Case Summary: SIMAD Holdings Chapter 11

SIMAD Holdings filed Chapter 11 to pursue an expedited financing or sale of its 30-camp portfolio, after missing a May 31 interest payment on $214M in Tel Aviv bonds following a ~$34M owner transfer under investigation and facing cash seizure by merchant cash advance lenders.

A deck version of this summary is also available HERE.

Business Description

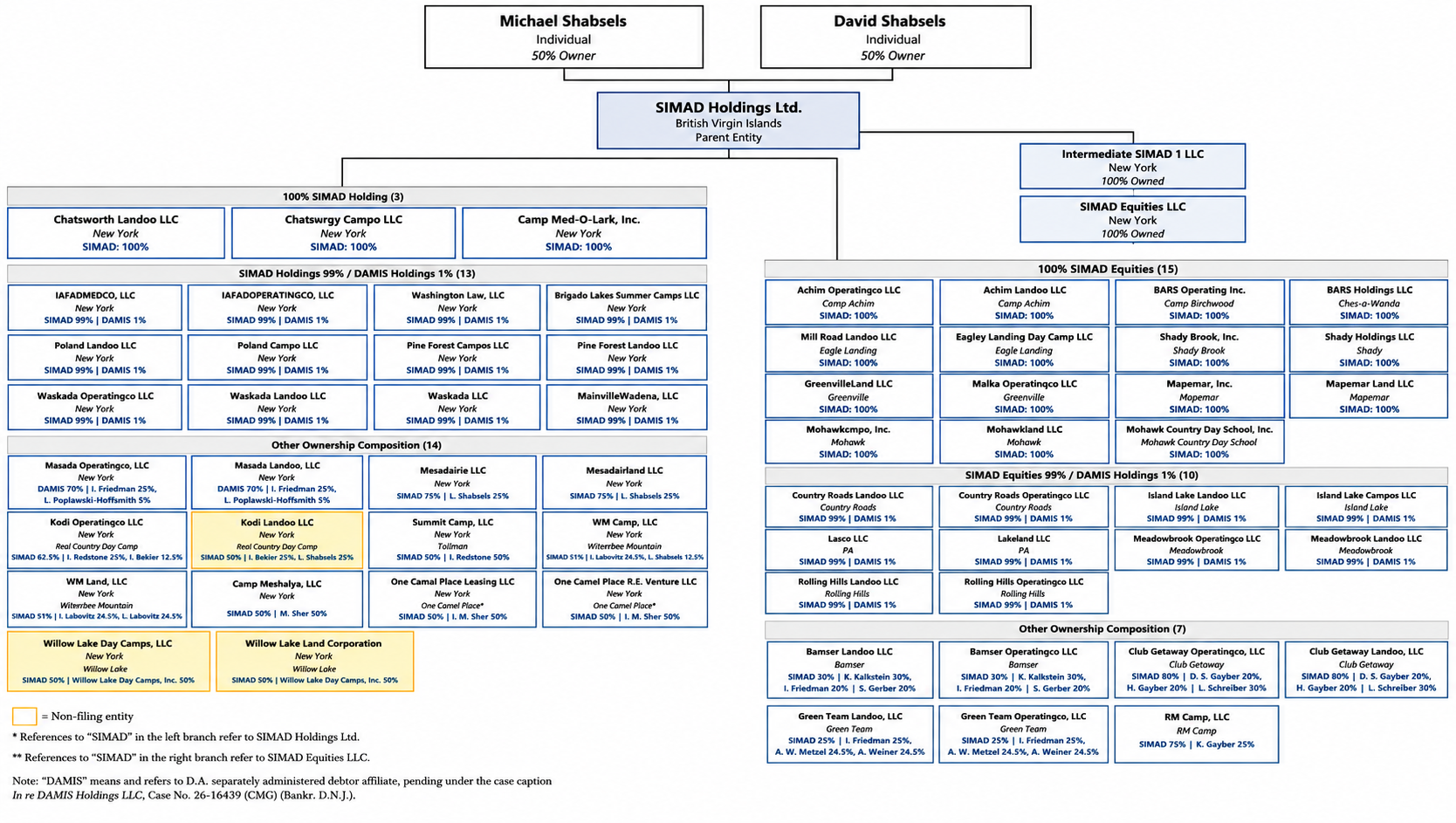

SIMAD Holdings Ltd., a British Virgin Islands holding company headquartered in Trumbull, CT, together with its Debtor⁽¹⁾ affiliates (collectively, the "SIMAD Debtors"), owns and operates one of the largest privately held for-profit networks of summer camps in the United States.

- The portfolio comprises approximately 30 camps—22 overnight (sleepaway) camps and 8 day camps—concentrated in New York, Pennsylvania, New Jersey, and Maine, and also including Blue Star Camps in North Carolina. One camp, Willow Lake Day Camp, is owned and operated but is not a Chapter 11 debtor and therefore sits outside the estate.

- SIMAD Holdings Ltd. is owned in equal halves by brothers Michael and David Shabsels, New York–based real estate investors who entered the for-profit camp business in 2006. In total, the Shabsels enterprise reportedly comprised roughly 80 real estate assets — the camps plus office, retail, multifamily, and hotel properties across the country, the latter largely held through the separately administered DAMIS group of affiliates (DAMIS Holdings)⁽²⁾.

