Case Summary: Searles Valley Minerals Chapter 11

Searles Valley Minerals filed Chapter 11 to pursue a §363 going-concern sale of its business — anchored by its Trona, CA mining complex — after 2019 Ridgecrest earthquake damage, soda ash oversupply and price collapse, and mounting losses left it no viable out-of-court path.

Business Description

Headquartered in Overland Park, Kansas, with its core operating complex in Trona, California, Searles Valley Minerals Inc. ("SVM"), together with its Debtor⁽¹⁾ and non-Debtor affiliates (collectively, the "Company"), is a vertically integrated mining and processing company employing approximately 280 people as of the Petition Date. The Company produces critical industrial minerals including borates - sold commercially as V-BOR (borax pentahydrate), its primary refined borate product, sodium sulfate, and salt — and until recently soda ash — sourced from one of only four known water-soluble sodium borate (tincal) reserves in the world, one of only five natural soda ash mining locations in the United States, and the second largest boron deposit globally.

The Company serves a diversified customer base across industrial, agricultural, and specialty chemical end markets concentrated in Southern California and Baja, Mexico, with its minerals feeding into everyday manufactured products including beverage and pharmaceutical glassware and laundry detergents. Two subsidiary debtors round out the enterprise: Searles Domestic Water Company LLC ("SDWC"), which operates a water treatment facility serving Trona residents, and Trona Railway Company LLC ("TRC"), which runs a short-line railway connecting SVM's facilities to the Union Pacific main line for product delivery.

Searles Valley Minerals Inc. and certain affiliates filed for Chapter 11 protection on June 15, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the District of Delaware, reporting approximately $100 million to $500 million in both assets and liabilities.

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

Mining operations at Searles Lake date back more than 150 years, originating with John Searles, who discovered the lake in 1862 while prospecting for gold, and his brother Dennis, who founded the San Bernardino Borax Mining Company to commence borax extraction.

The business changed hands multiple times before its most recent acquisition in 2007, when SVM's predecessor was acquired by its current sponsor, Nirma Limited ("Nirma"), a manufacturer of detergents, soaps, and salts headquartered in Ahmedabad, Gujarat, India. Nirma and its affiliate Navin Overseas FZC ("Navin") are also customers of SVM, purchasing approximately $9.8 million, $9.2 million, and $6.2 million of V-BOR in calendar years 2023, 2024, and 2025, respectively, alongside soda ash purchases of less than $1 million annually in 2024 and 2025. While sales to Nirma and Navin are on customary market terms, both entities began prepaying SVM for V-BOR several years ago to help offset the Company's deteriorating liquidity position.

