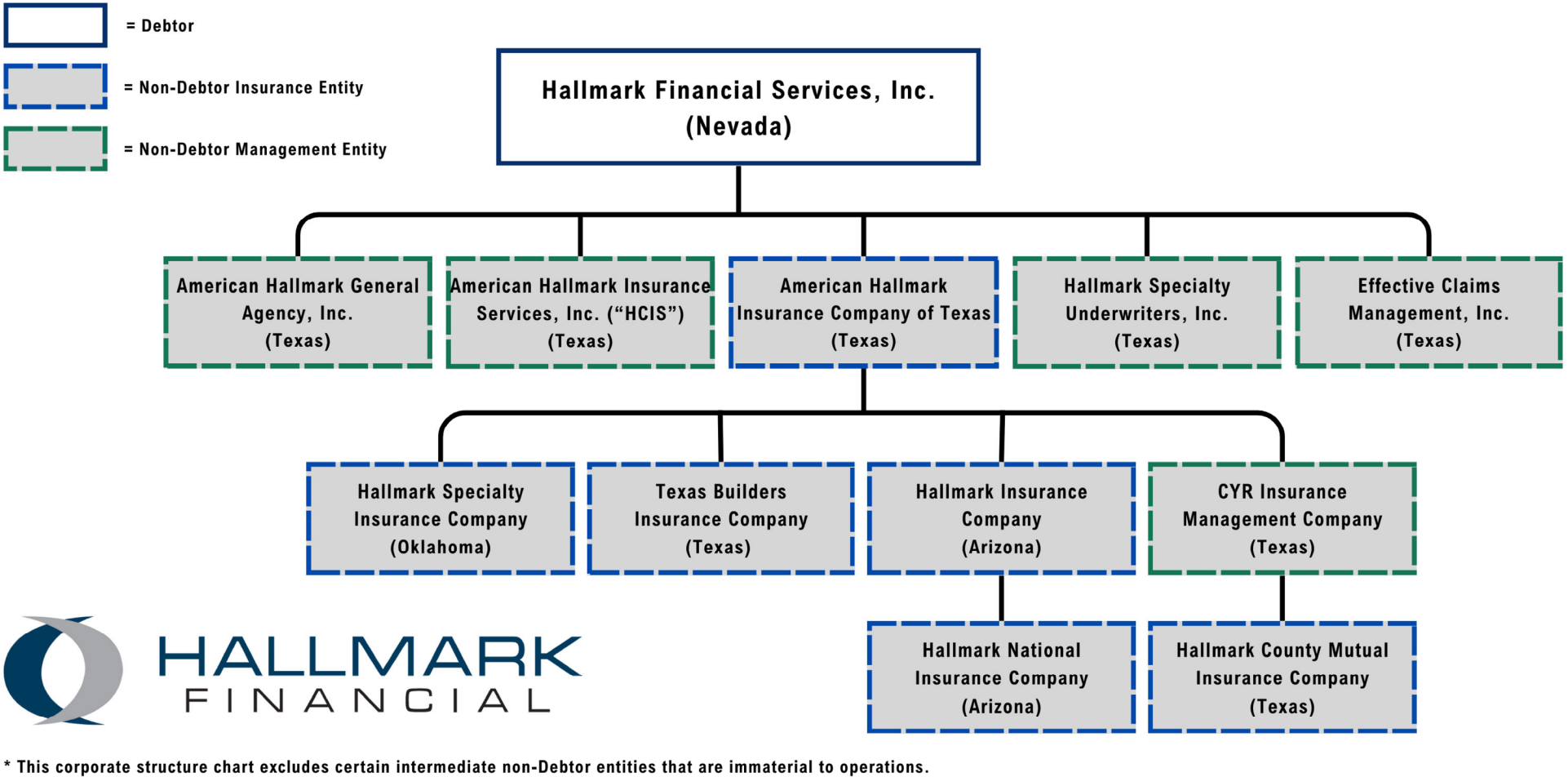

Corporate Structure

Operations Overview

Business Segments

Hallmark historically organized its insurance operations across three business units — commercial lines, personal lines, and specialty commercial lines, with the specialty commercial lines divested in 2022. Each business unit operates with its own dedicated management team and is independently responsible for marketing, distribution, and underwriting within its respective market, while the parent company provides centralized support functions including capital management, claims management, reinsurance, actuarial, investment, financial reporting, technology, and legal services. Revenue flows to the parent through its MGA Subsidiaries, which earn commissions and fees for services rendered to the Insurance Subsidiaries pursuant to a management agreement. In recent years, Hallmark has materially contracted its operational footprint through a combination of voluntary run-offs, third-party reinsurance arrangements, and outright asset sales.

- Commercial Lines — The commercial lines segment operates through Hallmark's commercial accounts business unit, which underwrites low-severity, short-tailed property and casualty products in the standard admitted market. Products are distributed through a network of 242 independent agency groups serving non-urban businesses across 16 states, concentrated in the southwest and northwest regions. The segment's product suite comprises commercial automobile, general liability, umbrella, commercial property, commercial multi-peril, and business owner's coverage. The segment previously included workers' compensation and aviation business units; workers' compensation ceased writing new policies effective July 1, 2015 and is administered in run-off by an independent third party, while the aviation business was sold to a third-party purchaser effective June 30, 2025.

- Personal Lines — A specialty personal lines business unit that markets and services non-standard personal automobile policies and renters insurance across 10 and 12 states, respectively. The segment serves drivers who find it difficult to purchase automobile insurance from standard carriers due to factors including driving record, vehicle, age, claims history, or limited financial resources, generally providing the minimum limits of liability coverage mandated by state laws. The segment's product suite includes personal automobile policies, which provide third-party bodily injury and property damage coverage at statutory minimum limits as well as first-party physical damage and, where required, no-fault personal injury protection coverage, and renters policies, which provide coverage similar to homeowners insurance except that the structure itself is not covered.