The camps serve children and teenagers ages 7 to 16 across a diversified mix of programming — residential (sleepaway) and day camps, with individual camps focused on sports, arts, technology, academics, and religion. Many feature Jewish programming or primarily serve Jewish families, though they are for-profit and unaffiliated with any denomination or the Foundation for Jewish Camp, which includes over 300 nonprofit Jewish camps across North America. Approximately 20,500 children enroll each year, as much as 5% of them from outside the United States. Tuition ranges from roughly $8,000–$10,000 per season to more than $17,000 for premium overnight programs.

The SIMAD Debtors' 2025 results reflected steady growth: revenue rose to $165.4 million from $159.4 million in 2024, operating profit increased to $24.3 million from $22.0 million, and consolidated EBITDA (including the SIMAD Debtors' share in associates) climbed to $41.9 million from $37.7 million; SIMAD Holdings Ltd. had reported net profit of $8 million for 2024.

SIMAD Holdings Ltd. and 60 affiliated debtors filed for Chapter 11 protection on June 4 and June 5, 2026 (together, the "Petition Date") in the U.S. Bankruptcy Court for the District of New Jersey, reporting consolidated estimated assets of $100 million to $500 million and liabilities of $500 million to $1 billion.

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

⁽²⁾ A separate but related group—DAMIS Holdings LLC and 89 affiliated debtors—filed the same day (Case No. 26-16439), holding the broader commercial and recreational real-estate portfolio (office and retail buildings, multifamily entities, and recreational assets such as Rocking Horse Ranch and Splashdown Beach). SIMAD and DAMIS share common 50/50 Shabsels ownership and a common Trumbull, CT headquarters but are separately administered, and the SIMAD Debtors represent that their cash "will not flow to DAMIS Holdings LLC ("DAMIS") or any of the DAMIS affiliates"; both brothers also filed personal bankruptcy. Note that the BVI "SIMAD Holdings Ltd." (lead debtor, Case No. 26-16388) is distinct from the U.S. "SIMAD Holdings LLC" inside the DAMIS group.

Corporate History

The Shabsels brothers began acquiring camps in 2006 and, over nearly two decades, assembled one of the country's largest camp networks through a steady roll-up of established, multi-generational institutions. Several portfolio assets long predate the holding-company structure—Pine Forest Camp in Pennsylvania traces its origins to 1931 and bills itself as a continuously family-operated camp, now in its fourth generation of family management, while Camp Wekeela dates to 1922. The brothers generally preserved each camp's legacy brand, local directors, and customer-facing identity rather than rebranding the portfolio under a single corporate name.

The December 2025 Tel Aviv Bond Offering

SIMAD Holdings Ltd., a BVI holding company, is the ultimate parent of the SIMAD camp Debtors and the issuer of the December 2025 secured bond offering on the Tel Aviv Stock Exchange, which served as the financing engine for the roll-up's most recent phase. The company issued Series A debentures with NIS 620 million (approximately $211.6 million) of par value. The camp portfolio was appraised in connection with the offering at $466.6 million, with a projected cap rate of approximately 10.5% for 2025.

- The offering was led by underwriter InFin Capital, headed by Yehonatan Cohen, which received an exceptionally large underwriting commission of NIS 15 million. Of the proceeds, $50 million was earmarked to purchase assets from the controlling shareholders, with a similar amount for early repayment of loans that carried the Shabselses' personal guarantees.

- Thirteen camps that SIMAD Holdings Ltd. was to acquire from its owners were pledged to bondholders: Camp Achim, Chen-A-Wanda, Club Getaway, Country Roads Day Camp, Eagle's Landing, Echo, Green Lane, Malka, Lavi, Meadowbrook, the SHMA Camps, Mohawk Day Camp, and Rolling Hills Day Camp.

Corporate Structure

SIMAD Holdings Ltd. sits at the apex of the group as ultimate parent and lead debtor. Below it, the camp entities are held along two parallel tracks: roughly half owned directly by SIMAD Holdings, and the remainder through a wholly-owned intermediary chain — Intermediate SIMAD 1 LLC to SIMAD Equities LLC, both New York entities — before reaching the operating camps. Ownership at the camp level is more varied. Approximately a third of the underlying entities are wholly owned within the SIMAD group; another third carry a nominal 1% interest held by the affiliated DAMIS group; and the remaining third involve outside minority partners, typically the camps' original founders who retained a stake at the time of sale — the Bellottos at Kiwi and the Herschthals at Blue Star among them.

Camp-level pairing. The standard playbook was to form two entities per camp—a "LandCo" holding the real estate and an "OperatingCo" running operations—typically owning both, with some original camp owners retained as partners (e.g., Pine Forest Campco LLC / Pine Forest Landco LLC; Mohawkcampco LLC / Mohawkland LLC).

Operations Overview

The camps operate seasonally during the summer, on land owned by the debtor subsidiaries, under a decentralized, camp-level management model. The common economic profile is built on prepaid enrollment revenue, heavy seasonal labor and logistics costs, and significant real-estate intensity.

Revenue Model, Seasonality & the Prepaid-Deposit Liability

Beyond tuition, the SIMAD Debtors derive a less-material portion of income from on-campground sales of food and clothing, and generate off-season income by leasing their properties to private events or groups and educational institutions. The prepaid structure that funds the model is also its largest hidden working-capital risk: deposits for a given summer are "due the year prior," while the cost of running one season "alone cost[s] tens of millions."