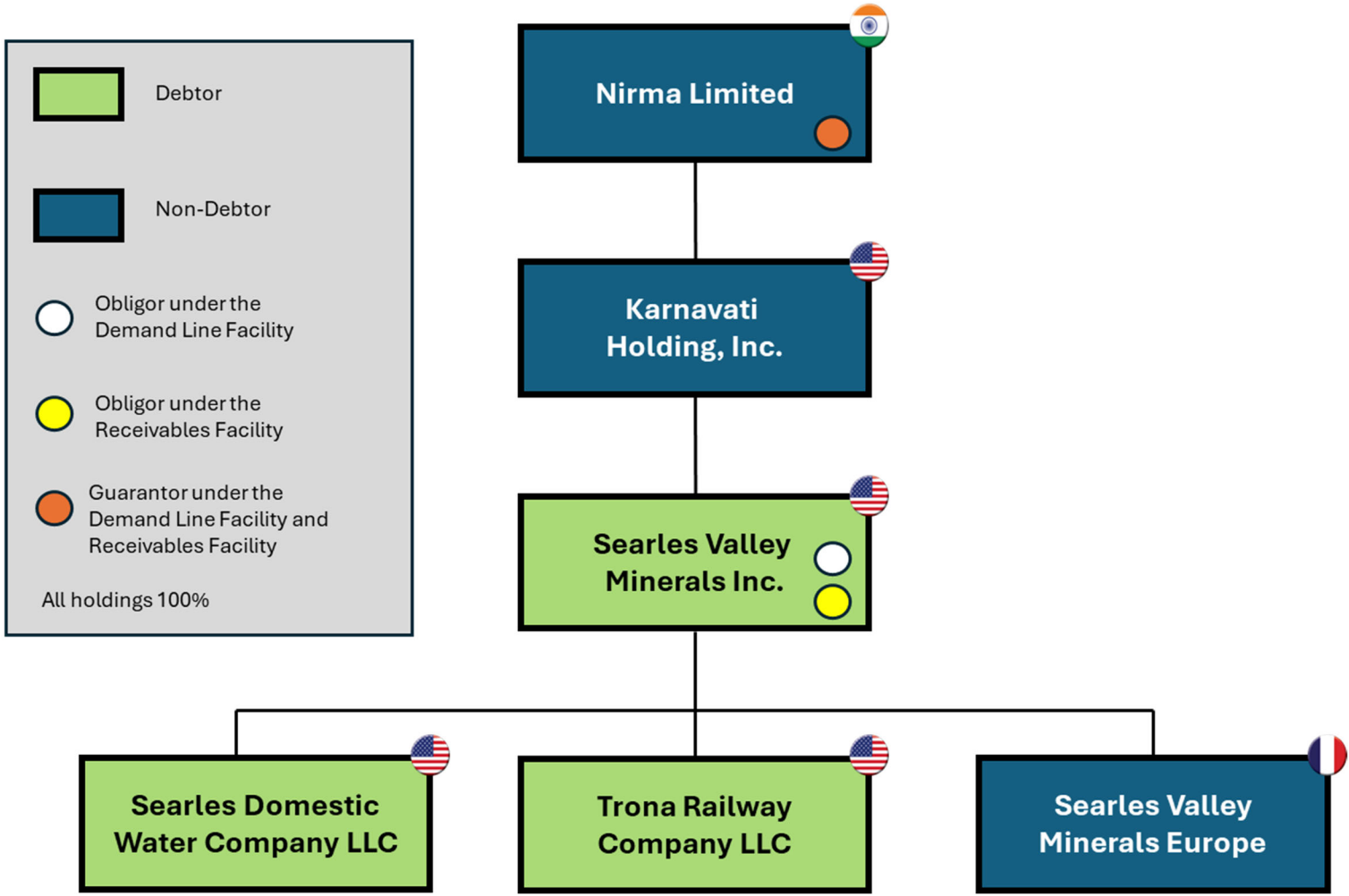

Organizational Structure

Searles Valley Minerals Inc. is the direct parent of both Trona Railway Company LLC and Searles Domestic Water Company LLC, each incorporated in Delaware. Searles Valley Minerals Inc. also holds 100% of Searles Valley Minerals Europe, a French entity that historically served as an international sales outpost but currently conducts no business. Searles Valley Minerals Inc. itself is wholly owned by Karnavati Holdings, Inc. ("KHI"), a Delaware corporation, which in turn is wholly owned by Nirma Limited.

Operations Overview

Warm Solution Mining ("WSM")