- Run-Off Segment — In addition to its ongoing business units, Hallmark also maintains a “run-off” segment where the company continues to process claims on certain business lines for which its Subsidiaries no longer write new policies. This includes the commercial automobile, senior care facilities, and satellite launch business lines.

Subsidiary Structure

Hallmark's operating subsidiaries fall into two categories.

- The Insurance Subsidiaries include Hallmark Insurance Company, Hallmark Specialty Insurance Company, Hallmark National Insurance Company, and American Hallmark Insurance Company of Texas, Hallmark County Mutual Insurance Company, and Texas Builders Insurance Company.

- The MGA Subsidiaries include American Hallmark General Agency, Inc. and Hallmark Specialty Underwriters, Inc.

Through these non-debtor Subsidiaries, the Debtor offers commercial and personal insurance solutions to businesses and individuals in specialty and niche markets on an admitted basis. The business lines include underwriting and servicing property and casualty insurance products that require specialized underwriting expertise and market knowledge.

Management Services Agreement

On November 7, 2025, Hallmark Financial Services, Inc. entered into the Management Services Agreement with five wholly owned non-debtor MGA subsidiaries — American Hallmark Insurance Services, Inc., American Hallmark General Agency, Inc., Hallmark Specialty Underwriters, Inc., CYR Insurance Management Company, and Effective Claims Management, Inc. — under which HFS provides centralized management and administrative services across treasury and cash management, accounts payable, payroll and benefits, accounting and finance, legal and compliance, information technology, facilities, and human capital functions on behalf of the subsidiaries.

Subsidiary cash receipts are swept daily into HFS-maintained collection accounts, with HFS disbursing funds on behalf of each subsidiary and maintaining intercompany ledgers to track the net balance attributable to each entity. On pricing, the MSA takes a cost-recovery approach — HFS charges each subsidiary its direct out-of-pocket costs plus an allocable share of shared overhead, with no markup permitted for regulated insurance subsidiaries absent regulatory approval, with fees accruing monthly and settling through the intercompany ledger. The MSA runs for an initial ten-year term with automatic five-year renewals, and explicitly subordinates all intercompany obligations to policyholder claims, insulating the regulated insurance subsidiaries from any cash management mechanics that could conflict with state insurance law.