- That timing makes every prepaid enrollment a pre-petition customer claim and creates refund exposure if any camp fails to open—yet the first-day package contains no customer-programs motion: the debtors did not seek authority to honor camper deposits, issue refunds, or continue customer programs (the consolidated-list motion addresses campers only by redacting the names of enrollees, who are minors). With aggregate general unsecured claims estimated at just ~$2.7 million—far below the value of ~20,500 prepaid enrollments—the deposits appear to be treated as performance obligations to be discharged by running the 2026 season rather than as scheduled cash claims. Families' protection therefore hinges entirely on the camps opening and operating through August; a mid-season funding failure would convert prepaid tuition into unsecured refund claims.

- The New York City Board of Education is reported to be the SIMAD Debtors' largest customer, although no first-day filing quantifies or describes the relationship.

Operations and Workforce

Each camp retains its own management team, accounting functions, staff, and operational infrastructure under a long-standing local brand. These are asset-heavy operations—cabins or rooms, dining halls, a clinic, swimming pools, and extensive sports and arts facilities (Pine Forest alone advertises a 1,000-acre campus); the infrastructure extends to propane, well water, septic systems, and Starlink satellite internet.

- As of the Petition Date, the Debtors' workforce comprises approximately 342 full-time employees (including roughly 30 camp directors) plus approximately 4,300 part-time and seasonal employees at the summer peak, alongside more than 50 independent contractors, with many seasonal staff drawn from abroad through the U.S. J-1 Camp Counselor Exchange Program. Peak-season payroll runs approximately $10.2 million per month and employee benefits roughly $400,000 per month.

Prepetition Obligations

The capital structure above is for informational purposes only. Refer to the First Day Declaration for a full list of borrowers, guarantors and collateral camps. Note that in the Declaration, the Debtors emphasize that the capital structure presented is preliminary and subject to further review and revision, and that inclusion of any indebtedness is not an acknowledgment of the validity of any liens or claims asserted by the identified lenders, with all rights reserved.

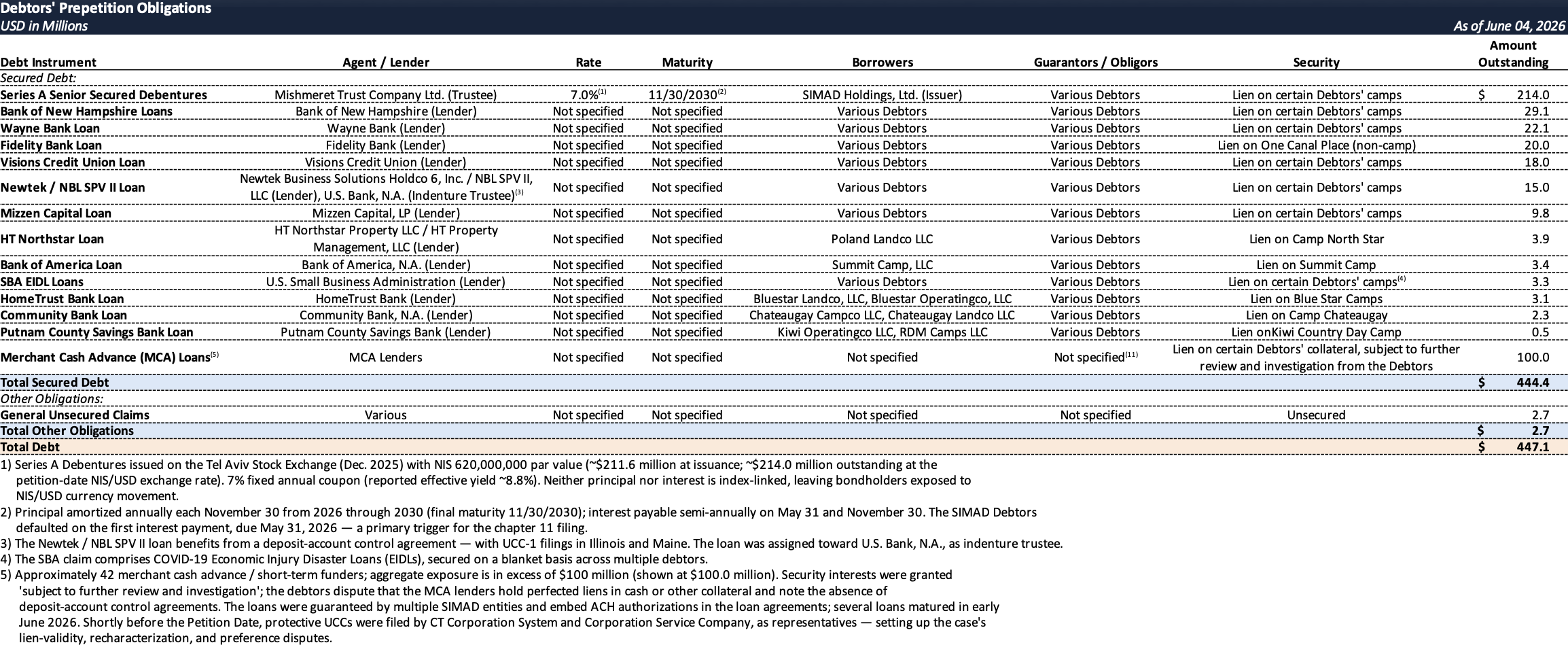

See below for additional lender-by-lender breakdown of the prepetition secured debt stack as disclosed in the Cash Collateral Motion.

- Series A Senior Secured Debentures — Mishmeret Trust (~$214 million) — Raised on the Tel Aviv Stock Exchange in December 2025 at NIS 620 million par, bearing 7% fixed annual interest with principal due annually from 2026 through 2030. The debtors missed the first interest payment on May 31, 2026 — the immediate filing trigger. Collateral spans 35 entities across the majority of the camp portfolio. The interim order was not filed with the petition, leaving collateral terms and adequate protection details unconfirmed.

