Case Summary: Simply Interior Homes Chapter 11

Simply Interior Homes filed for Chapter 11 to pursue a dual-track going-concern sale and liquidation after an undercapitalized carve-out, affiliate Live Comfortably's alleged failure to remit collected customer cash, and sponsor Centre Lane's refusal to provide capital support.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Rock Hill, South Carolina, Simply Interior Homes, LLC ("SIH"), along with its Debtor⁽¹⁾ affiliates (collectively, the "Debtors" or the "Company"), is a designer, sourcer, and wholesale supplier of home textile and décor “soft goods”— fashion bedding, window treatments, bath products, and furniture and décor (slipcovers, rugs, and floor coverings) — to major U.S. retail channels, including department stores, off-price retailers, e-commerce retailers, and home centers.

The Company operates an asset-light, B2B model — functioning as a wholesale supplier and sourcing partner rather than a vertically integrated manufacturer or brick-and-mortar retailer. Its value lies in customer programs, design and development capabilities, brand rights, and vendor relationships, not in owned production facilities or a retail footprint.

Simply Interior Homes and certain affiliates filed for Chapter 11 protection on June 8, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the District of Delaware, reporting approximately $100 million to $500 million in both assets and liabilities.

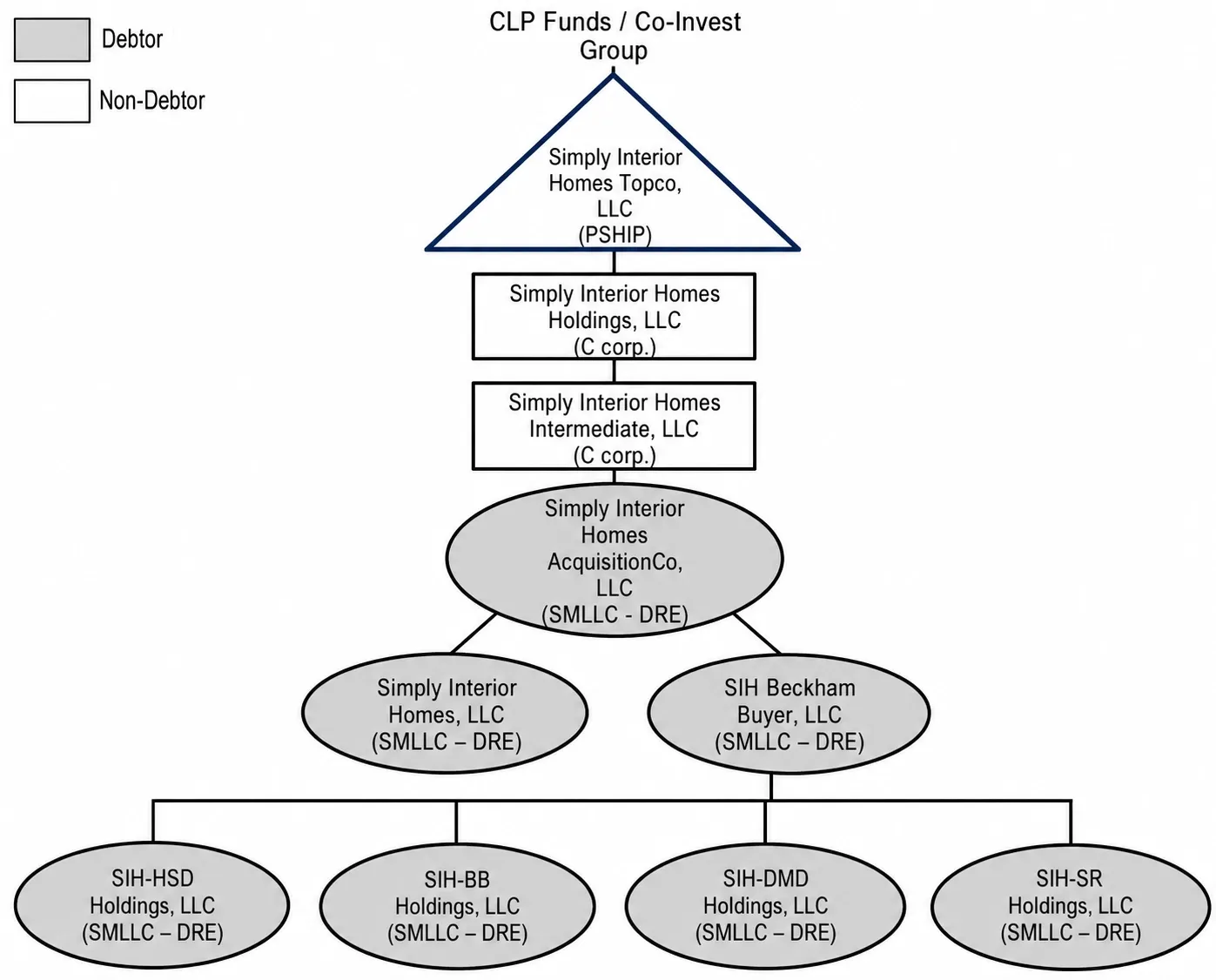

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

The Debtors were formed in connection with the carve-out of the soft goods business division from Keeco, LLC, one of North America's largest home textile suppliers, and a portfolio company of Centre Lane Partners ("CLP"). Keeco operated through two business segments: (1) utility bedding, such as pillows, comforters and mattress pads, and (2) soft goods, including blankets, sheets, comforters, quilts, throws, duvets, decorative pillows, and bed-in-a-bags, and blackout and decorative window curtains and shower curtains (collectively, “Soft Goods”).

Over approximately five years, CLP scaled Keeco through a series of acquisitions focused on utility bedding, and in the process of doing so, those acquisitions also added non-core Soft Goods categories that were not synergistic with the manufacturing-focused utility bedding platform.

The 2025 Carve-Out

In early 2025, CLP sponsored the separation of the Soft Goods division from Keeco into the standalone Debtors through a two-step structure.

- Step one: with Keeco's term loan facility in default, the Collateral Agent conducted a partial strict foreclosure under Article 9 of the UCC over certain Soft Goods collateral, which was transferred to CLP-designated transferees and ultimately vested in Debtor SIH, or Simply Interior Homes, LLC (f/k/a Soft Goods Operating, LLC).