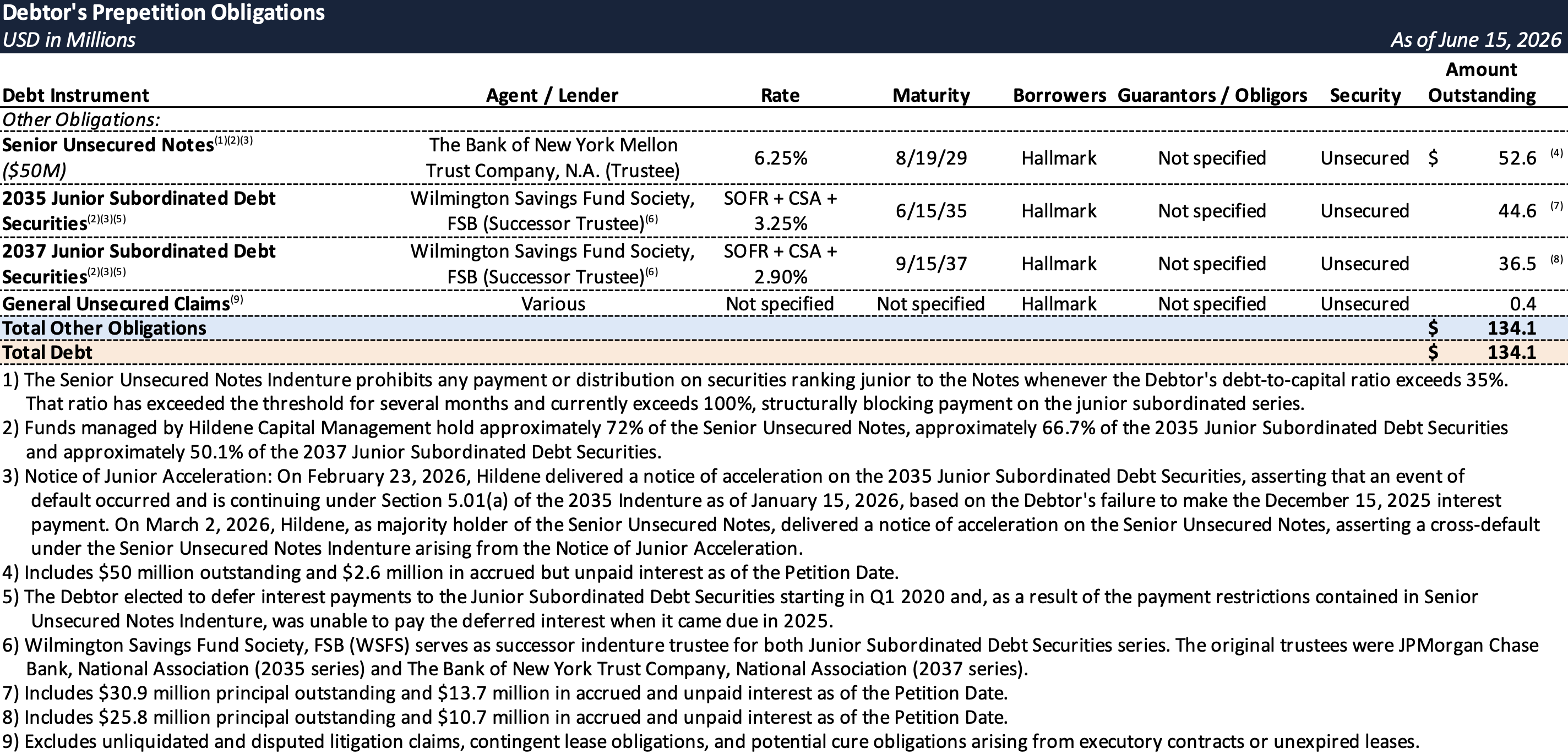

Prepetition Obligations

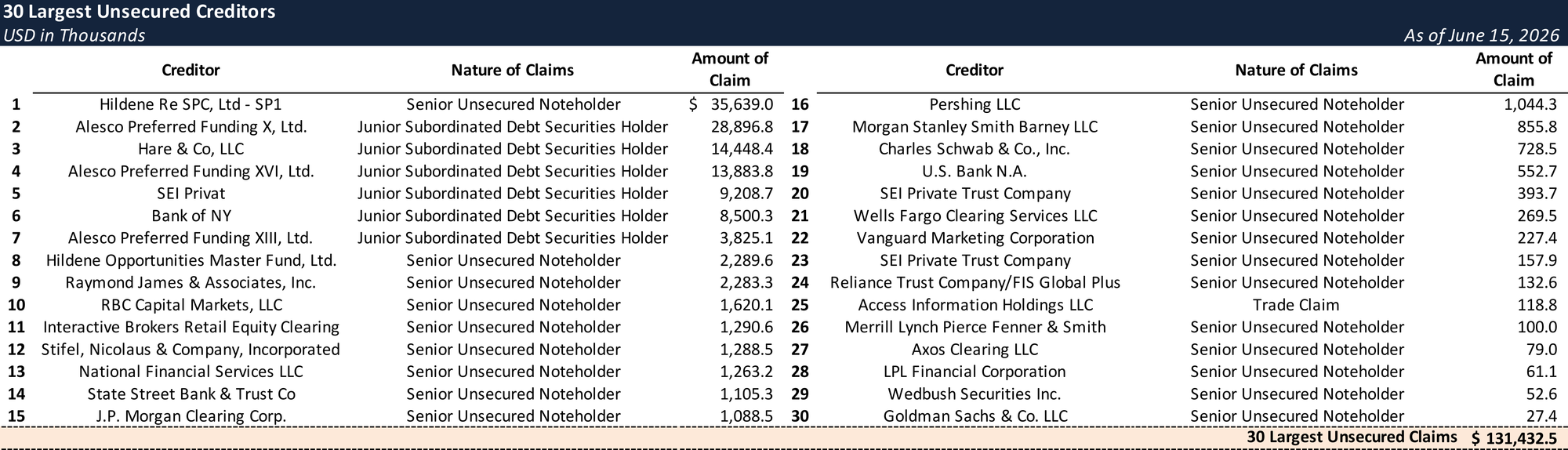

Top Unsecured Claims

Events Leading to Bankruptcy

This is a parent-only, balance-sheet failure—not an operating insolvency of the carriers. The distress traces to legacy casualty-reserve deterioration that metastasized through a contested reinsurance transaction, a ratings collapse, and the run-off of a divested segment, until a single senior-note covenant blocked any consensual out-of-court cure even after the Debtor had the cash to pay.

Loss Portfolio Transfer and DARAG Arbitration

Beginning in late 2019 and early 2020, Hallmark began experiencing greater losses in certain portfolios than in prior years, most acutely in its binding primary commercial automobile book, where increasing claim severity across the 2016 and 2017 underwriting years had accumulated to unsustainable levels. On March 2, 2020, Hallmark publicly announced its exit from the binding primary commercial auto business and disclosed $63.8 million of pre-tax adverse prior-year loss development, net of reinsurance, for fiscal 2019. To cap the exposure arising from the run-off of this book, Hallmark's subsidiaries entered into a Loss Portfolio Transfer Reinsurance Contract (the "LPT Contract") with DARAG Bermuda Ltd. and DARAG Insurance (Guernsey) Limited, executed July 16, 2020, consummated July 31, 2020, and effective as of January 1, 2020, under which Hallmark ceded approximately $172.9 million in gross reinsurance premium against an aggregate reinsurance limit of $240.0 million.

Not long after closing, DARAG commenced arbitration against Hallmark and its subsidiaries alleging misrepresentations in the LPT Contract. The proceedings resulted in two adverse awards: an interim award that produced a $32.9 million write-off in the first quarter of 2023, followed by a final, binding award on June 2, 2023 that added a further $4.0 million — yielding a total aggregate write-off of approximately $36.9 million, exceeding Hallmark's pre-award estimate of $25 to $35 million. The final award resulted in the termination of the LPT Contract. The First Day Declaration references only the June 2, 2023 final award and the $25–$35 million pre-award estimate.

