Case Summary: Sleep Number Chapter 11

Sleep Number filed Chapter 11 to sell its assets to Fairfax-owned Sleep Country Canada for $415M through a lender-backed Section 363 process, after a multi-year mattress recession and a pandemic-era balance sheet left the smart-bed maker with roughly $672.5M of funded debt it could no longer carry.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Minneapolis, Minnesota, Sleep Number Corporation ("SNBC," Nasdaq: SNBR), along with its Debtor⁽¹⁾ affiliates (collectively, "Sleep Number" or the "Company"), is a vertically integrated developer, manufacturer, retailer, and servicer of personalized "smart beds" sold direct-to-consumer, positioning itself as the leader in personalized sleep wellness. The Company's mattresses are designed to evolve with each sleeper, featuring adjustable firmness, pressure-relieving support, and temperature-balancing comfort. The Company holds over 1,000 patents and patents pending, has accumulated billions of hours of sleep data, and claims to have helped more than 16 million people achieve better sleep across nearly 40 years of operation.

As of the Petition Date, Sleep Number employs approximately 2,920 employees located across multiple sites in the United States. Contract workers typically account for approximately 18% of Sleep Number's total workforce. The Company operates 572 Sleep Number stores with locations across all 50 U.S. states, targeting high-quality, convenient, and visible locations.

Sleep Number Corporation and four affiliated Debtors filed for Chapter 11 protection on June 12, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Southern District of New York, reporting $642.3 million in assets and $1.3 billion in liabilities (as of April 30, 2026).

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

Sleep Number Corporation was founded in 1987 as Select Comfort Corporation. The Company opened its first retail store in 1992, bringing personalized sleep solutions directly to customers, and in 2000 introduced home delivery and professional set-up services. The Company became publicly traded in 1998 and is listed on the Nasdaq Global Select Market under the symbol "SNBR." In 2017, Select Comfort Corporation changed its legal name to Sleep Number Corporation and rebranded as "Sleep Number."

