Case Summary: SiFi Networks America Chapter 11

SiFi Networks America filed for Chapter 11 after its UK parent cut funding and moved to appoint administrators amid a ~$17.5M Generate arbitration award it cannot satisfy, pursuing a fast-track §363 sale of its asset-light FiberCity project-management arm via an insider credit bid from ArcLink.

Business Description

Headquartered in Wilmington, DE, SiFi Networks America, LLC (the "Company" or the "Debtor") is a specialized telecommunications infrastructure project management and deployment services provider that is the United States-based subsidiary of SiFi Networks America Ltd. ("SNA Ltd." or "Parent," and together with its affiliates and the Debtor, "SiFi"), a United Kingdom private limited company.

SiFi is an open-access developer, operator, and wholesaler of fiber-to-the-premises ("FTTP") networks in California and the Midwest region of the United States. SiFi constructs citywide open-access networks under its FiberCity® brand (the "Networks") through long-term access agreements to municipal public rights-of-way for the private finance, construction, operation, and maintenance of citywide FTTP Networks. The Networks are then leased to internet service providers, creating an expedited route to mass-market expansion without the associated capital cost of entry. The Networks are constructed in urban and suburban communities of approximately 20,000 to 75,000 homes that generally lack comparable high-speed service offerings and are typically served by a single telephone company and cable company.

SiFi Networks America, LLC filed for Chapter 11 protection on June 5, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the District of Delaware, reporting $1 million to $10 million in assets and $10 million to $50 million in liabilities.

Corporate History

SiFi was founded in 2013 by entrepreneur Roland Pickstock and telecom and sport entrepreneur Mike Harris. The Company spent its early years securing citywide right-of-way and development agreements — and, in some cities, winning competitive municipal RFPs — for its privately funded FiberCity networks across California, the Northeast and the Midwest.