AM Best Ratings Downgrade and Withdrawal

The DARAG arbitration loss had consequences beyond the immediate balance sheet impact. Prior to the ruling, Hallmark's insurance subsidiaries held an A- (Excellent) financial strength rating from A.M. Best, which Hallmark considered essential to their ability to write commercial insurance policies. Following the May 4, 2023 interim arbitration award, AM Best downgraded Hallmark's ratings in two steps: on May 5, 2023 it cut the insurance subsidiaries' FSR from A- (Excellent) to B++ (Good) and the parent's Long-Term ICR from "bbb-" (Good) to "bb" (Fair); on May 9, 2023 it cut the FSR further to C++ (Marginal) and the parent ICR to "ccc-" (Weak), all under review with negative implications. On May 15, 2023, at Hallmark's request to exit AM Best's interactive rating process, AM Best withdrew the ratings altogether.

Stripped of the rating its carriers needed to write business, Hallmark resorted to "fronting" on other carriers' higher-rated paper—a workable but margin-eroding fix that compressed profitability and left subsidiary earning power impaired pending a rating restoration.

Sale of the Specialty Commercial Segment

While the DARAG arbitration was ongoing in 2022, Hallmark elected to exit the specialty commercial segment entirely, driven in large part by a higher than usual volume of claims exceeding reserves. On October 7, 2022, Hallmark consummated the sale of substantially all of its excess and surplus lines operations — comprising nine business units within the specialty commercial segment — to an affiliate of Core Specialty Insurance Holdings, Inc., with approximately 200 employees transitioning to the acquirer. The transaction did not result in the assumption of all claims, and unassumed claims were placed into run-off. Because claims in the specialty commercial portfolio exceeded reserve amounts, the segment caused significant balance sheet losses, forcing Hallmark to fall out of compliance with the 35% debt-to-capital ratio covenant under the Senior Unsecured Notes Indenture.

Director and Officer Litigation

The DARAG arbitration exposed alleged misconduct by former CEO Naveen Anand and former Chief Actuary Kenneth Krissinger, prompting Hallmark to retain outside advisors to investigate. Before Hallmark could act, Anand filed a declaratory judgment action on December 18, 2024 seeking advancement of legal expenses, forcing Hallmark to assert compulsory counterclaims for breach of fiduciary duty and fraudulent concealment — alleging that Anand and members of his senior executive team suppressed claim reserves in 2018 and 2019, concealing this from auditors, the board, and DARAG. On June 11, 2026 — four days before the Petition Date — the Court partially granted Anand's summary judgment motion on advancement, ordered Hallmark to advance his legal fees, denied Anand's motion to dismiss Hallmark's breach of fiduciary duty counterclaim, and granted dismissal of the contribution claim. Trial is scheduled for February 2027.

Separately, on October 10, 2025, Hallmark filed a petition against Krissinger in the Business Court of Texas concerning his role in the reserve suppression scheme. Krissinger removed the case to the Northern District of Texas, answered the complaint, and asserted a counterclaim for advancement. Hallmark argued Krissinger is not entitled to advancement because he was not an "officer" under the company's bylaws — distinguishing him from Anand. Trial is scheduled for July 2027.

Prepetition Sale Efforts

By late 2024, it had become apparent that Hallmark would require a balance sheet restructuring or capital infusion to satisfy deferred interest obligations on the Junior Subordinated Debt Securities, which were scheduled to come due by year-end 2025. In December 2024, Hallmark engaged Raymond James to explore a possible sale of some or all of its subsidiary businesses. Raymond James went to market in spring 2025, contacting 164 total industry participants — 80 prospective financial buyers and 84 potential strategic buyers. Approximately 52 signed NDAs, 10 submitted indications of interest, and three submitted formal letters of intent, including at least one proposal contemplating an acquisition of the entire enterprise. Hallmark concluded the enterprise proposal was not actionable due to insufficient consideration.