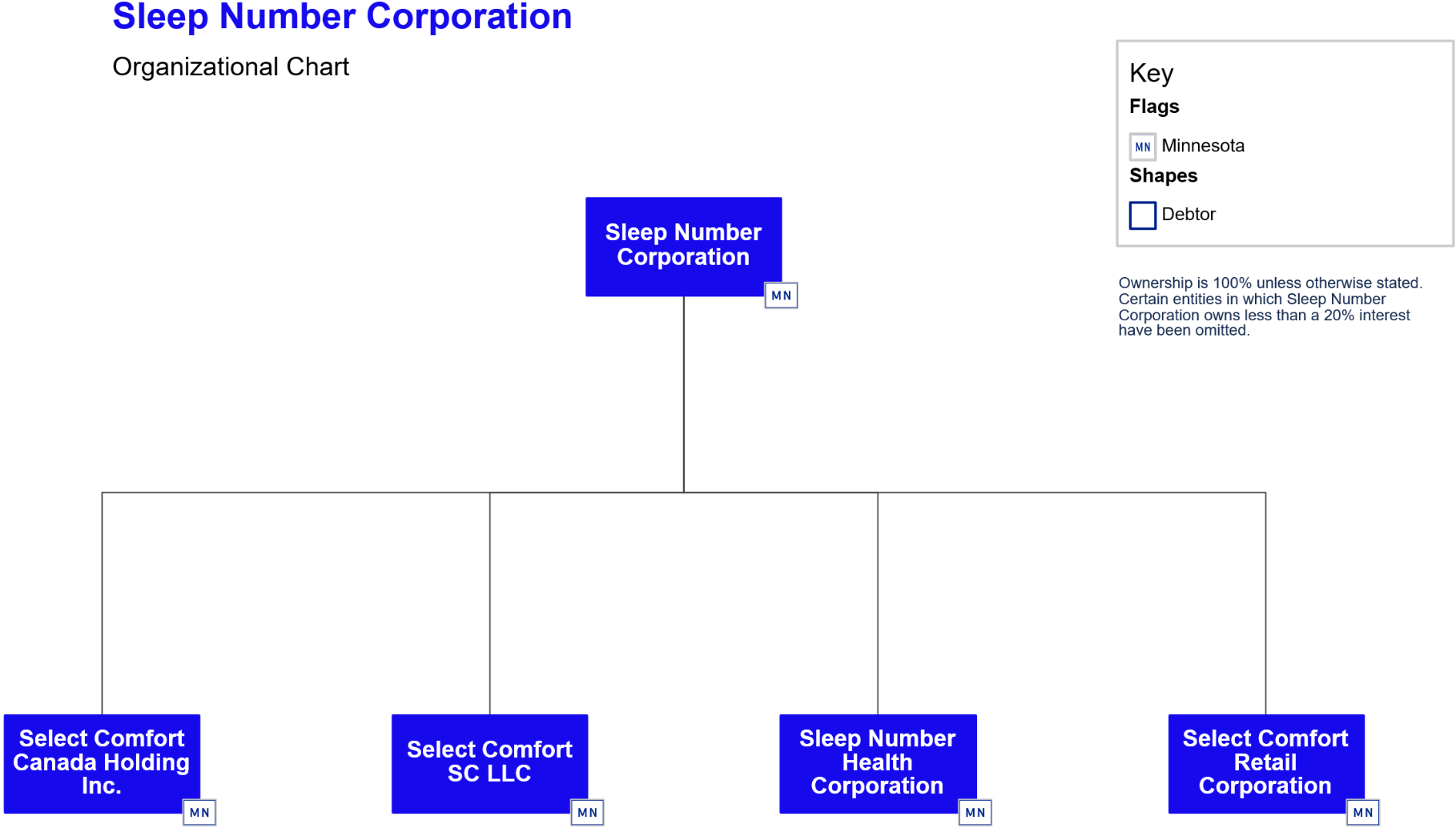

Corporate Structure

SNBC is a Minnesota corporation and public holding company that wholly owns its four direct subsidiaries, each a co-Debtor in the Chapter 11 Cases.

Operations Overview

Sleep Number runs an exclusively direct-to-consumer model it calls "Total Retail," selling through its own stores, online, phone, and chat rather than any third-party mattress retailer; stores function largely as showrooms within a "sell-from-anywhere" framework, with digital channels driving education, conversion, and retention. During the LTM period ended April 4, 2026, Sleep Number generated approximately $1.34 billion in net sales, with retail stores contributing approximately $1.17 billion, or roughly 87% of total revenue.

Product Portfolio

Sleep Number's mattresses and bases are "smart" products combining physical and digital innovations, featuring four core capabilities: (1) signature firmness adjustability, (2) digital sensing providing sleep health and quality metrics, (3) "sense and do" technology that automatically adjusts the mattress throughout the night; and (4) individualized temperature control, including the Climate360® system. Smart mattresses are also updated regularly through over-the-air software updates.

In March 2026, the Company announced a redesigned portfolio, streamlining its lineup from 12 to seven beds across three collections — ComfortMode™, ComfortNext™, and Climate™ — with two of the new beds introducing Sleep Number's first Tri-Brid™ design combining micro coils, foam, and adjustable air. The Company has received broad industry recognition, including #1 in customer satisfaction in the J.D. Power 2025 U.S. Mattress Satisfaction Study, America's Best in Customer Service by USA Today in 2026, and One of the Most Trustworthy Companies in America by Newsweek in 2026. The ClimateCool® smart bed received recognition from TIME, Forbes, Esquire, Men's Health, and Oprah Daily in 2025, and the Climate360® was named Best Smart Bed for Temperature Control by Forbes.

Supply Chain and Manufacturing

- Raw Materials Sourcing - Sleep Number sources the raw materials and components used in its products from a network of third-party global suppliers. To mitigate supply disruption risk, the Company has pursued measures including strengthening primary supplier relationships, identifying alternate suppliers, redesigning products, exploring alternative components, and maintaining safety stocks. The Company also operates a dedicated cut and sew facility for cover production in Irmo, SC and an advanced engineering and prototyping facility in Salt Lake City, UT.