Institutional Capital Backing

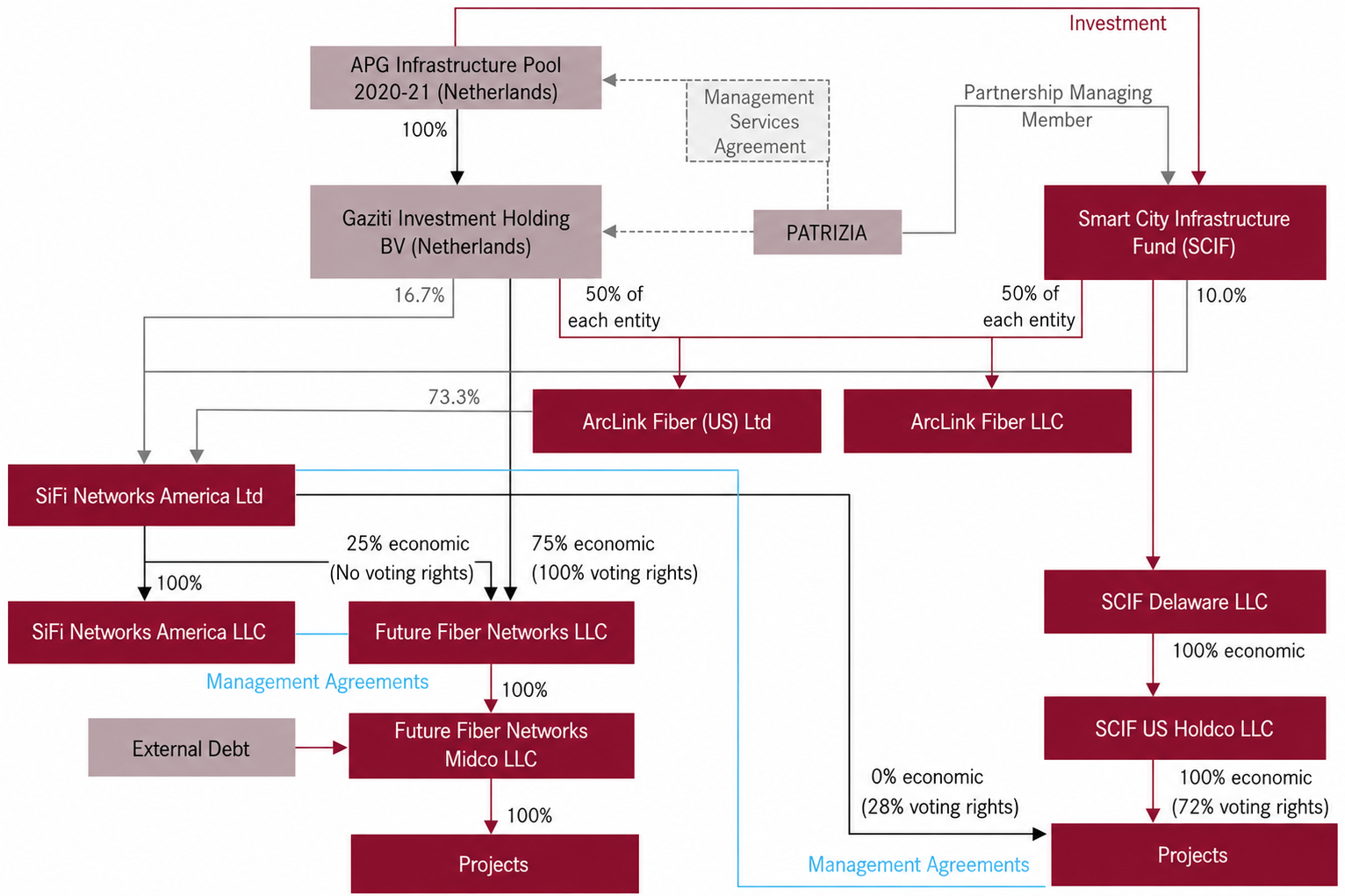

A distinctive feature of the platform is its reliance on European-style infrastructure sponsor capital — equity committed by APG, the Dutch pension asset manager for ABP (Europe's largest pension fund), through a European-domiciled fund manager that has evolved over time: Whitehelm Capital, which originated the SCIF mandate, was acquired by PATRIZIA in February 2022 and rebranded as PATRIZIA Infrastructure, with PATRIZIA assuming management of SCIF and the existing SiFi investment relationship.

In November 2018, APG anchored the Smart City Infrastructure Fund ("SCIF") with €250 million through Whitehelm Capital. SCIF deployed its inaugural investment in April 2019, committing over $75 million into SiFi's Fullerton network, before following with an additional $50 million injection into SiFi in May 2020.

In September 2021, APG announced a $500 million equity commitment to the APG/SiFi joint venture and a 16.7% direct stake in SiFi at the parent level to roll out open-access fiber-to-the-home (“FTTH”) networks in the US. On June 28, 2023, the joint-venture vehicle between APG and SiFi parent — Future Fiber Networks LLC — raised $350 million of seven-year debt.

In April 2026, APG and PATRIZIA converted their longstanding investor relationship into outright ownership, acquiring SiFi Networks America Ltd. from its founders, Mike Harris and Roland Pickstock, for undisclosed consideration.

Equity Ownership

100% of the Debtor's membership interests are held by SiFi Networks America Ltd. ("SNA Ltd."), a UK-based entity. Ownership runs upstream through Netherlands-domiciled holding vehicles tied to APG and PATRIZIA, which together control SCIF, Future Fiber Networks LLC, and the ArcLink Fiber entities. As a result, the Debtor's prepetition secured lender, DIP lender, and stalking horse purchaser — ArcLink — sits within the same sponsor group that ultimately controls the Debtor's equity.

Organizational Structure

Operations Overview

SiFi operates through what it calls an open-access three-layer model: a management/infrastructure company that builds and owns the fiber in the ground (the investor-owned, non-recourse Project Companies, with the Debtor acting as project/program manager), an operating company that manages the active electronics on the network, and unaffiliated third-party ISPs that deliver retail services to customers over the open-access network.