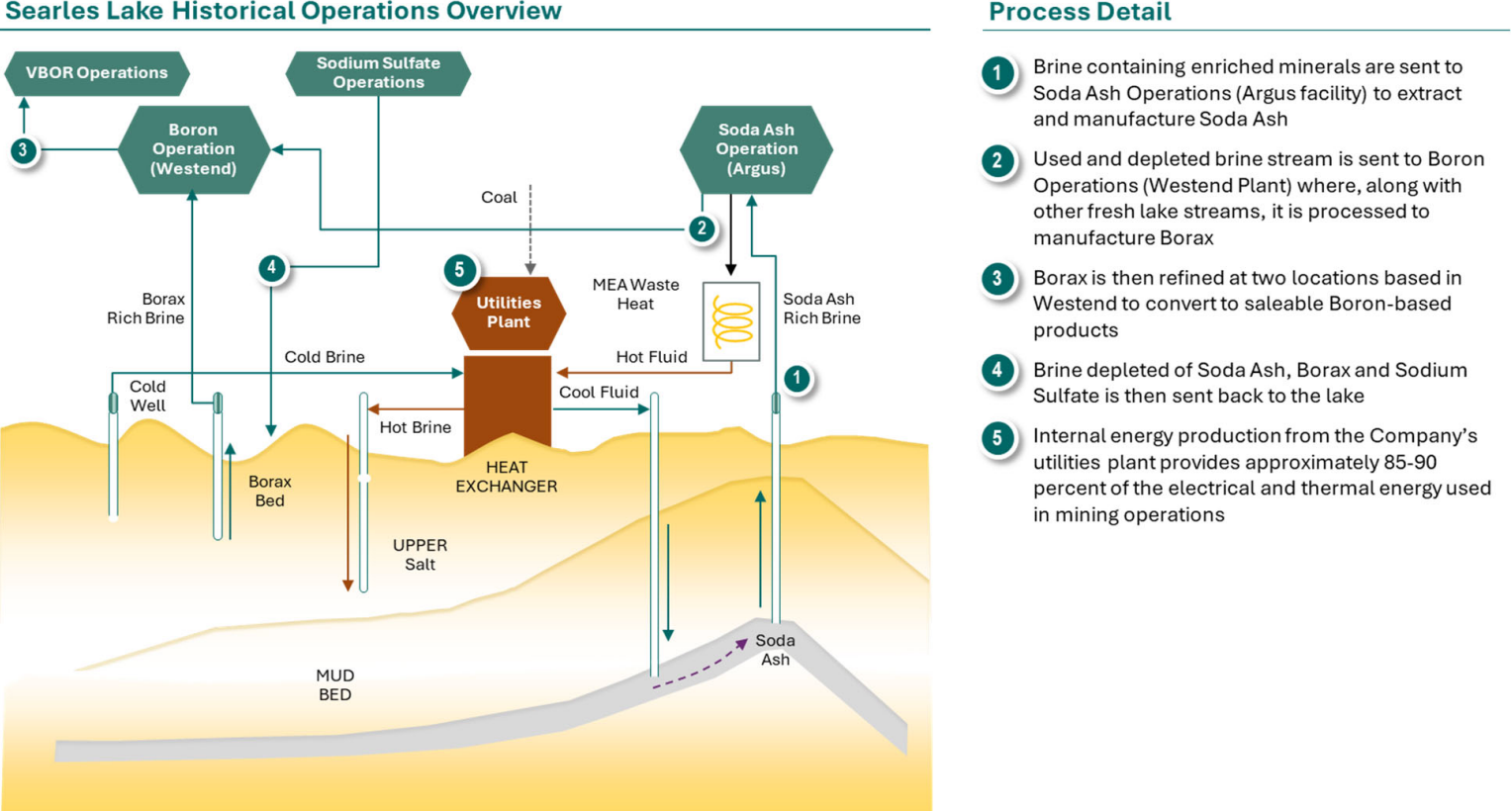

Rather than traditional open-pit mining, SVM extracts minerals from Searles Lake's dry lakebed through Warm Solution Mining ("WSM"), an environmentally friendly process. Hot brine is injected into subsurface mineral deposit layers through injection wells, dissolving the minerals underground, after which the resulting mineral-rich brine is pumped back to the surface through production wells. The wells are organized along "borax roads," each containing five production wells and 30 injection wells, positioned in the Upper Salt Brine layer approximately 30 to 70 feet beneath the lake surface — the zone where most of the borax is concentrated.