- Step two: the parties completed the carve-out through a Membership Interest Purchase Agreement (the "MIPA") among Simply Interior Homes AcquisitionCo, LLC (f/k/a Soft Goods, LLC), as purchaser; Live Comfortably Borrower LLC (f/k/a Keeco Borrower LLC), as seller; and SIH, as the company—with the majority of the cash purchase price used to satisfy certain subordinated notes issued by SIH in connection with the foreclosure. Originally expected to close in late October 2024, the transaction closed roughly four months late, on February 21, 2025.

Concurrently, Keeco rebranded as "Live Comfortably" to focus exclusively on core utility bedding. The Debtors launched as an independent company with their own management, but CLP and its affiliates remained the indirect sole owner and effective decision-maker, and the Debtors continued to depend on Live Comfortably for many essential services—formalized in a Transition Services Agreement (the "TSA") and ancillary agreements executed at closing.

Organizational Structure

Operations Overview

The Debtors’ business model encompasses private label manufacturing, licensed brand development, and retail merchandising support, with a licensed and proprietary brand portfolio that includes:

- Eclipse — Window treatments built on light-blocking, noise-reducing blackout curtain solutions — carried at Walmart, HomeGoods, Amazon, and other major retailers.

- Hookless — Bath products built on patented hook-free shower-curtain technology — carried at Lowe’s, Home Depot, and other home improvement and mass merchant channels.

- Historic Charleston — A licensed bedding collection inspired by classic decorative arts.

- Kate Spade Home bath accessories — A premium licensed brand.

As of the Petition Date, the Debtors employ approximately 27 employees across their principal office in Rock Hill, South Carolina and their showroom and sourcing locations. The Debtors rely heavily on international sourcing and manufacturing partnerships, maintaining sourcing relationships with manufacturers and suppliers in India, Pakistan, China, and Vietnam, among other countries, with overseas sourcing infrastructure enabling the Debtors to manage tariff impacts, maintain production flexibility, and achieve speed-to-market delivery for their retail partners. In the ordinary course of business, the Debtors rely on third-party logistics providers and freight carriers to ensure the timely transport and delivery of home textiles merchandise and home décor products to their retail partners and distribution centers.