- Smart Beds Assembly - All smart beds and mattresses are pre-assembled in assembly distribution centers prior to delivery, on a made-to-order basis with minimal raw materials, work-in-process, and finished goods inventories. The Company operates five assembly distribution centers located in Minneapolis, MN; Cincinnati, OH; Dallas, TX; Irmo, SC; and Salt Lake City, UT. Bedding fulfillment is centralized in Ohio to serve the entire United States. The Company continues to advance its outbound logistics network by evolving its mix of truckload carriers and dedicated cross docks to reduce product handling, damage, and costs while in transit to customers' homes.

- Delivery and Installation - Delivery and installation of Sleep Number smart beds and mattresses are handled by Sleep Number delivery technicians or trained third-party service providers under a blended model designed to deliver a strong customer experience. Post-purchase customer support is provided via phone, email, chat, and social media, with a portion of customer service operations outsourced for efficiency.

- Research & Development - The Company's global R&D team operates across onshore locations in Minneapolis, MN and San Jose, CA and offshore teams in Europe and Asia, covering mechanical engineering, comfort, adjustability, temperature, anthropometrics, and test systems. R&D expenses were $34 million in 2025, down from $45 million in 2024. The sleep wellness platform collects and analyzes data through a research-grade, multi-sensor ecosystem leveraging ballistocardiography, AI/ML algorithms, and cloud infrastructure, having accumulated more than 38 billion hours of sleep data from over 4.8 billion real-world sleep sessions.

Sales and Marketing

Sleep Number operates an exclusive direct-to-consumer distribution model, delivering an experience that integrates digital and physical touchpoints. As the exclusive distributor of its own products, the Company maintains a nationwide portfolio of retail stores, targeting high-quality, convenient, and visible locations based on market sales and profit potential, store geography, demographics, and proximity to other brand experiences. Since 2010, the Company has repositioned a large percentage of its mall stores to stronger, optimally sized non-mall locations. In 2025, stores accounted for 88% of net sales, with the remaining 12% derived from online and other sales channels.

The Company's loyalty rewards program, Smart Sleepers℠, has accumulated over 1.9 million members, with the most dedicated members participating in over 3 million engagements per year on the Company's digital platform through video, web, email, and blog content. Smart Sleepers also post product reviews on social media, which the Company describes as activating the marketing flywheel and advancing brand exposure.

In 2025, Sleep Number reset its marketing strategy to attract consumers from a larger addressable market, and in April 2026 launched its newest integrated marketing campaign, "To a Good Life's Sleep," its first major integrated campaign in several years. The campaign marks a shift away from feature-centric and utility-based messaging toward a benefit-focused narrative designed to support Sleep Number's full portfolio across every price point, from entry-level options to premium smart beds.

Intellectual Property

Sleep Number's intellectual property portfolio is a key component of its business, centered on its patent holdings with particular focus on smart features that improve sleep quality and thermal solutions for temperature disruptions. As of the Petition Date, the Company holds various U.S. and foreign patents and patent applications covering air control systems, remote control systems, air chamber features, mattress construction, foundation systems, sensing systems, automated adjustments, and in-bed temperature control, among other technologies. The Company also owns U.S.-registered trademarks and service marks, several of which have been registered or have pending applications in various foreign countries, and holds additional intellectual property rights including trade secrets, trade dress, and copyrights related to its products, processes, and technologies.

Partnerships and Collaborations

- Sports & Entertainment - Sleep Number has been the Official Sleep and Wellness Partner of the NFL since 2018, with the partnership extending to the NFL Players Association and the Professional Football Athletic Trainers Society. At the club level, the Company held partnerships in 2025 with the Los Angeles Rams, the Dallas Cowboys, and the Minnesota Vikings, supporting national media and community-activation efforts in some of Sleep Number's most important markets. In January 2026, the Company announced a strategic partnership with three-time Super Bowl Champion Travis Kelce, under which Kelce committed to acquire common stock on the open market, receive compensatory restricted stock units vesting over the initial three-year term of the relationship subject to customary vesting conditions, and participate in future marketing efforts pursued by the Company.