Processing Plants

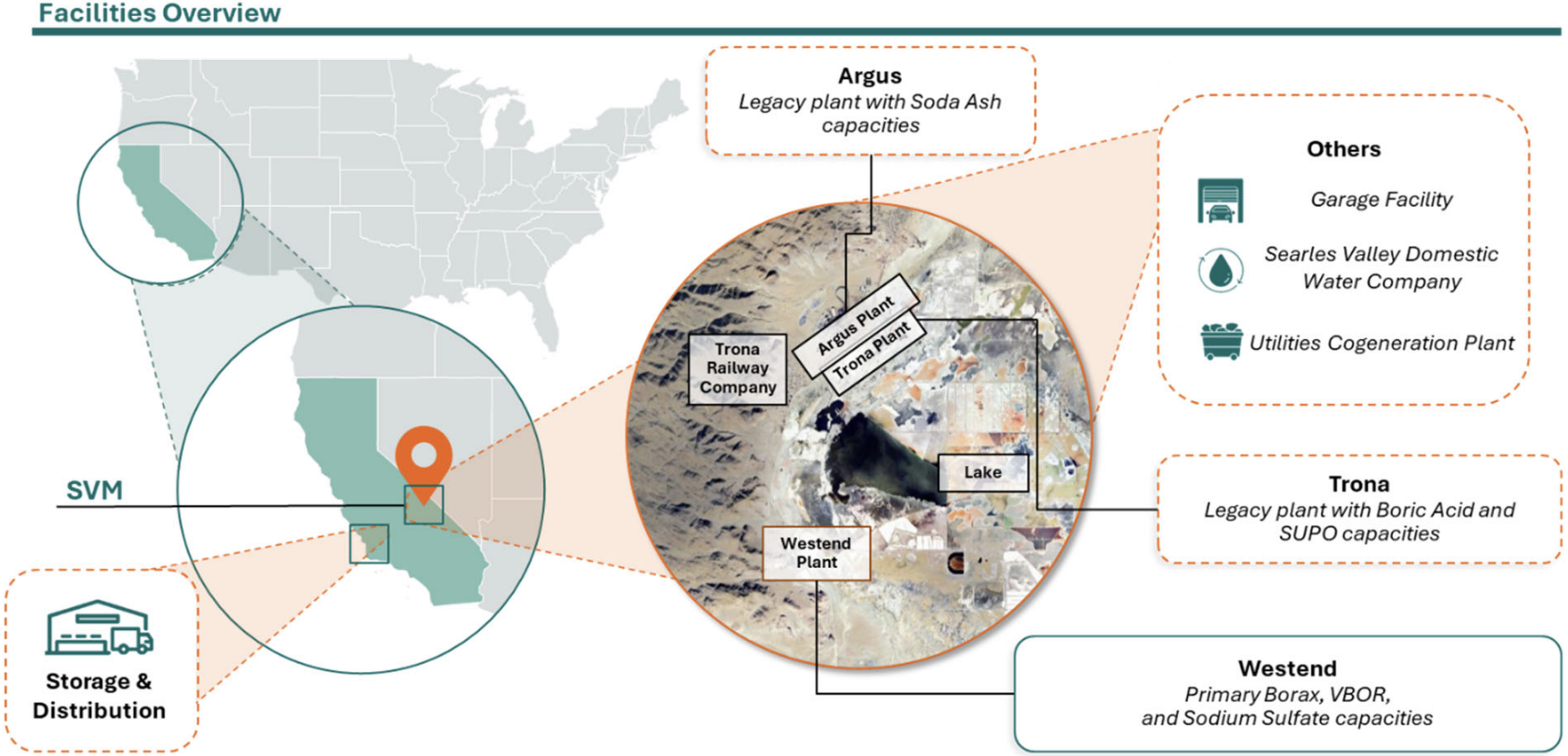

The Company has historically operated three processing plants at Searles Lake: Westend, Argus, and Trona. Activity at the Argus and Trona facilities is currently mothballed, but the Company continues to conduct mining and processing operations at its Westend facility.

- Westend - At Westend, unrefined Primary Borax is extracted from both fresh lake brine and carbonated brine from the Argus SAC plant. Primary and secondary recovery borax from the upstream borax plant is dissolved and recrystallized, converting it from borax decahydrate to the pentahydrate form (“V-BOR”). Historically, the Westend plant had high Primary Borax and V-BOR production rates. However, Primary Borax production was impacted as a result of the Ridgecrest Earthquakes in 2019, resulting in a drop in brine grade and negatively impacting profitability.

- Argus - Historically, soda ash was produced at the Argus facility. This was accomplished by carbonating lake brine with CO2 to form sodium bicarbonate that would then be crystallized and converted back to sodium carbonate (dense soda ash). The Argus plant also has an additional Soda Ash Consolidation (“SAC”) unit to carbonate brine to be fed to the Westend facility. As discussed in further detail below, soda ash production has declined since 2021 due to a combination of both technical and commercial challenges, and in February 2026 the Company shut down soda ash operations to preserve liquidity.

- Trona - Boric acid (“BAX”) is produced at the Trona plant by reacting the Primary Borax produced at Westend with sulfuric acid. Historically, BAX was produced at the Trona plant using borax extracted via the liquid-liquid extraction (“LLX”) unit, but in 2024 the Company mothballed the LLX plant due to high chemicals and utilities costs that resulted in poor production economics.

- Utilities Plant — The Company's facilities also include a coal-fired cogeneration plant that supplies approximately 85–90% of the electrical and thermal energy consumed across the entire mining and processing complex.