Transition Services Agreement with Live Comfortably

The Debtors entered into a Transition Services Agreement (the "TSA") with Live Comfortably at closing on February 21, 2025, under which Live Comfortably assumed responsibility for virtually every back-office function the Debtors needed to operate — IT infrastructure, accounting, payroll, logistics, and sales support. Notably, the TSA had been negotiated by CLP and Live Comfortably in 2024, before the Debtors' own management team had even been hired, and the CRO Declaration notes that CLP appears to have effectively directed Live Comfortably's performance under the agreement throughout its term.

That dependency quickly became a liability. Because the Debtors had no independent IT systems at formation and were delayed in updating their legal name with the IRS, they couldn't establish independent vendor accounts with major customers — forcing customer payments to flow through Live Comfortably's bank accounts well into 2026. Between January and May 2026, over 75% of the Debtors' collections — ranging from $300,000 to $1.5 million per week — landed in Live Comfortably's accounts rather than the Debtors'. The CRO alleges that Live Comfortably, acting under CLP's direction, routinely delayed passing those funds along despite repeated demands. As of June 7, 2026, $311,000 received during the week of May 31 still hadn't been remitted.

On top of that, the TSA carried trailing annual charges exceeding $2.7 million — a notable burden for a company already operating under significant liquidity constraints. As the relationship between the parties deteriorated, Live Comfortably, under the direction of CLP, threatened to terminate the TSA and discontinue the critical services provided thereunder. The CRO identifies that threat as a contributing factor in the Debtors' decision to commence these Chapter 11 Cases.