- Health & Research Institutions - Sleep Number has established research partnerships with several prominent health and wellness institutions, using its longitudinal sleep data as the foundation for studies on health-related topics. Research partners include the Mayo Clinic, the American Cancer Society, Northwestern University, and the University of Pittsburgh. In 2020, Sleep Number entered a collaboration with the Mayo Clinic covering multiple research projects, including studies on the relationship between disrupted sleep and markers of aging, the cardiovascular implications of excessive daytime sleepiness, and the prevalence of disordered sleep conditions — including sleep apnea, insomnia, and short sleep — among patients with Somali heritage and associated cardiovascular risk factors. In 2022, Sleep Number partnered with the American Cancer Society to study the connection between cancer and sleep quality, with the stated goal of developing sleep strategies and guidance for cancer patients and survivors over a six-year research period. The Company has also donated sleep products to the American Cancer Society's Hope Lodge locations in support of cancer patients and caregivers.

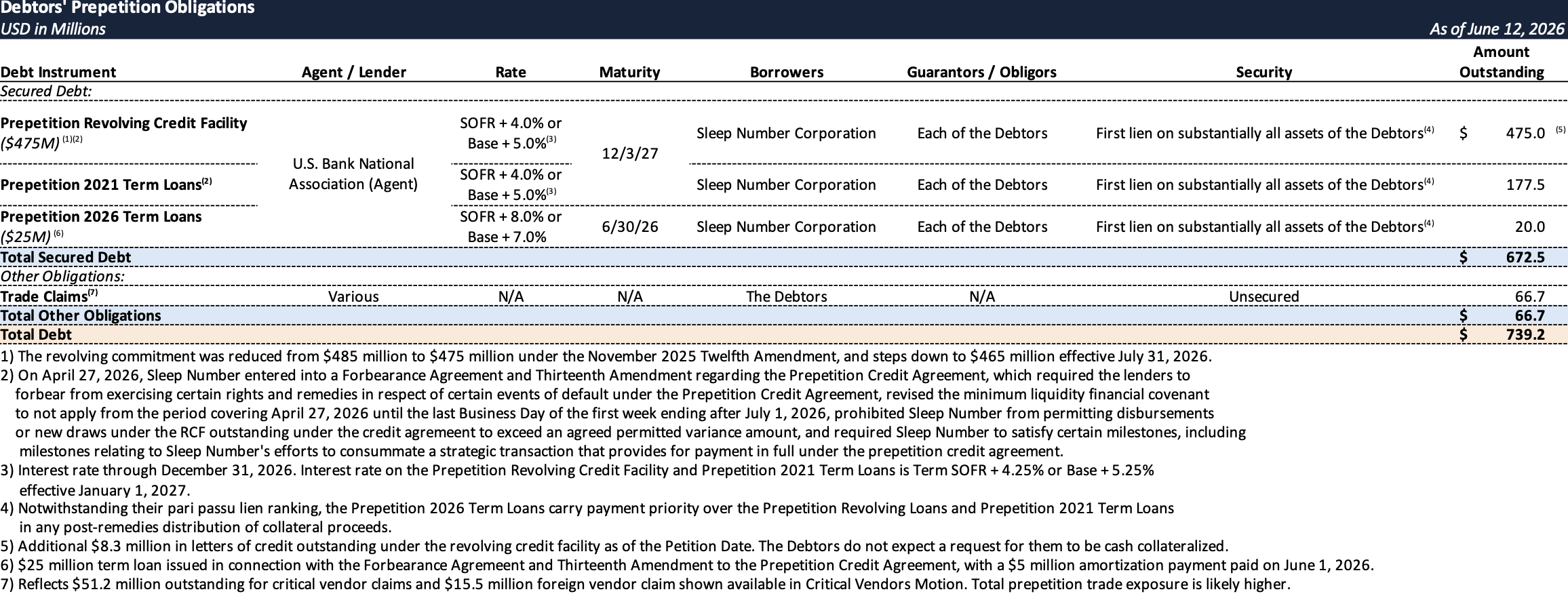

Prepetition Obligations

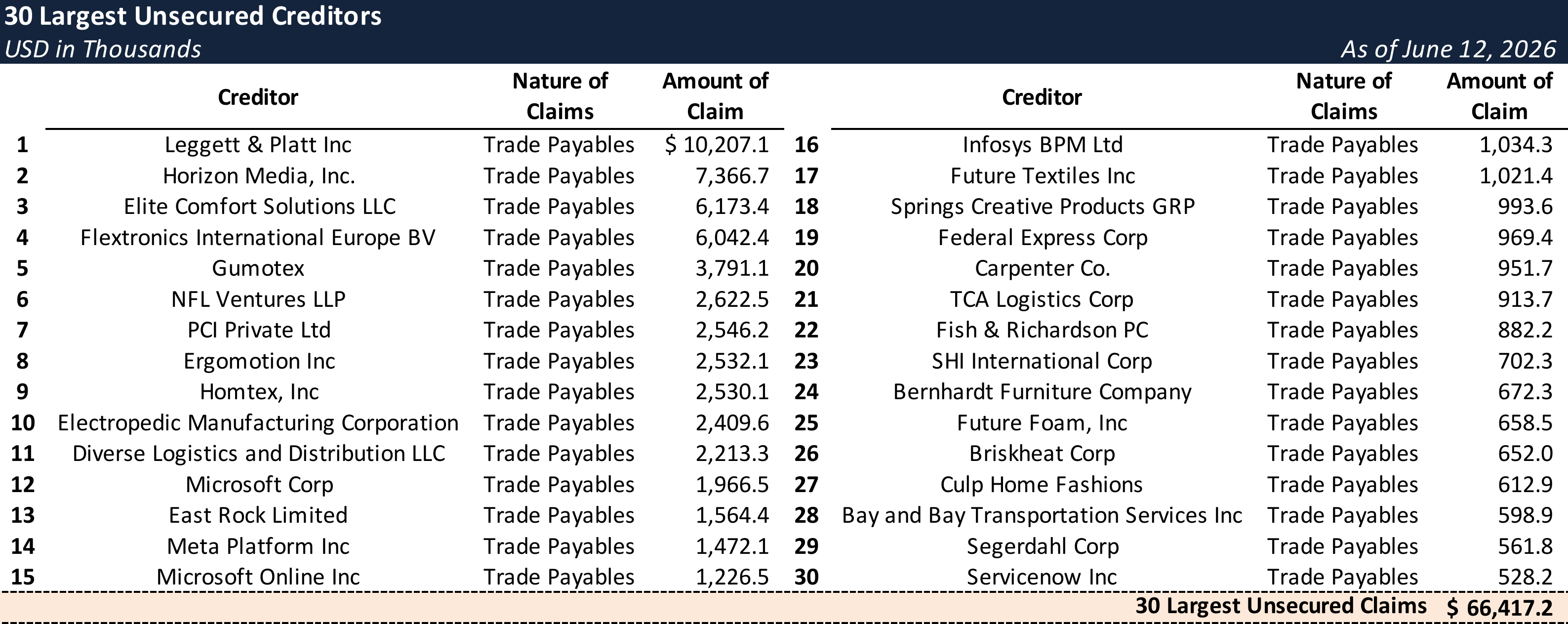

Top Unsecured Claims

Events Leading to Bankruptcy

Sleep Number's financial distress was compounded by strategic decisions made during the pandemic, when the Company experienced a significant demand spike and pursued an expansion strategy that over-extended its cost structure across store footprint, manufacturing capabilities, and debt levels — the resulting leverage ultimately reducing its ability to navigate prolonged macroeconomic headwinds.

Macroeconomic Headwinds

Over the past decade, the mattress retail industry has experienced broad-based distress driven by a structural shift toward e-commerce, declining in-store foot traffic, challenges in maintaining a right-sized real estate and distribution footprint, and compressing profit margins. Sleep Number was not immune, facing the cumulative headwinds of heightened competition, reduced discretionary consumer spending, an unpredictable regulatory environment, elevated inflation and interest rates, and a less dependable global supply chain, all of which weighed materially on the Company's financial performance.