Raymond James separately received three letters of intent for Aerospace Insurance Managers ("AIM"), Hallmark's aviation MGA subsidiary, and ultimately reached an agreement with Bishop Street Underwriters to acquire AIM. The transaction closed June 30, 2025, generating net proceeds of approximately $30.9 million.

Notice of Acceleration

Although the Aviation Sale Proceeds were sufficient to pay the deferred interest due on the Junior Subordinated Debt Securities, the terms of the Senior Unsecured Notes Indenture prohibited distributions on junior-ranking securities while the debt-to-capital ratio exceeded 35% — a threshold Hallmark had long since breached. Hallmark sought consent from the Senior Unsecured Noteholders to make the junior interest payments but was unsuccessful. On February 23, 2026, Hildene delivered a Notice of Acceleration on the 2035 Junior Subordinated Debt Securities, asserting an event of default under Section 5.01(a) of the 2035 Indenture as of January 15, 2026, based on Hallmark's failure to make the December 15, 2025 interest payment. On March 2, 2026, Hildene, as majority holder of the Senior Unsecured Notes, delivered a Notice of Acceleration on the Senior Unsecured Notes, asserting a cross-default arising from the Notice of Junior Acceleration.

Chapter 11 Filing

The Plan's economic core is a debt-for-control equitization: Hildene converts its majority holdings across Hallmark's ~$134 million debt stack—roughly 72% of the Senior Notes and the majority of both junior series—into ownership of the reorganized company, while non-Hildene holders are cashed out or reinstated.

The Restructuring Support Agreement

Following extensive arm's-length negotiations, the parties executed a Restructuring Term Sheet on March 27, 2026, and a Restructuring Support and Forbearance Agreement on April 3, 2026, embedding a dual-track toggle structure: a go-shop marketing process targeting Alternative Restructuring Transactions at a minimum value of approximately $51.2 million, and a fallback pre-negotiated plan of reorganization if no qualifying bid emerges. As part of the RSA, Hildene agreed to forbear from exercising remedies against the Debtor from the RSA effective date through the earlier of the Petition Date or the RSA's termination, and to direct the applicable indenture trustees not to exercise remedies to the extent directed by other noteholders.

The Dual-Track Toggle

The Plan implements a dual-track toggle. Hildene's Restructuring Transaction serves as the stalking-horse backstop, while the Debtor simultaneously runs a go-shop soliciting a higher or better, all-cash Alternative Restructuring Transaction priced above the Initial Plan Value. On or around April 1, 2026, Raymond James launched the RSA-mandated marketing process, contacting 173 total industry participants — 81 prospective financial buyers and 92 potential strategic buyers. Sixty-one signed NDAs, two submitted indications of interest, and three submitted formal letters of intent. If the market clears the floor, the Debtor sells; if not, it consummates the pre-negotiated Hildene deal.

The Initial Plan Value is not an enterprise appraisal but a contractual floor derived from a claims formula: broadly, the Senior Unsecured Notes Claims (including accrued interest), plus 10% of the Junior Subordinated Debt Securities Claims (including accrued interest), plus estimated unpaid professional fees, administrative claims, and GUCs, less the Debtor's cash and investments as of the Plan Effective Date. Owing to differing measurement dates and component estimates across the filings, the figure appears as approximately $51.2 million in the Declaration (Doc. 15 ¶48), approximately $47 million in the Disclosure Statement's summary build (Doc. 18 §I.A), and approximately $46 million in the risk factors section of the same document (Doc. 18 §V.B.3) — three references to the same contractual construct, each reflecting a different snapshot date or rounding convention rather than a substantive disagreement.