- Bank of New Hampshire Loans (~$29 million) — Two loans originated in December 2021 ($27 million) and July 2023 ($6 million), secured by mortgages on camp properties, assignments of leases and rents, and security interests in other collateral across a cluster of North Carolina, Maine, and New Hampshire camps including Blue Star, Camp Wekeela, Camp North Star, and Windsor Mountain. Interim order bundled with Mishmeret and also not filed, leaving collateral terms unconfirmed.

- Wayne Bank Loan (~$22 million) — Two structurally distinct loans. The Camp Mesorah loan ($3.7 million, originated 2017) is secured by mortgages across Mesorahland, Meadowbrook Landco, and Shab Holdings, with assignments of rents and UCC-1s in New York and Pennsylvania. The Pine Forest loan (~$18.4 million combined, originated 2022) is secured by open-end mortgages on Pine Forest properties with UCC-1s in Pennsylvania only. Camp Echo appears in the secured creditor table against Wayne Bank but is absent from the interim order — an unexplained gap the forthcoming schedules should clarify. No DACA. Adequate protection: replacement liens plus 507(b) superpriority claim.

- Fidelity Bank Loan (~$20 million) — Collateral is One Canal Place, a commercial real estate asset unrelated to any camp operation. Loan originated March 26, 2026 — weeks before the filing — making it the most recently originated secured debt in the case. Uniquely, the interim order requires the debtors to remit base rent, CAM charges, real estate taxes, and insurance to Fidelity monthly starting July 2026, a more operational adequate protection arrangement than any other lender received. No DACA.

- Visions Credit Union Loan (~$18 million) — Borrower is RDM Camps LLC, secured against Camp Lokanda. No interim cash collateral order was filed, placing Visions alongside Mizzen as a lender whose consent was not obtained and whose lien position remains unresolved at filing.

- Newtek / NBL SPV II Loan (~$15 million) — Originated June 30, 2025. Collateral is defined broadly across inventory, equipment, accounts, deposit accounts, general intangibles, and all proceeds — covering eight operating camp entities with additional landco guarantors. UCC-1s filed in Illinois and Maine on June 15, 2025. The loan was originated by Newtek, assigned to NBL SPV II, and subsequently assigned to U.S. Bank N.A. as indenture trustee, indicating securitization. Crucially, borrowers entered into a deposit account control agreement with Newtek Bank — the only confirmed DACA in the case — giving Newtek perfected cash-control priority no other lender holds. The interim order specifically freezes those deposit account funds pending further court order. Adequate protection: replacement liens only, no superpriority claim.

- Mizzen Capital Loan (~$9.8 million) — Spans a broad cross-section of camp entities including Banner, Pine Forest, Mohawk, Mogen Avraham, Mesorah, and Windsor Mountain. No interim cash collateral order was filed, leaving its lien validity, priority, and claim amount as open disputes.

- HT Northstar Loan (~$3.9 million) — Borrower is Poland Landco LLC, secured against Camp North Star. No interim cash collateral order filed. Collateral terms and adequate protection arrangements unconfirmed from available documents.

- Bank of America Loan (~$3.4 million) — Originated September 2022 against Summit Camp LLC only — the most self-contained collateral structure among the traditional bank lenders. Secured by an open-end mortgage, assignment of rents, and blanket personal property lien, with UCC-1 in Pennsylvania. No cross-guarantees, no multi-camp exposure. Adequate protection: replacement liens plus 507(b) superpriority claim. No DACA.

- SBA EIDL Loans (~$3.25 million) — Twenty-one separate COVID-19 disaster loans made in 2020 to twenty-one individual debtor entities, ranging from $57,157 to $464,678 per entity. Each carries its own promissory note, blanket personal property lien, and UCC-1 filing — making this twenty-one individual perfected liens rather than one consolidated claim. No DACA. Adequate protection: replacement liens plus 507(b) superpriority claim.

- HomeTrust Bank Loan (~$3.1 million) — Originated September 2021 against Blue Star Camps in North Carolina. Security package uses a deed of trust rather than a mortgage — the governing instrument under North Carolina law — plus assignment of rents and blanket personal property lien, with UCC-1 in North Carolina. Enforcement governed by North Carolina deed of trust law, distinct from the New York and Pennsylvania frameworks applicable to most other lenders. No DACA. Adequate protection: replacement liens plus 507(b) superpriority claim.

- Community Bank Loan (~$2.3 million) — Originated June 2022 against Camp Chateaugay only. One lender, one camp, two entities, straightforward mortgage plus blanket personal property lien with UCC-1 in New York — the cleanest and most contained collateral structure in the case. No cross-guarantees, no multi-camp exposure. No DACA. Adequate protection: replacement liens plus 507(b) superpriority claim.

- Putnam County Savings Bank Loan (~$489,000) — The oldest loan in the case, originated August 2013 against Kiwi Country Day Camp. Borrower is Kiwi Operatingco LLC with RDM Camps LLC as guarantor — notably the same RDM Camps entity that is the direct borrower under the Visions Credit Union loan, creating dual exposure. Security package covers personal property of both entities with UCC-1s in New York. No DACA. Adequate protection: replacement liens plus 507(b) superpriority claim.