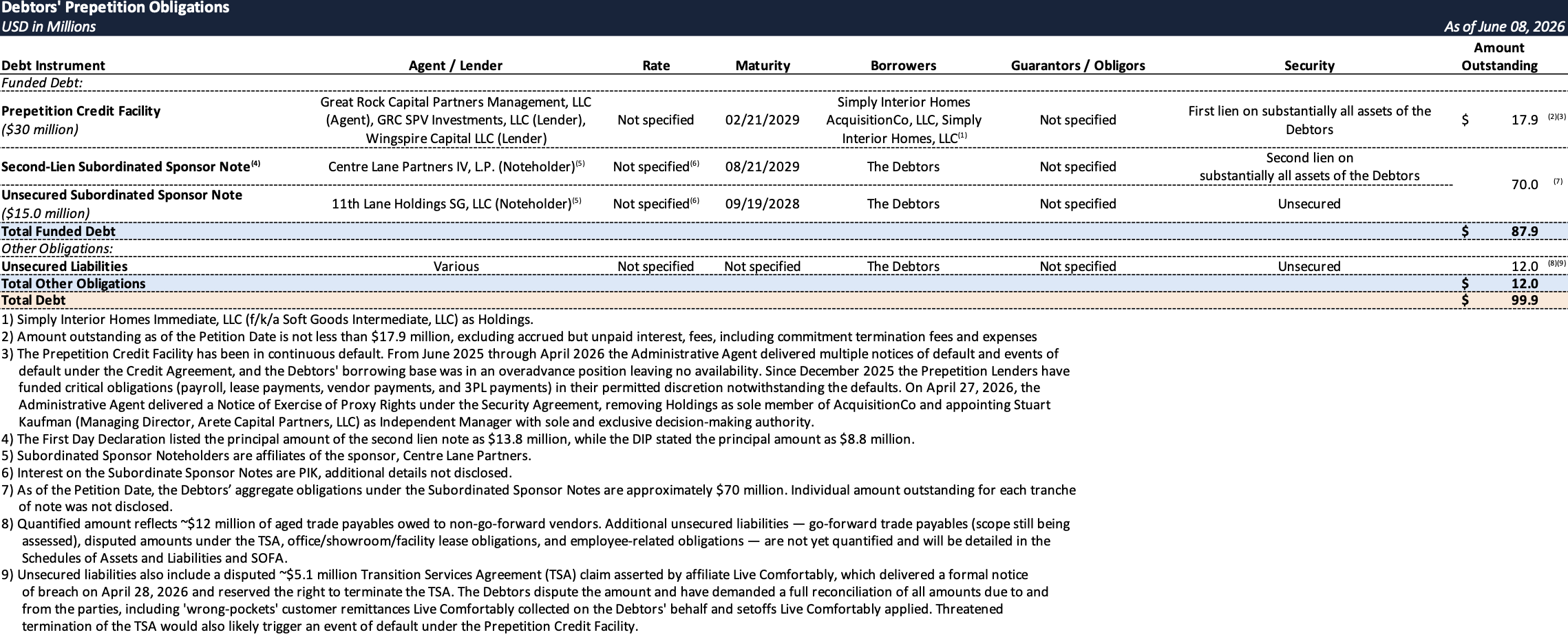

Prepetition Obligations

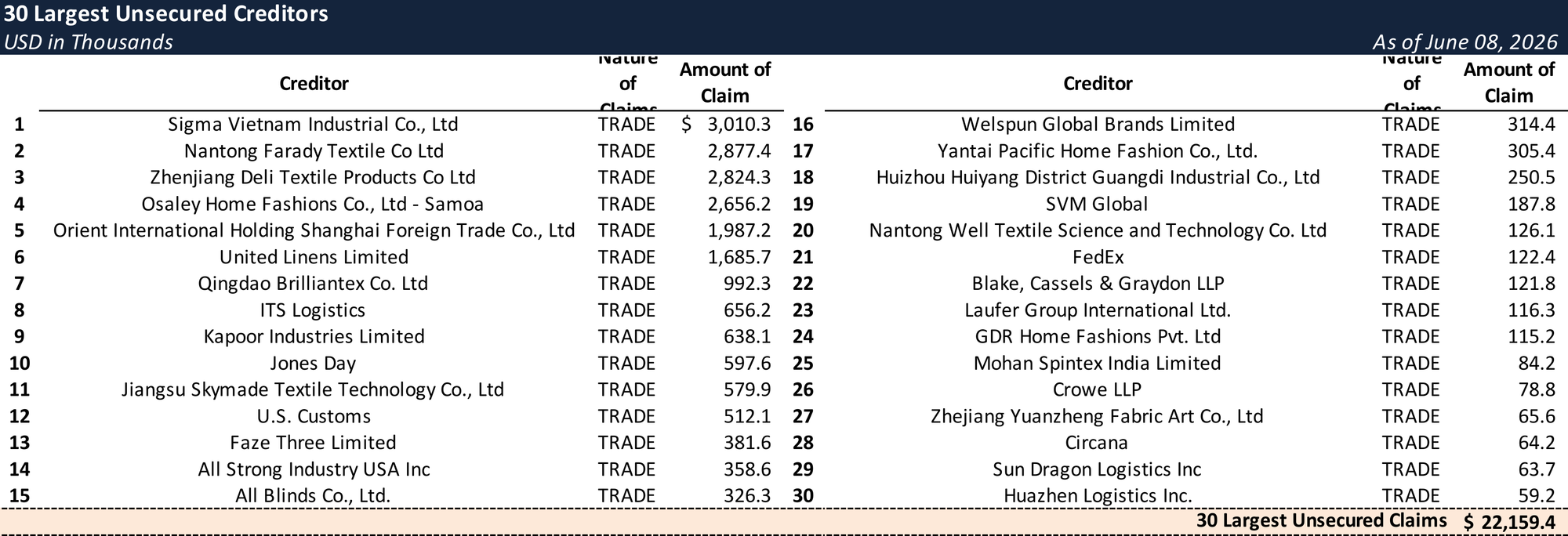

Top Unsecured Claims

Events Leading to Bankruptcy

Simply Interior Homes never recovered from how it was born. The Debtors attribute the filing to a chain of compounding failures—an undercapitalized launch, inherited operational deficiencies and lost customer programs, an escalating dispute with affiliate Live Comfortably under the TSA, the collapse of multiple sponsor-led recapitalization efforts, and reciprocal-tariff margin pressure—and have signaled they intend to investigate sponsor CLP's role throughout the cases (Doc. 11, ¶¶ 9–10, 34).

Undercapitalized Opening Balance Sheet and a Pre-Formation Revenue Strip

CLP projected that the carve-out business would open — on the original late-October 2024 timeline — with approximately $5 million of cash and $49 million of finished-goods inventory at closing, and generate substantial first-year sales and EBITDA in 2025; projections on which the Debtors' prospective lenders relied. The deal ultimately closed four months late, on February 21, 2025.

Actual conditions diverged sharply. To bridge the closing delay, CLP pre-funded the purchase price and released inventory, enabling its other portfolio company, Live Comfortably, to recognize approximately $21 million of Soft Goods revenue in January and February 2025 — before the Debtors were even formed. The Debtors opened instead with no cash, only approximately $27 million of inventory (of which approximately $22 million was excess and obsolete), and approximately $32 million of assumed accounts payable against a projected $25 million — payables that included those pre-formation sales. Newly hired management was required to immediately revise the 2025 revenue plan, cutting it from $185 million down to $86 million.