Investor and Funding Structure

SiFi has secured approximately $1 billion in institutional capital commitments to date, funded through non-recourse, special purpose vehicles or "City LLCs" (the "Project Companies") that are owned by the investors themselves — primarily through Future Fiber Networks LLC and SCIF. The Debtor secures contracts and analysis in readiness to present to the investors for approval. If approved, the investor forms the Project Company and provides the equity required to build a Network.

The Debtor's Role

The Debtor originates contracts with municipalities and local governments, which it operationally executes through its U.S.-based employees, comprising approximately thirty-three (33) individuals — project managers, coordinators, and operational leadership personnel. The Debtor primarily supports fiber network deployment initiatives within SiFi's business through network deployment planning, tracking permitting processes, jurisdictional coordination, vendor and subcontractor management, construction management, program management, delivery coordination, stakeholder reporting, and compliance support. As a result, the Debtor has developed substantial expertise in managing complex, multi-phase telecommunications infrastructure development projects.

The Debtor generates approximately $10 million in annualized revenue, primarily through management fees that are earned for developing and managing the Networks. Management fees are fixed, with some variability based on targets, and paid monthly by the Project Companies based on the size of the applicable project. Due to increased resources and complexity, management fees are higher during construction than during operations. The Debtor also has the potential to earn development fees, subject to meeting key milestones, which are paid at a rate of two percent (2%) of CapEx.

Network Portfolio

The Debtor, in conjunction with its Parent, provides project management services for nine (9) active Networks:

- Two (2) that are complete in Placentia, CA and Kenosha, WI;

- Five (5) that are operational but still under construction in Farmington, MI; Rockford, IL; Simi Valley, CA; Oceanside, CA; and Palmdale, CA;

- One (1) under construction in Fullerton, CA; and

- One (1) due to become operational shortly in Escondido, CA.

SiFi previously developed projects in East Hartford, CT and Saratoga Springs, NY that were abandoned, and a project in Rancho Cordova, CA that currently is suspended.