- MCA Loans (>$100 million, ~42 lenders) — Short-term advances accumulated in the weeks and months before filing. Security interests purportedly granted but explicitly flagged as subject to further review — the debtors affirmatively state they do not believe any MCA lender holds a perfected cash lien through a DACA. Loans are cross-guaranteed across multiple SIMAD entities and embed ACH authorizations giving lenders direct account access, which was a primary liquidity threat driving the timing of the filing. No interim cash collateral orders obtained for any MCA lender. Protective UCC-1s filed by CT Corporation System and Corporation Service Company shortly before the Petition Date set up what will likely become the case's central lien validity, preference, and recharacterization disputes.

Events Leading to Bankruptcy

The SIMAD Debtors did not fail operationally: 2025 posted the highest revenue on the company's brief public record, with revenue, operating profit and EBITDA all up year-over-year. What forced the filing was a governance rupture at the BVI parent, a defaulted Tel Aviv bond, and a wall of short-term merchant-cash-advance debt that could have seized the season's cash on a single creditor's command.

The $34 Million Transfer and Bond Default

The proximate trigger was a late-May 2026 disclosure. In reviewing its first-quarter financial statements, SIMAD Holdings Ltd. disclosed to the Tel Aviv Stock Exchange that almost $34 million (approximately NIS 100 million) had been transferred—reportedly without board approval—to corporations controlled by Michael and David Shabsels. SIMAD Holdings Ltd. initially characterized the transfer as having occurred inadvertently, as a byproduct of the way the company had been run before it was listed.

- The audit committee ordered the brothers to return the full sum plus 7% interest (the coupon on the company's bonds) within one day. The brothers accepted but, the following day, said they could not return the money by the end of May and could not estimate when they could. Several Israel-based board members initially resigned, then suspended their resignations to aid recovery efforts.

- Because the funds were not returned, SIMAD Holdings Ltd. missed the first interest payment on its Series A debentures, due May 31, 2026—only about six months after the raise. On the disclosure the bonds collapsed roughly 38% in a single trading day (erasing an estimated NIS 240 million of value and pricing to a distressed yield of ~26%) before the Tel Aviv Stock Exchange suspended trading and Midroog, the Israel credit rating agency, cut the issuer to its default-level grade; the missed coupon was approximately NIS 21 million.

- Notably, the CRO's first-day declaration does not itself allege the transfer. It attributes the filing to the May 31 default and MCA-acceleration risk, and states that "the full circumstances that led to the filing … are still under investigation by the SIMAD Debtors and their professionals". These remain allegations and company/press disclosures; the Shabselses have not been criminally charged and have largely declined to comment.

The Acceleration Trigger: Merchant Cash Advances and Personal Guarantees

A defaulted bond alone need not have forced an emergency, in-season filing; the merchant-cash-advance book is what made the timing urgent. The SIMAD Debtors owed more than $100 million to roughly 42 MCA and short-term funders, many of whose contracts granted the right to debit SIMAD bank accounts directly via ACH, and some of whose loans matured in early June 2026. On the eve of the summer season, a single lender's enforcement could have triggered an enterprise-wide cash-seizure cascade. In the first-day declaration—not the cash-management motion—the CRO stated that the debtors do not believe the MCA lenders hold a perfected interest in the cash in the SIMAD Debtors' bank accounts.

- SIMAD Holdings Ltd. also disclosed that the owners had taken on personal financial commitments in significant amounts, secured on the assets and cash flows of the company's subsidiaries, raising the concern that assets pledged to bondholders may have been double-pledged—casting doubt on bondholders' ability to seize the 13 collateral camps. This double-pledge concern recurs below as both a recovery overhang for bondholders and an estate cause of action.

Regulatory Scrutiny and Prior Litigation

The default drew immediate regulatory attention in Israel, and it was not the brothers' first allegation of misconduct.

- Regulatory Scrutiny — The Israel Securities Authority ("ISA") opened an inquiry and requested documents, examining whether the distribution to the owners was consistent with the bond trust deed and whether securities laws were violated. Reporting indicated the ISA could seek to extradite the brothers—described as an unprecedented step—though as of mid-June 2026 they had not been criminally charged and had not responded to requests for comment.

- The Kiwi Takeover Suit — The owners of Kiwi Country Day Camp (Karla and Ivan Bellotto) sued in 2021, alleging the Shabselses orchestrated a hostile takeover—entering a partnership, then diluting the owners' stake, refinancing the property and distributing proceeds only to themselves, and withholding books and records. That case went to a five-day trial in summer 2025 before the brothers dismissed their attorneys mid-trial, and it resumed in May 2026. A separate suit involving Camp Lavi (Lavco LLC) in Lakewood, PA raised similar minority-dilution and records-access allegations.

- The Swiss Fund MCA Suit — In April 2026, the Shabsels parties sued Swiss Fund LLC in Connecticut Superior Court over a merchant-cash-advance contract: Damis had agreed to 42 weekly payments totaling $15 million for a $9.7 million advance and—after payoff letters and an April 15 notarized zero-balance statement—Swiss Fund allegedly demanded further payment and withdrew $117,187.50 from a Damis account on April 17. The complaint alleges breach of contract, statutory theft under Connecticut law, and unfair trade practices.

Chapter 11 Filing

The New Jersey case has several distinctive features: the estate's causes of action may rival the camps in value, it proceeds as a plenary U.S. Chapter 11 rather than an Israeli or BVI process, and the first-day relief was engineered around a single objective—opening the 2026 season on time.