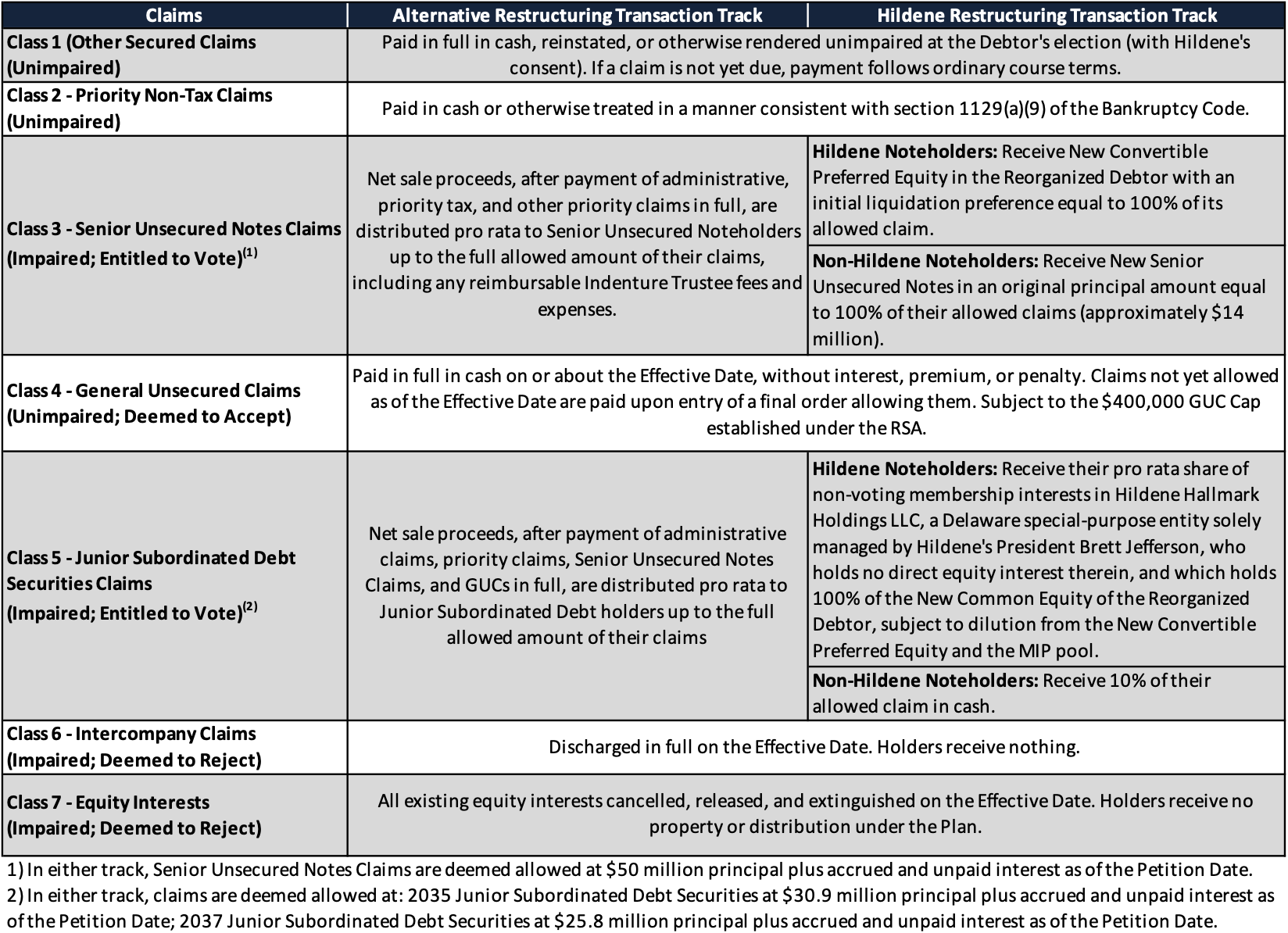

Treatment of Claims

Bidding Procedures

Hildene is the Stalking Horse Bidder at the Initial Plan Value. Notably, the Debtor sought no break-up fee, no expense reimbursement, no bid protections, and no no-shop (Doc. 20). A Qualified Bid must be all cash exceeding the floor by at least $100,000, with no diligence or financing contingencies and a 10% deposit; Hildene is a deemed Qualified Bidder, posts no deposit, and tops with cash rather than credit-bidding. The Bid Deadline is July 30, 2026; the auction, if needed, is August 4, 2026. As of the Disclosure Statement, no actionable competing bid above the floor had emerged.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.