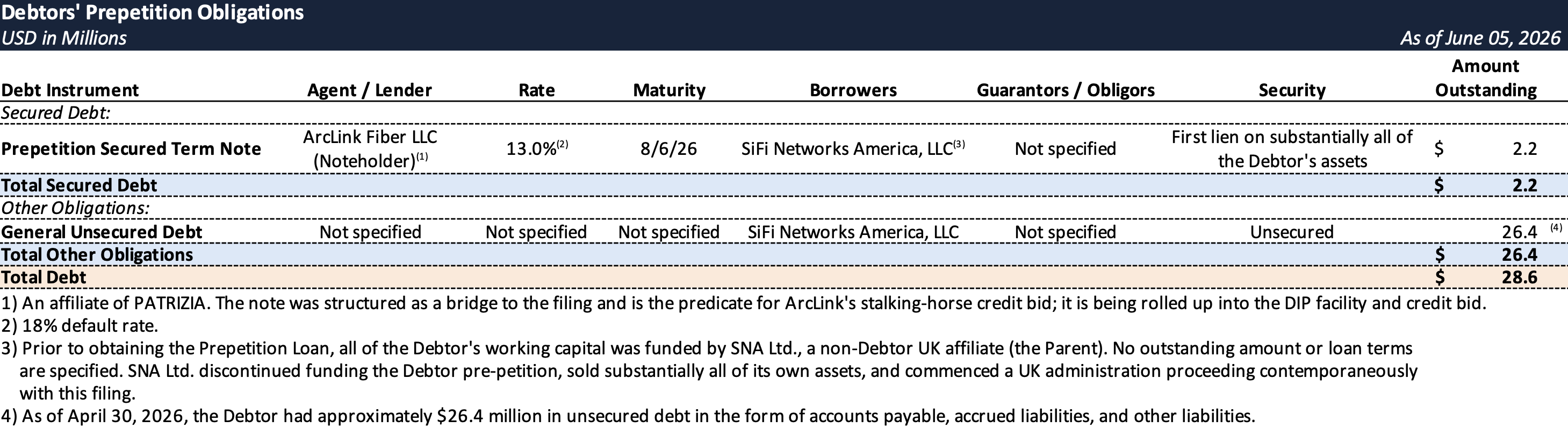

Prepetition Obligations

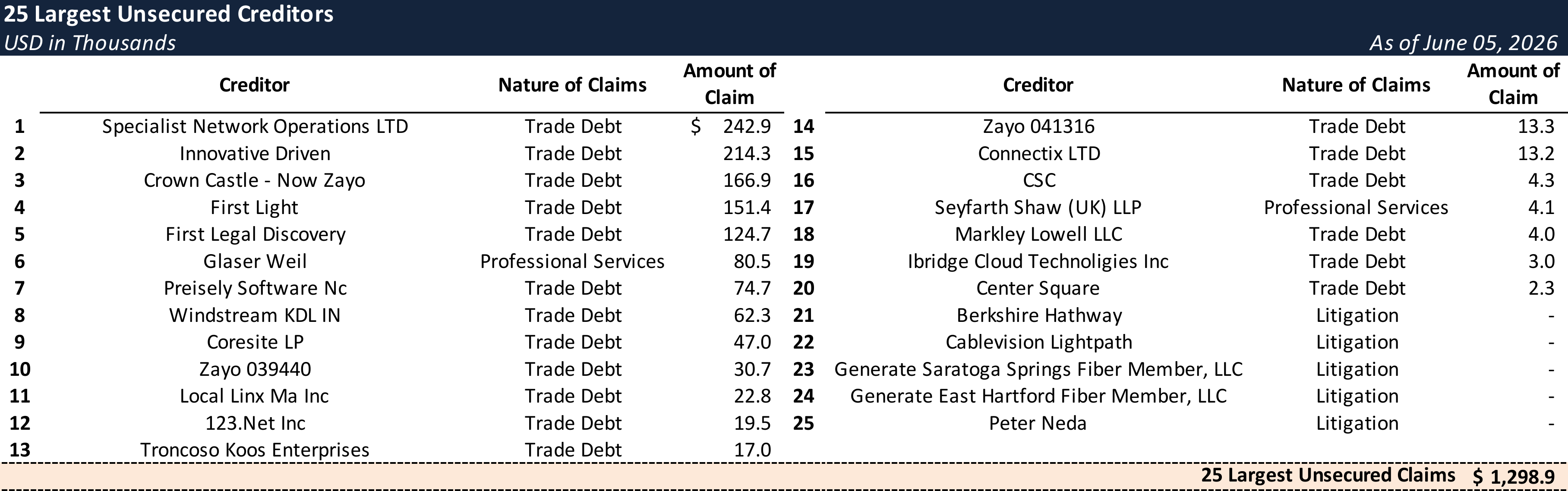

Top Unsecured Claims

Events Leading to Bankruptcy

SiFi's bankruptcy is the product of a cascade of execution, litigation and capital-structure failures layered onto a model with high upfront CapEx, a thin operating cushion at the Debtor level, and a substantial litigation tail. The First Day Declaration frames the filing as the convergence of three interlocking causes: the UK parent discontinuing funding, selling substantially all of its own assets and commencing a UK insolvency process; adverse litigation results coupled with an inability to keep paying professional advisors; and vendors and servicers threatening legal action and/or to stop doing business with the Debtor. The arithmetic underneath is stark: roughly $26.4 million of known unsecured obligations against approximately $206,000 of cash and roughly $10 million of annualized fee revenue left the Debtor with too little liquidity, collateral or direct asset ownership to absorb the shock once parent funding ceased.