A distinct and more recent pressure came from the unpredictable shifting of U.S. trade policy beginning in April 2025, when the U.S. government began imposing a new wave of tariffs on imported goods under various schemes, including under the International Emergency Economic Powers Act of 1977 ("IEEPA"), which applied to certain of Sleep Number's direct import products during fiscal year 2025. While the U.S. Supreme Court's February 2026 ruling determined that IEEPA does not authorize the President to impose tariffs, the broader trade landscape remained complex, and the Company continued to navigate ongoing regulatory uncertainties regarding potential alternative tariff frameworks.

Internal Cost-Cutting Measures

In April 2025, the Company appointed Linda Findley as CEO to lead its turnaround, who immediately initiated efforts to fix the capital structure and streamline operations by consolidating roles across key functions, strengthening accountability, and creating a nimbler organization designed to enable faster decision-making. These efforts reduced operating costs by $136 million compared to 2024 (excluding restructuring and other non-recurring costs), through optimizing the real estate portfolio and right-sizing the fixed cost base.

In November 2025, the Company introduced its turnaround strategy "Sleep Number Shifts," a focused, company-wide effort centered on three pillars: (a) Product — simplifying the offering with the goal of growing the customer base while building on repeat customer demand; (b) Marketing — modernizing efforts by expanding channels and reach with new creative to better connect with today's consumer and drive engagement with a focus on better return on investment; and (c) Distribution — optimizing store footprints and exploring opportunities to expand into new channels, both physical and digital. Collectively, these efforts improved the Company's liquidity position and provided the breathing room necessary to transition to exploring long-term restructuring options in 2026.

Financing Efforts

To assist in analyzing its financing needs and developing capital structure solutions, Sleep Number retained Guggenheim Securities, LLC as investment banker in February 2026, engaged AlixPartners, LLP as operational advisor to assist with the business plan and transformation, accelerate cost savings, and support contingency preparations, and mandated Davis Polk & Wardwell LLP as counsel. Together with its advisors, the Company pursued a range of alternatives including seeking recapitalization and financing opportunities from new and existing sources, soliciting interest in strategic combinations, and marketing its assets and operations to third parties.

In March 2026, Guggenheim contacted 33 parties in connection with an active solicitation of recapitalization and bridge financing proposals, 26 of which executed non-disclosure agreements and were granted access to diligence materials. Ultimately, only one written recapitalization proposal was received, which the Company determined was not actionable nor in the best interests of stakeholders. While several proposals for senior bridge financing were received, the existing lender group would not consent to being primed, and no actionable proposals for unsecured or junior financing were received. The Company concluded that the only viable pathway was to raise incremental bridge liquidity from its existing lenders while launching a marketing process to identify a purchaser for its assets as a going-concern sale.

To shore up liquidity in parallel with its restructuring efforts, the Company incurred the Prepetition 2026 Term Loans in April 2026 for general corporate purposes to improve its liquidity position and remain focused on its strategic objectives. Additionally, on May 13, 2026, pursuant to a participation agreement under the Thirteenth Amendment, SNBC sold to a third-party buyer all of its rights in its claims for tariff refunds previously paid to U.S. Customs and Border Protection under IEEPA, along with related rights (the "IEEPA Tariff Refund Sale"). While the additional liquidity made available through the cost-cutting measures, Prepetition 2026 Term Loan Financing, and IEEPA Tariff Refund Sale was not sufficient to fully address the Company's continuing financial obligations and commitments, it provided Sleep Number with sufficient runway to pursue a robust prepetition marketing process and identify the Stalking Horse Bidder to support the implementation of a value-maximizing sale transaction in these Chapter 11 Cases.

Special Transactions Committee

In connection with the financing efforts, the Board implemented several governance enhancements, including the creation of a Special Transactions Committee in March 2026 to lead the refinancing and strategic alternatives initiative. On June 4, 2026, the Board appointed Colin M. Adams — a director with significant restructuring experience — to the boards of each of the Debtors and as a member of the Special Transactions Committee, with Mr. Adams also serving as the sole member of the Special Investigations Committee established to evaluate certain potential claims the Debtors may hold. On June 12, 2026, the Board appointed Kent Percy of AP Services, LLC as Chief Restructuring Officer to assist with the Chapter 11 filings and provide certain management services in connection with the Chapter 11 Cases.