Railway & Logistics

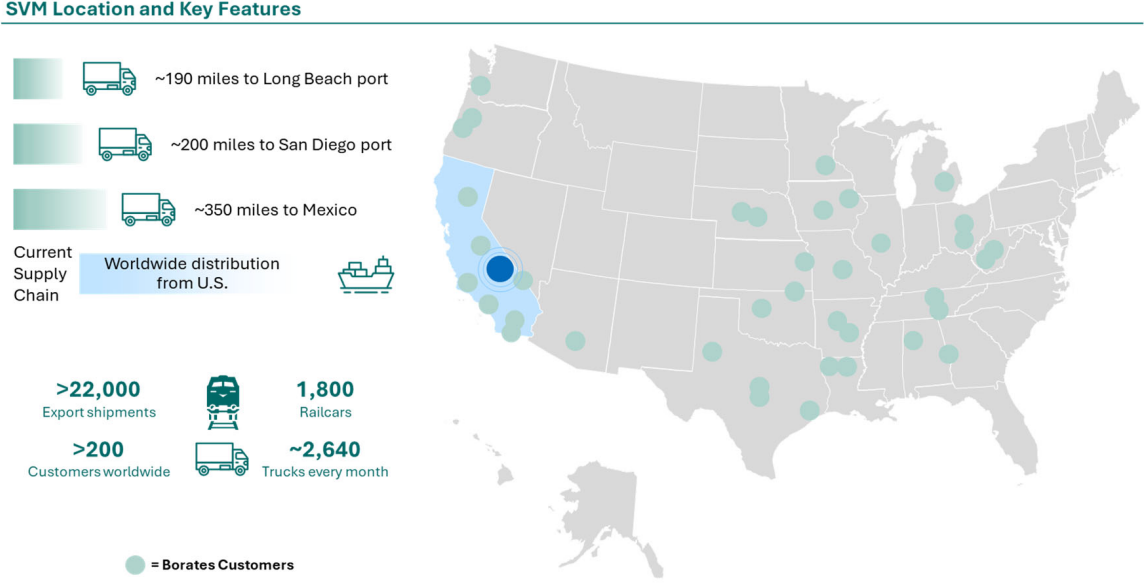

Debtor TRC owns and operates a private short-line railway (the "TRC Railway") connecting SVM's Searles Lake facilities to the Union Pacific main line, serving as the primary logistics backbone for product distribution across North America. The railway has capacity to transport the entirety of the Company's production output — approximately 1.8 million tons per year — using a fleet of approximately 1,600 leased railcars. Historically, the Company maintained dedicated storage and distribution capabilities at two port facilities: Long Beach, accessible via a transloader into the BNSF Railroad, and San Diego, accessible via the TRC Railway and Union Pacific main line. In February 2026, concurrent with the mothballing of soda ash operations and the accompanying workforce reduction, the Company halted its use of the San Diego Port, effectively reducing its active port footprint to Long Beach.

Land Leases & Water Sourcing

- BLM Leases - A significant portion of the land underlying SVM's mining and processing operations is federally owned and leased from the United States Department of the Interior's Bureau of Land Management ("BLM"). Under the terms of the BLM lease, the Company pays a production royalty calculated as a percentage of net sales.

- Water Sourcing and Supply - SVM sources water through five wells and two 30-mile pipelines in the Searles Lake area, consuming approximately 90% of that water in its own mining operations and selling the remaining 10% to SDWC. SDWC, regulated by the California Public Utilities Commission, distributes that water as potable drinking water to approximately 760 residential and commercial customers along the west shoreline of Searles Lake, including the town of Trona. Notably, SVM's water rights are currently in dispute — the Company is a party to pending state court litigation in California's Superior Court to determine rights to the Indian Wells Valley Basin, its sole source of water, and has sought bankruptcy court relief to continue prosecuting those claims without interruption.