Estate Causes of Action

Beyond the camps—appraised in connection with the bond offering at ~$466.6 million and likely to clear most of the funded debt in a going-concern sale—the estate's causes of action may be the principal source of recovery for junior and unsecured creditors, most efficiently captured through a post-confirmation litigation trust. The CRO has already done the two things that matter: he removed the Shabselses' access to cash and expressly reserved that the full circumstances that led to the filing of the Chapter 11 Cases are still under investigation by the SIMAD Debtors and their professionals. The principal claims a trust would price:

- Avoidance / Fraudulent Transfer: — The ~$34 million transferred to Shabsels-controlled entities "without board approval" is the anchor claim—pursued as an actual or constructive fraudulent transfer and/or unlawful distribution. The audit committee's one-day return demand and the brothers' inability to repay help establish both intent and harm.

- Merchant Cash Advance Preference Exposure — Shortly before the Petition Date, CT Corporation Systems and Corporation Service Company—standard MCA agent-filers—filed various UCCs against several SIMAD Debtors. Against a ~42-lender, $100M+ book with cross-guarantees and ACH access, those last-minute filings sit squarely within the 90-day window, and the estate already disputes perfection.

- Breach of Fiduciary Duty / D&O Claims — Against the Shabselses (and potentially directors) for authorizing or permitting the transfer and the personal-guarantee/double-pledge structure. The D&O insurance tower, not the personal estates, is likely the collectible source.

- Double-Pledge / Impairment of Collateral — The owners' personal commitments "secured on the assets and cash flows of the company's subsidiaries" may have encumbered assets pledged to bondholders, threatening the collateral camps—a claim of direct interest to the bond trustee.

- Veil-piercing / Substantive Consolidation — Commingling with DAMIS and the ~80 real-estate assets, plus the unapproved intercompany movement of cash, supports alter-ego theories that would expand the asset pool.

The threshold diligence question is not liability but collectability. Even well-founded claims against the Shabselses are only as valuable as the assets standing behind them — and with both brothers reportedly in personal bankruptcy, direct judgment recovery against their personal estates is likely limited. The D&O insurance tower is the most immediately accessible recovery source, existing precisely to cover breach of fiduciary duty claims against officers and directors. The DAMIS real-estate portfolio is a separate consideration: DAMIS Holdings filed its own chapter 11 and is being administered independently, meaning its assets are not automatically available to SIMAD creditors. Accessing them requires winning a veil-piercing or substantive consolidation argument — that SIMAD and DAMIS were operated as a single commingled enterprise by the same controlling shareholders — which, if successful, would expand the creditor recovery pool by whatever net equity survives DAMIS's own secured debt. A third avenue lies in the intercompany cash movements and insider transfers that remain under active investigation; the full scope of what moved, to whom, and when will not be known until the Schedules and Statements of Financial Affairs are filed.

Cross-Border Posture and Bondholder Recovery

The structural feature that distinguishes this case is the forum. SIMAD is a BVI parent whose only public debt trades in Tel Aviv but whose operating assets—the camps—sit in the United States. Rather than defaulting into an Israeli court process or a BVI liquidation and seeking ancillary U.S. relief under Chapter 15, the enterprise filed a full, plenary Chapter 11 in New Jersey. That choice is deliberate: it places the U.S. camp real estate and operating cash directly under the U.S. automatic stay, channels every creditor—including the Israeli bondholders—into a single U.S. claims-adjudication and plan process, and forecloses a race to enforce by the ~42 MCA lenders. It inverts the usual "Israeli bond default → Israeli trustee enforcement" path: here the Israeli trustee's recovery runs through the U.S. bankruptcy.

The U.S. record shows the bond trustee, Mishmeret Trust Company Ltd., was a co-architect of the filing: the board's authorizing resolutions were adopted "in coordination, cooperation and consultation with the Trustee for the Holdings' bondholders and its legal advisors in the United States," and the first cash-collateral order names "the Trustees and Bondholders" first among the secured "Reserving Lenders." Mishmeret retained dual U.S. counsel—Riker Danzig and Chapman and Cutler—within days.

This is a recognizable template. In All Year Holdings Ltd.—the Yoel Goldman BVI real-estate empire that defaulted on more than $750 million of TASE bonds—the identical trio now steering SIMAD ran a Chapter 11 in the Southern District of New York that proceeded in parallel with BVI and Tel Aviv District Court proceedings: Mishmeret as trustee, Chapman and Cutler as the trustee's U.S. counsel, and Assaf Ravid as CRO/CEO and later plan administrator. (In that case Ravid later alleged in court filings that Goldman had inflated financials and protected himself by paying personally guaranteed loans.) The SIMAD filing reprises that playbook deliberately.

Recovery for the bondholders—holding the ~$214 million asserted senior secured claim against an appraised ~$466.6 million portfolio—turns on a few swing factors rather than headline asset coverage. First and most important is collateral validity: whether the liens on the pledged camps are valid, perfected, and unencumbered, or whether the owners' personally guaranteed borrowings and the MCA financings double-pledged the same assets. Clean, first-priority liens point toward a high recovery on the secured portion; a successful double-pledge or avoidance challenge would push recovery into impaired territory. Second is the fate of the ~$34 million transfer, recoverable as an estate claw-back that augments the general estate (benefiting bondholders only to the extent of any unsecured deficiency claim). The third swing factor is process. A going-concern sale — one that preserves the camps as operating businesses and captures the brand equity, enrolled camper base, and revenue streams that underpin the $466.6 million appraisal — is the value-maximizing outcome. A piecemeal liquidation of camp real estate, by contrast, would realize a fraction of that figure; rural camp land divorced from its operating business is worth materially less than a functioning summer camp enterprise. How quickly the estate can execute a sale, and whether plan exclusivity holds long enough to run a controlled process, will directly determine where in that range bondholders land.