Operational Deficiencies

In fiscal year 2025, the Debtors generated approximately $84.7 million in gross revenue and $3.4 million in Adjusted EBITDA — both substantially below projections. The underperformance was driven in large part by poor customer service levels and an inadequate inventory mix inherited from Keeco. On the first day of operations, fill rates were approximately 30–40% across most product categories, well below the 95%-plus levels expected by retail partners, resulting in the loss of material sales programs with certain major customers, including Wal-Mart.

The Debtors implemented a comprehensive sales and operations improvement process that rebounded fill rates to over 90% by the fourth quarter of 2025. However, the damage to customer relationships had already been done — certain programs were never recommenced, permanently impairing the Debtors' revenue base.

Liquidity constraints compounded the deterioration on the vendor side. As the Debtors fell behind on supplier payments — due in part to Live Comfortably's failure to remit receivables collected under the TSA — vendors increasingly demanded cash-in-advance or prepayment terms, while others reduced or eliminated trade credit entirely. This created a self-reinforcing cycle in which tightening liquidity drove further vendor restrictions, which in turn constrained the Debtors' ability to procure inventory and fulfill customer orders. By the Petition Date, the Debtors had gone more than twelve weeks without making material payments to suppliers, prompting customs brokers and service providers to hold inventory at ports and in transit, and causing the majority of the Debtors' supplier base — including key overseas manufacturing partners — to suspend shipments altogether.

Tariffs Impact

Reciprocal tariffs that took effect on April 15, 2025 further compressed the Debtors' already strained margins. Despite management's requests for capital to address the impact, CLP provided limited financial support and directed the Debtors to forgo passing tariff cost increases through to customers, on the expectation that CLP would secure a tariff exemption. That exemption never materialized, and the compounding tariff burden continued to erode the Debtors' financial position throughout the second half of 2025 and into 2026.

Refinancing Efforts

Over the course of 2025 and into 2026, the Debtors and their stakeholders pursued multiple out-of-court alternatives to address the Debtors' deteriorating financial condition, none of which produced a sustainable solution. In early 2026, CLP advised the Debtors and the Prepetition Lenders that it planned to acquire a new business and roll it into the Debtors' existing operations on an accelerated timeline, with the goal of providing additional liquidity through the combined business and incremental term financing availability. To facilitate the transaction, CLP formed five new entities — SIH Beckham Buyer, LLC and its subsidiaries SIH-HSD Holdings, LLC, SIH-BB Holdings, LLC, SIH-DMD Holdings, LLC, and SIH-SR Holdings, LLC — all of which are named Debtors in these Chapter 11 Cases despite never having commenced operations.

The transaction ultimately could not close due to unavailability of financing. Its failure consumed significant resources, eliminated the Debtors' remaining path to recapitalization, and left them without any viable out-of-court restructuring option — a situation that CLP declined to remedy through additional financing or capital support. With no alternatives remaining, the Debtors and their restructuring advisor, Reflect, were left to evaluate all remaining options, ultimately leading to the commencement of these Chapter 11 Cases.

The TSA Dispute With Live Comfortably

On April 28, 2026, Live Comfortably delivered a formal notice of breach asserting approximately $5.1 million in unpaid TSA charges and reserving the right to terminate and suspend services. The Debtors dispute the figure and have demanded a full reconciliation — including a complete accounting of all historical wrong-pockets payments and setoffs — contending that Live Comfortably, at CLP's direction, improperly applied customer cash belonging to the Debtors' estate against amounts it claims are owed under the TSA.

The dispute is effectively two-sided. The Debtors carry the ~$5.1 million only as a disputed liability, against which they assert an offsetting intercompany receivable for customer remittances Live Comfortably collected but never credited — an amount that, given the scale of the uncredited remittances, could offset a material portion of Live Comfortably’s demand once a full reconciliation is completed, leaving open whether the Debtors are ultimately a net debtor or net creditor in the relationship.

The stakes extend beyond the dollar dispute. Because substantially all of the Debtors' core back-office functions remain housed within the TSA, a termination would be potentially catastrophic to the Debtors' operations and would likely trigger an event of default under the Prepetition Credit Facility. For that reason, the Debtors have expressly demanded that Live Comfortably continue performing all of its obligations under the TSA while simultaneously directing CLP to cease engaging the Debtors' customers, vendors, and lenders on the Debtors' behalf.