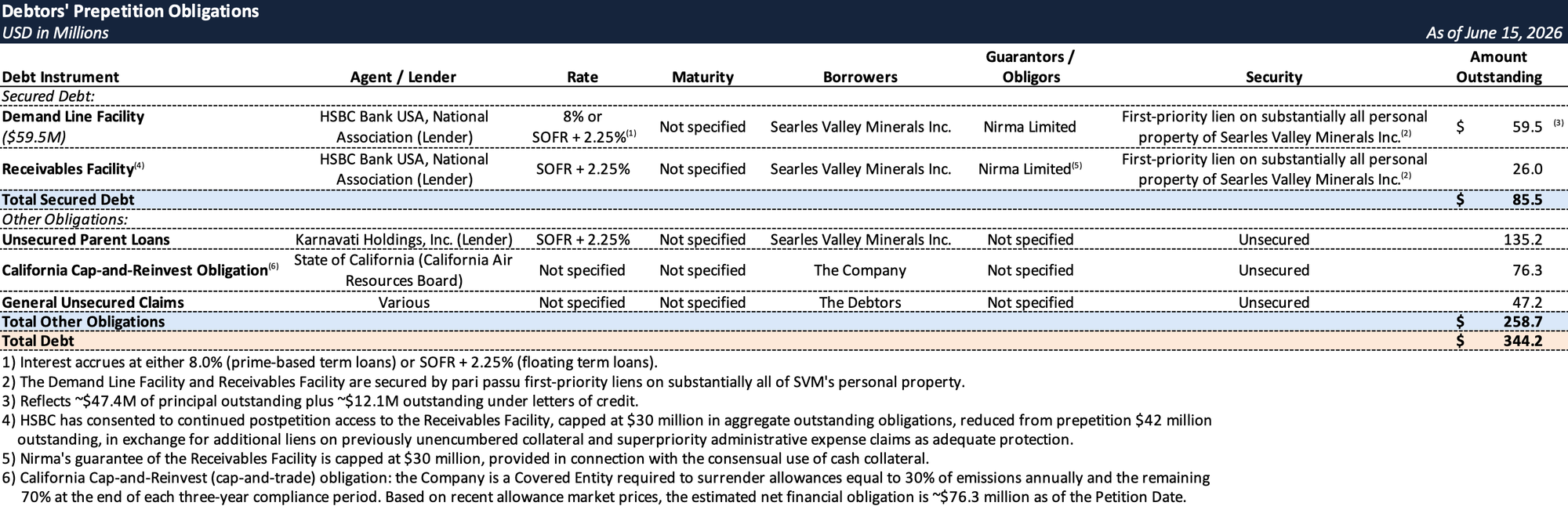

Prepetition Obligations

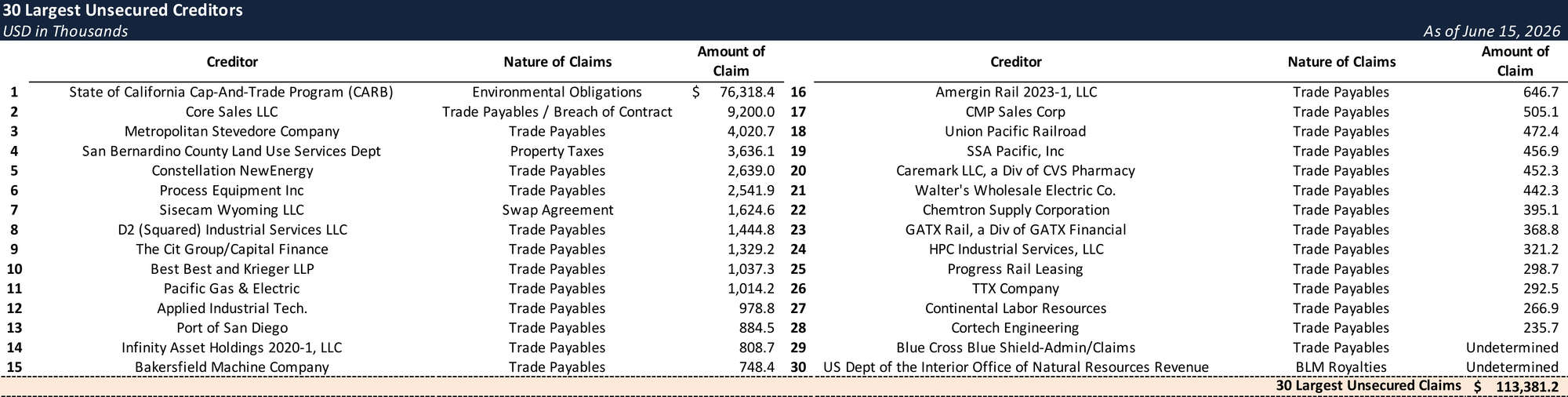

Top Unsecured Claims

Events Leading to Bankruptcy

The Company faced a series of escalating challenges in recent years, marked by substantial capital expenditure requirements, rising production costs, and a structural decline in demand for soda ash — historically its largest source of revenue. Despite undertaking measures at various junctures to address these pressures, the Company was unable to arrest its deteriorating financial position, with mounting operating losses and a liquidity shortfall ultimately leaving it with no viable alternative but to commence these Chapter 11 Cases to preserve the value of its business.