Restructuring, First-Day Relief and Case Status

SIMAD Holdings Ltd. engaged Assaf Ravid as Chief Restructuring Officer under an engagement letter dated June 2, 2026—two days before filing—drawing on the All Year experience described above. The SIMAD Debtors also engaged FTI Consulting, Inc. (to assist the CRO) and Cole Schotz P.C. (Michael D. Sirota) as counsel; B. Riley Securities helped prepare the initial budget; and Kroll Restructuring Administration LLC is the proposed claims/noticing agent. Upon his appointment, Ravid took control of the SIMAD Debtors' bank accounts—with the Shabselses ceding control and signatory changes underway—and, together with the individual camp directors, took operational control of the camp entities. The relief sought in the first days was built around a single objective: open the 2026 season on time.

Two-Stage Cash-Collateral Process (no DIP loan)

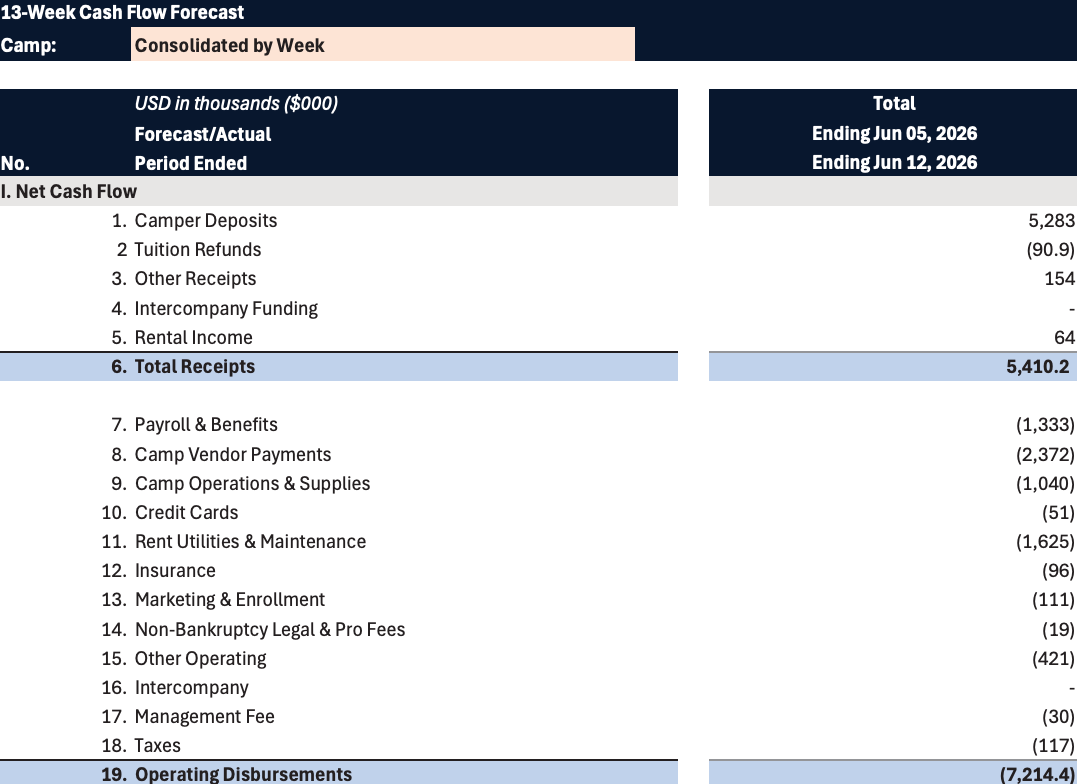

- Stage 1 (June 8) — At the emergency hearing, Chief Judge Gravelle entered an interim order authorizing the SIMAD Debtors to use cash, including cash collateral, and their existing bank accounts on a limited basis—solely to fund prepetition gross salaries, payroll taxes, and other emergent expenses "necessary to open the camps"—for the period from the Petition Date through and including June 15, 2026, under a B. Riley–prepared budget (operating disbursements of roughly $7.2 million for the opening window). This was a consensual cash-collateral order under § 363, not a DIP loan; no new financing was extended.

- Stage 2 (June 14) — The debtors filed a fuller, 97-page cash-collateral motion seeking interim and final orders to use cash collateral (the estates held ~$18.8 million of cash at filing), grant adequate protection, and schedule a final hearing within ~21 days, with adequate-protection terms negotiated lender-by-lender through separate interim orders for the bond trustee/Bank of New Hampshire, the U.S. SBA, Wayne Bank, Community Bank, HomeTrust Bank, Bank of America, and others. The proposed package is a standard one of § 361 replacement liens and § 507(b) superpriority claims (subject only to U.S. Trustee fees), with no professional-fee carve-out and no sale or plan milestones.

- Adequate protection — The June 8 order recognized three "Reserving Lenders"—the bondholders and their trustee (Mishmeret), Bank of New Hampshire, and Metropolitan Partners Group Administration, LLC (administrative agent for a group of private-credit funds)—preserving their rights to the extent they hold valid liens. Bank of New Hampshire alone was granted an express dollar-for-dollar replacement lien for post-petition diminution.

Press reporting indicates the Shabselses provided approximately $1.5 million to the bond trustee to help bridge the opening of the season — roughly $400,000 for legal and company expenses and approximately $940,000 for camp operations. That figure appears only in media accounts and is not reflected in the bankruptcy docket through June 15, 2026; the court record does not characterize the payment as a loan, gift, or settlement contribution. Whatever its form, it is a thin margin against the season's actual cash requirements. The debtors' own B. Riley-prepared budget shows $7.2 million of operating disbursements for the opening week alone, and the season hinges on sustained cash-collateral access — not on the bridge — to stay open through August.