The ABL Default and Proxy Exercise

From June 2025 through April 2026, the Administrative Agent delivered multiple notices of default and events of default to the Debtors and CLP under the Prepetition Credit Facility. The Debtors' borrowing base had fallen into an overadvance position, leaving no available financing. Beginning in December 2025, the Prepetition Lenders stepped in to fund critical obligations — including payroll, lease payments, vendor payments, and third-party logistics costs — on a discretionary basis notwithstanding the ongoing defaults, though the lack of available liquidity continued to strain the Debtors' ability to pay vendors and service customers on a going-concern basis.

After CLP repeatedly refused to provide the liquidity and capital support the Debtors had requested, the Administrative Agent took more decisive action. On April 27, 2026, it delivered a Notice of Exercise of Proxy Rights, acting as proxy and attorney-in-fact under the Security Agreement to remove Holdings as sole member of AcquisitionCo and appoint Stuart Kaufman, Managing Director of Arete Capital Partners, LLC, as Independent Manager of AcquisitionCo with sole and exclusive decision-making authority.

Following the Proxy Exercise, the newly constituted management — acting through Goodwin Procter LLP as replacement counsel — directed CLP and its affiliates, including Live Comfortably, to immediately cease engaging with the Debtors' customers, vendors, and lenders, and to cooperate fully with the Independent Manager in transitioning control of the business. The Prepetition Lenders continued to provide limited discretionary funding for critical obligations post-Proxy Exercise, but that funding proved insufficient to satisfy outstanding vendor obligations or sustain operations through the Petition Date.

Determination to File and the Dual-Track Path Forward

Facing unfundable liquidity needs, a disputed but operationally indispensable TSA, damaged supplier relationships, and existing defaults under the Prepetition Credit Facility, the Debtors determined that a value-maximizing sale and liquidation process represented the best available path forward for their estates and stakeholders.

The structure is explicitly dual-track. SB360 Capital Partners — selected from a field of four firms — has been engaged as liquidation consultant to conduct an orderly liquidation of the Debtors' on-hand and in-transit inventory, accounts receivable, and FF&E, running in parallel with a going-concern sale and marketing process being led by investment banker Rock Creek Advisors. Any assets successfully sold through the Rock Creek process would be removed from the liquidation, with the two workstreams operating simultaneously to maximize blended recovery.

DIP Financing

The Debtors secured a superpriority revolving $15.0 million DIP facility, of which $5.0 million is new-money, with the same Great Rock/Wingspire lender group that holds the prepetition debt — a structure that is effectively lender-controlled and loan-to-own-adjacent in character. The facility also includes a $10.0 million roll-up tranche at a 3:1 ratio — but converting only on the first $3,333,333 of new money drawn, meaning the full $10.0 million roll-up is complete after the Debtors access just $3.3 million of new cash. Pricing is Adjusted Term SOFR plus 7.50% cash pay, with a 0.75% unused-line fee, a $5,000 per month collateral monitoring fee, and a $100,000 PIK closing fee (equal to 2.00% on the new-money commitment), maturing September 30, 2026. The facility includes a Carve-Out comprising $25,000 for a Chapter 7 trustee and a $200,000 post-trigger professional-fee cap, and funds the dual-track going-concern sale and liquidation process.

Critically, while the Debtors stipulate to the validity of the prepetition debt and grant broad releases, those releases run exclusively to the Prepetition and DIP Secured Parties — Great Rock and Wingspire — in their capacities as such. CLP and Live Comfortably are expressly outside the release perimeter, and any party with standing retains the right to file a Challenge within 75 days of entry of the Interim Order, preserving the estate's avoidance, recharacterization, and affiliate-liability claims against the sponsor.

The sale timeline is compressed and hard-wired to the DIP facility. With no stalking horse identified at filing, the Debtors are targeting a bid deadline of July 27, an auction on July 30, a sale hearing on August 6, and a closing by August 13 — all running inside a liquidating Chapter 11 plan that contemplates a Plan and Disclosure Statement by July 22, confirmation around September 18, and a DIP maturity of September 30. The plan itself contemplates the establishment of both a Liquidating Trust and a Litigation Trust upon confirmation.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.