Ridgecrest Earthquakes

The Ridgecrest Earthquakes — two consecutive seismic events on July 4th and 5th, 2019 — struck approximately 25 miles from the Searles Lake complex and caused significant above-ground and subsurface damage to SVM's extraction operations and the lake. The facilities were offline for approximately two months, during which the absence of heat injection caused the lake to cool and brine concentration levels to decline, with lasting effects on production output. As of the Petition Date, extraction operations remain at approximately 50% of pre-earthquake capacity. The Company incurred approximately $50 million in losses from repairs and lost revenue during the recovery period, with EBITDA declining from approximately $52 million in fiscal year 2019 to just $2 million in fiscal year 2020.

Industry Headwinds

The global soda ash market has experienced significant volatility in recent years, driven by worldwide oversupply — predominantly from lower-cost Chinese synthetic soda ash producers — sluggish downstream demand in key sectors including construction and glassmaking, and rising production costs attributable to heightened environmental regulation. These headwinds weighed heavily on SVM's soda ash operations, with net sales declining from approximately $223 million in fiscal year 2023 to approximately $147 million in fiscal year 2026. The Company's financial performance deteriorated as a result, posting losses of $18 million, $24 million, $27 million, and $71 million in fiscal years 2023, 2024, 2025, and 2026, respectively.

By early 2026, with monthly operating losses exceeding $5 million and liquidity continuing to deteriorate, the Company elected to temporarily shut down its soda ash operations. In connection with its mothballing of soda ash production, the Company implemented a corresponding reduction in force, laying off 240 employees and independent contractors (approximately 46 percent of its prior workforce).

Strategic Alternatives and Sale Process

Facing deteriorating market conditions and the lingering operational impact of the Ridgecrest Earthquakes, the Company explored strategic alternatives including a transformation plan to shift focus from soda ash to higher-margin borate production and potential expansion into other markets. Implementation, however, would have required substantial capital expenditures the Company was not positioned to fund. In February 2024, SVM and KHI engaged Lazard as investment banker to evaluate a potential sale transaction. A formal marketing process launched in August 2025 reached over 140 parties, with 50 executing NDAs. By April 2026, it became clear that an out-of-court transaction was not viable, as prospective buyers were unwilling to acquire the business outside a court-supervised process given the Company's legacy liabilities. Lazard subsequently pivoted discussions with several buyers toward a potential in-court §363 sale process.

Independent Committee

On May 26, 2026, SVM appointed John S. Dubel as an independent director, delegating to him authority to review, negotiate, and approve related-party transactions between the Company and its shareholder and sponsor, KHI and Nirma, as well as to review historical transactions between the Debtors and their affiliates. Notably, three current members of the SVM Board — Matthew Dowd, Kaushik Patel, and Avinash Puri — also serve on the board of directors of KHI. On June 12, 2026, the Board established a special independent committee comprised solely of Mr. Dubel, granting it exclusive authority over transactions between KHI and the Debtors.

Supply and Liquidity Agreement

In connection with its exploration of a §363 sale process, the Company — with the assistance of Lazard and Ankura — analyzed its liquidity needs and canvassed the market for financing sources to fund an in-court sale process. Lazard contacted 37 parties to gauge interest in providing such financing, while Nirma and the Company's advisors concurrently engaged with soda ash suppliers to capture liquidity from existing soda ash contracts.

On June 14, 2026, the Company entered into a Soda Ash Supply Agreement and Liquidity Arrangement with TATA Chemicals North America Inc. ("TATA"), under which TATA will provide the Debtors with $20 million in unsecured, interest-free liquidity advances and assume fulfillment of the Company's soda ash supply obligations to its end users. In exchange, TATA will receive payments based on an agreed price per metric ton of soda ash and superpriority administrative expense claims. The Debtors' obligations under the agreement are guaranteed by Nirma, which in turn will receive non-priming postpetition liens and superpriority administrative expense claims on account of its contingent reimbursement claims against SVM, subject to Court approval. Funding is structured in two tranches — $7 million available on an interim basis and the remaining $13 million upon final Court approval.

Chapter 11 Filing

DIP Financing and Liquidity

The Company enters Chapter 11 with a layered liquidity structure assembled from three sources: a parent-provided DIP facility, a supplier-based liquidity advance, and continued access to its prepetition receivables facility.