Litigation

The Debtor faces four active litigation matters that collectively contributed to its decision to seek Chapter 11 protection.

- Generate Litigation — In December 2023, Generate Saratoga Springs Fiber Member, LLC and Generate East Hartford Fiber Member, LLC (collectively, "Generate") filed a complaint against the Debtor, SNA Ltd., and certain of their affiliates in the Court of Chancery of the State of Delaware, seeking specific performance with respect to certain agreements relating to fiber optic networks in Saratoga Springs, NY and East Hartford, CT. The matter was subsequently moved to arbitration before the American Arbitration Association/International Centre for Dispute Resolution, which issued a Partial Final Award on January 22, 2026 and a Second Partial Final Award on May 1, 2026, finding the Debtor jointly and severally liable to Generate in the amount of approximately $16.3 million, plus attorneys' fees of approximately $1.2 million — bringing the total exposure to approximately $17.5 million. On April 27, 2026, the defendants filed a motion for summary judgment with the Delaware Chancery Court seeking to vacate the Partial Final Award. According to the First Day Declaration, the Debtor has no ability to satisfy the ultimate $17.5 million judgment.

- Neda Litigation — On January 21, 2025, Peter Neda, the Debtor's former general counsel, filed a complaint against the Debtor and SNA Ltd. in the Superior Court of the State of California alleging, among other things, breach of contract. The parties are currently engaged in discovery.

- Cablevision Lightpath Litigation — On May 6, 2026, Cablevision Lightpath LLC filed a complaint against the Debtor in the Superior Court for the State of Delaware alleging, among other things, breach of contract. As of the Petition Date, the Debtor had not been served with the complaint.

- Berkshire Hathaway Litigation — Berkshire Hathaway Specialty Insurance Company filed a lawsuit against the Debtor as a third-party defendant in the United States District Court for the Central District of California, alleging breach of a National Multi-City Agreement entered into between Corbel Communications Industries LLC ("Corbel") and the Debtor in 2018, which granted Corbel a right of first refusal with respect to certain microtrenching projects. A jury trial is scheduled to commence on August 25, 2026.

Parent Funding Withdrawal & UK Insolvency

Prior to the Petition Date, the Debtor was entirely dependent on SNA Ltd. for its working capital — a dependency that proved fatal when SNA Ltd. abruptly discontinued funding, moved to sell substantially all of its own assets, and commenced its own insolvency proceeding in the United Kingdom, leaving the Debtor without a source of operating liquidity. With no third-party financing available, the Debtor was forced to turn to ArcLink — its own sponsor affiliate — for a $2.2 million emergency loan on May 6, 2026, a stopgap measure that provided only temporary relief given the Note's August 6, 2026 maturity and the Debtor's inability to satisfy the underlying obligations.

The collapse of the parent relationship required the Debtor to closely coordinate its Chapter 11 filing with the commencement of SNA Ltd.'s UK administration proceeding. To preserve operational continuity across the two concurrent insolvency proceedings, the Debtor and SNA Ltd. entered into a prepetition Master Services Agreement governing the ongoing provision of services to one another. SNA Ltd. filed a notice of intention to appoint administrators on June 4, 2026 — one day before the Petition Date — with its asset sale closing on the same day the Debtor sought Chapter 11 protection, effectively stripping the Debtor of its parent at the same moment it entered bankruptcy.

Decision to Restructure

Given the foregoing, SNA Ltd. came to the inevitable conclusion that a restructuring of the Debtor's business would be necessary. On April 22, 2026, SNA Ltd. appointed Michael Wyse of Wyse Advisors, LLC as the sole independent Manager of the Debtor to assess its financial position and develop a comprehensive restructuring plan. Following his appointment, the Debtor retained Cole Schotz P.C. as legal counsel, KCP Advisory Group LLC as financial advisor, and Sherwood Partners, Inc. as sales agent to assist with the Debtor's overall restructuring strategy and contingency planning.