Other First-Day Relief

- Cash management — The debtors sought to preserve a deliberately decentralized treasury of 92 bank accounts, structured on a camp-by-camp basis with generally one or two accounts per entity and no master concentration or sweep account at the holding company level. Intercompany transactions ceased at the Petition Date; the debtors sought authority to resume them postpetition with administrative expense status, subordinated to any existing liens on the cash used. The court was separately asked to direct the debtors' payment processors — Campminder, Shopify, Paysafe, and others — to continue honoring their existing agreements and processing camper payments without interruption.

- Critical vendors — The debtors sought authority to pay up to approximately $2.5 million on an interim basis and $3.5 million on a final basis to roughly 115 vendors whose services are essential to safe camp operations. The vendor universe spans six categories: food service, health and safety, construction and maintenance, busing and transportation, J-1 visa staffing and recruitment, and recreational program providers.

- Insurance — The debtors sought authority to pay approximately $3.1 million in outstanding premiums across roughly 27 policies brokered by Brown & Brown of Garden City Inc. A notable structural detail: SIMAD had historically routed its insurance premium payments through affiliate DAMIS rather than paying carriers directly, leaving $719,514 of SIMAD insurance funds sitting in DAMIS accounts as of the Petition Date. The proposed interim order directed DAMIS to turn those funds over immediately to fund an end-of-June installment — the first court-ordered asset transfer from DAMIS to SIMAD in the case.

- Utilities — The debtors proposed a $295,995 adequate assurance deposit — approximately 62% of one month's utility costs — against an aggregate utility spend of roughly $477,441 per month across approximately 30 camps, with the deposit to be held in a segregated account at Flagstar Bank.

Process, Sale and Deadlines

- Plan exclusivity, not a plan deadline — The petition states the "Chapter 11 Debtors Exclusive Right to File a Plan Expires on 10/2/2026." This is the debtors' 120-day plan-exclusivity period under 11 U.S.C. § 1121(b) (June 4 plus 120 days falls exactly on October 2, 2026)—the window in which only the debtors may file a plan—not a hard deadline to file or confirm a reorganization plan, and it is routinely extended for cause. (Doc. 1.)

- Sale process — Per the CRO, the debtors are exploring an expedited financing and/or sale transaction and have received expressions of interest from numerous parties, with FTI Consulting engaged to assist the CRO/debtors. As of mid-June 2026, however, no bid-procedures or § 363 sale motion had been filed.

Key Parties

With general unsecured claims estimated at only ~$2.7 million, no official creditors' committee, trustee, or examiner had been appointed as of mid-June 2026. The real contest is among the secured banks, the bond trustee, the MCA lenders, and an emergent recapitalization constituency.

- The Ad Hoc Camp Committee — A group of 20 camp directors and owners, together with Excelsior Camps LLC — an entity formed by three established multi-camp operators: The TLC Family of Camps led by Jay Jacobs, Horizon Camps led by Tony Stein, and CampGroup led by Mark Benerofe and Dayna Hardin — filed a notice of appearance on June 14, 2026 through Kirkland & Ellis and Duane Morris. The committee states its goal as moving "to properly and promptly capitalize all 30 camps as part of a holistic transaction to get all 30 camps out of these chapter 11 cases in July," citing late-July visiting day — when 2027 deposits typically come due — as the functional deadline. The committee states it has been in contact with the directors and owners of all 30 camps, with several of the remaining ten expressing support.

- The bond trustee — L. Mishmeret Trust Company Ltd. — the largest secured creditor at approximately $214 million — is represented by Riker Danzig and Chapman and Cutler LLP, both of which filed notices of appearance in the case.

- Private-credit and bank lenders — Metropolitan Partners Group Administration LLC was recognized as a Reserving Lender in the June 8 interim cash collateral order alongside Mishmeret and Bank of New Hampshire. The named bank lenders — Bank of New Hampshire, Wayne Bank, Fidelity Bank, and TriState Capital Bank — have each appeared through counsel in the case.

- MCA lender appearing — Ace Funding Source LLC has appeared in the case, reportedly reserving jury trial rights and contesting jurisdiction — a posture consistent with the anticipated lien validity and avoidance disputes that the MCA stack is expected to generate.

- Other camp-operator parties — Individual camp owners and operators — including the Blue Star operating family, the Rocking Horse Ranch and Splashdown Beach operators, and individual owner David A. Shabsels — have appeared separately through their own counsel.

- The DAMIS group — The affiliated DAMIS group is proceeding in its own jointly administered chapter 11 case under Case No. 26-16439, represented by Faegre Drinker Biddle and Reath LLP.

- Private-credit and bank lenders — Metropolitan Partners Group Administration LLC, a private-credit lender that extended a $50 million loan in May 2025 jointly to Debtors SIMAD Holdings LLC and DAMIS Holdings LLC, holds approximately $25.4 million in principal obligations outstanding against the SIMAD Debtors and their affiliates as of the Petition Date. Metropolitan was recognized as a Reserving Lender in the June 8 interim cash collateral order but is not addressed in the fuller Cash Collateral Motion, and has separately expressed interest in providing DIP financing to the SIMAD Debtors. The named bank lenders — Bank of New Hampshire, Wayne Bank, Fidelity Bank, and TriState Capital Bank — have each appeared through counsel in the case.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.