- Parent Junior DIP Facility - KHI, SVM's immediate parent, provides a $20.0 million committed term loan structured as a junior, non-priming facility — $7.0 million on the interim order and $13.0 million upon final approval — maturing December 1, 2026. The economics are light for the risk: 11% per annum, entirely payable-in-kind, with a 1.0% PIK-eligible commitment fee. KHI receives a first-priority lien on previously unencumbered collateral (primarily real property) under §364(c)(2), with no roll-up of prepetition debt. One structurally notable feature sits outside the conventional DIP construct: SVM is obligated to deliver 3,300 metric tons of V-BOR to Nirma — KHI's ultimate parent and designee — over the course of the case in partial satisfaction of Nirma's prepetition advances, with delivery rights deemed fully earned upon entry of each court order. The facility carries standard operational controls — rolling two-week variance testing, 20% permitted variances, and a Delaware-standard carve-out — and was independently reviewed and approved by the Debtors' single-member Independent Committee given KHI's affiliate status.

- TATA Supply and Liquidity Agreement - Under a June 14, 2026 Supply and Liquidity Agreement, TATA fulfills those customer obligations while advancing up to $20.0 million in unsecured, interest-free liquidity ($7.0 million interim, $13.0 million final). Repayment is embedded in the purchase price SVM pays TATA for soda ash supplied on a dollar-for-dollar basis, making the net cost of the facility largely neutral to the Debtors. TATA takes no liens; its protection is a §364(c)(1) superpriority claim junior to HSBC, KHI, and Nirma. Key commercial terms — pricing per metric ton and customer volumes — are filed under seal. As a condition to providing that guarantee, Nirma required the Debtors to enter into a Reimbursement Agreement obligating SVM to reimburse Nirma for 100% of any amounts paid under the guarantee within 15 days of written demand, with unpaid amounts accruing interest at 11% per annum thereafter. As security, the Debtors granted Nirma non-priming postpetition liens on all DIP collateral and a superpriority administrative expense claim ranked pari passu with the KHI DIP — effectively installing the sponsor at DIP-level priority on a contingent basis, with recourse ahead of general unsecured creditors if the reimbursement obligation goes unpaid.

- HSBC Cash Collateral and Receivables Facility - HSBC, as Prepetition Secured Lender, has consented to the Debtors' continued use of cash collateral and ongoing access to the Receivables Facility postpetition — capped at $30 million in aggregate outstanding obligations, reduced from the prepetition limit of $42 million. The Receivables Facility provides critical working capital by allowing the Debtors to monetize future receivables on their soda ash and borate sales, and without it the Debtors estimate they would require approximately $28 million in additional incremental financing. In exchange for this continued access, the Debtors have granted HSBC additional liens on previously unencumbered collateral and superpriority administrative expense claims as adequate protection. Nirma's guarantee of the Receivables Facility — up to $30 million — was a material condition to HSBC's consent, and to the extent Nirma is called upon under that guarantee, it is subrogated to HSBC's liens and claims against the estate.

Bidding Procedures

The Debtors filed their Bidding Procedures and Sale Motion on the Petition Date, seeking approval of auction procedures, authority to designate one or more stalking horse bidders, assumption and assignment procedures, and ultimately a Sale Order transferring substantially all assets free and clear of liens, claims, and encumbrances under §363(f). The Debtors entered Chapter 11 without a stalking horse under contract, electing to commence the case once financing and cash collateral were secured rather than wait for a contracted price floor.

The Debtors are marketing substantially all assets as a going concern — the interdependent Searles Lake mining complex, three processing facilities (Westend currently operating; Argus and Trona mothballed), the captive coal-fired Utilities plant, the Trona Railway, the SDWC water utility, and all related leases and contracts. The integrated nature of the asset base means the system is most valuable as a whole, though the Bidding Procedures expressly permit sub-auctions, allowing the Debtors to lot the assets into separate groupings if doing so maximizes value.

Qualified bids must be irrevocable, all-cash, non-contingent, and as-is, backed by a 10% good faith deposit with overbids in $1 million increments. Stalking horse bid protections — break-up fee plus expense reimbursement — are capped in the aggregate at 3% of the cash purchase price, with no insider, affiliate, or credit-bidding party eligible. HSBC and KHI are each deemed Qualified Bidders with full credit bid rights, with sale proceeds running first to HSBC and then to KHI.

Key Dates / Timeline

- July 6, 2026 — Bidding Procedures Order

- July 10, 2026 — Final DIP / Cash Collateral Order; Non-Binding LOI Deadline

- August 6, 2026 — Bid Deadline

- August 13, 2026 — Auction

- August 20, 2026 — Sale Hearing

- September 10, 2026 — Sale Closing

- October 19, 2026 — Plan Effective Date

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.