DIP Financing

SiFi filed as a liquidating Chapter 11 built around a single counterparty wearing three hats — ArcLink Fiber LLC, a PATRIZIA affiliate, serves simultaneously as the Debtor's prepetition secured lender, DIP lender, and stalking-horse buyer, and is an admitted statutory insider.

- Structure: Senior secured, superpriority, delayed-draw term loan consisting of (i) $3.13 million in new money — approximately $1.1 million at interim and $2.0 million at final — and (ii) a cashless roll-up of the Prepetition Secured Note of approximately $2.22 million, bringing the aggregate facility to approximately $5.35 million. The Interim Roll-Up of $1.1 million equals the interim new money draw dollar-for-dollar, representing approximately 51% of the prepetition note rolled at the interim stage.

- Pricing and Maturity: 10% PIK; 120-day maturity; no funding fees.

- Collateral: First priority, superpriority lien on substantially all of the Debtor's assets, extending to the proceeds of Chapter 5 avoidance actions upon entry of the Final Order.

- Lien Stipulation and Challenge: The Debtor stipulates to the validity of the prepetition liens, subject to a challenge window capped at the earlier of one business day before the sale hearing or 75 days, supported by only a $25,000 investigation budget.

- Waivers: 506(c), 552(b), and marshaling waivers, each effective upon the Final Order.

- Lender Protections: Any suit by or on behalf of the Debtor or a creditors' committee that would subordinate ArcLink's claim or lien constitutes an event of default. The DIP Lender must consent to any proposed sale, and designation of any buyer other than ArcLink as the successful bidder is a termination event.

- Marketing Process: Sherwood Partners solicited ten alternative DIP lenders prepetition. Because ArcLink refused to be primed, competing lenders could only be offered junior paper — seven declined outright, one declined after conducting diligence, and two never responded. No third party was willing to lend on the junior or unsecured basis available, leaving ArcLink as the sole source of postpetition liquidity.

Sale Process

The stalking horse bidder is ArcLink, and the stalking horse purchase price is a credit bid of approximately $4.6 million — consisting of the full amount of approximately $2.2 million outstanding under the Prepetition Secured Note plus all or a portion of the DIP Obligations — with the only cash component being cure payments on assumed contracts. The Purchased Assets include substantially all of the Debtor's assets, most notably all avoidance actions and Chapter 5 causes of action, expressly including claims against the Debtor's own equityholders, officers, managers, and directors. Assumed liabilities are narrow; excluded liabilities are sweeping — leaving the $17.5 million Generate arbitration award, the Berkshire, Lightpath, and Neda litigation, and all administrative and professional fee obligations with the estate. Bid protections consist of a $200,000 expense reimbursement and a 3% break-up fee.

Any competing bidder must pay the entire ArcLink stack — the DIP roll-up and prepetition debt — in full in cash at closing, plus the $200,000 expense reimbursement, the Estate Funding Commitment, and a minimum overbid increment of $250,000. This requirement effectively limits the competitive field to parties with significant liquidity and no ability to credit bid, leaving ArcLink in a structurally advantaged position.

The case runs on an eight-week clock driven by DIP milestones:

- July 2, 2026 — Deadline to file and serve Sale Notice and Assumption Notice

- July 14, 2026 — Bid Deadline

- July 17, 2026 — Auction (if qualified bids received), 10:00 a.m. ET at Cole Schotz

- July 29, 2026 — Sale Hearing (Sale Order due within 54 days of filing)

- July 31, 2026 — Closing / outside date

Absent a full-cash overbid, ArcLink takes substantially all of the Debtor's assets — including the estate's avoidance actions and insider claims — by credit bid, while the litigation tail, cash, and corporate shell remain behind with the estate. Whether a creditors' committee is appointed in time to fight for a carve-out of the D&O claims and associated tail policy proceeds is the most consequential open question in the case.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.