Prepetition Sale and Marketing Process

Prior to the Petition Date, Sleep Number conducted a robust 14-week prepetition marketing process for the sale of substantially all of its assets. With the assistance of Guggenheim Securities, the Company prepared marketing materials and contacted 53 potential strategic and financial purchasers, of which 19 executed non-disclosure agreements and were provided with a confidential information memorandum and access to a virtual data room, and five submitted preliminary proposals.

As a result of this process, the Company secured an agreement with SNBR Inc., an affiliate of Sleep Country Canada Inc. (the "Stalking Horse Bidder" or "Sleep Country"), to serve as the stalking horse bidder for the sale of substantially all of the Company's assets. Sleep Country, founded in 1994 and operating under the Sleep Country™, Dormez-vous™, Casper™ (Casper Canada), Endy™, Hush™, Silk & Snow™, and Simba™ (United Kingdom) banners, is Canada's leading specialty sleep retailer operating a network of over 300 corporate-owned stores. Under the Stalking Horse APA dated June 12, 2026, the Stalking Horse Bidder has committed, subject to Court approval, to acquire substantially all of the Company's assets for a base purchase price of $415 million in cash and the assumption of certain liabilities, subject to certain potential purchase price adjustments.

Chapter 11 Filing

The DIP Facility

The Debtors obtained a $260 million superpriority priming DIP facility documented as the Fourteenth Amendment to the existing Amended and Restated Credit and Security Agreement, with U.S. Bank National Association as administrative agent. All prepetition lenders participated — 100% of the revolving, 2021 term, and 2026 term loan lenders — eliminating any priming consent issue.

- Facility Size - The facility consists of $65 million in new money term loans, structured as delayed draws with up to $50 million available upon entry of the Interim Order and the balance upon the Final Order, plus a $195 million 3:1 roll-up of prepetition secured obligations that builds draw-by-draw as new money is funded. Pricing is Term SOFR plus 800 basis points.

- DIP Fees - Fees total approximately $11.4 million, comprising a $5.2 million upfront fee, a $5.2 million exit fee, and approximately $1 million in agent administrative fees. Maturity is approximately three months from the Fourteenth Amendment effective date.

- Structural Protections and Lender Package - The facility includes a standard Carve-Out for professional fees, with post-trigger fees capped at $2.5 million. A segregated funded reserve mechanism requires the Debtors to prefund accrued professional fees weekly. Parties in interest may investigate — but not prosecute — the prepetition liens and obligations within a $100,000 budget. The Challenge Deadline runs to the earlier of 60 days after committee formation (or 75 days after the Interim Order if no committee is appointed) and the commencement of the Sale Hearing.

- Sale Milestones - The DIP facility imposes binding case milestones that constitute events of default if missed. The Interim Order must be entered within three days of the Petition Date; the Final Order within 30 days. Bidding procedures must be approved within 28 days and qualified bids submitted by the same deadline. If qualified bids are received, an auction must be conducted by July 13, 2026; a sale order entered by July 15; and the sale closed by July 31. These milestones run concurrently with the Challenge Deadline, compressing the effective window for any committee investigation.

The Stalking-Horse Sale

SNBR Inc., a Delaware corporation and an affiliate of Sleep Country Canada Inc., committed to buy substantially all assets for $415 million cash plus assumption of certain liabilities.

- Purchase Price - $415 million base cash, adjusted at closing: plus Prepaid Rent; plus or minus Closing Working Capital vs. a $101.4 million target (Inventory capped at $105.5 million for working capital purposes, Accounts Payable capped at $10.28 million); minus $25 million Adjustment Escrow released post-reconciliation; minus Cure Costs exceeding the $8 million Cure Cap plus all post-petition cure amounts; minus the Processor Reserve Deposit; minus any Additional Inventory Shortfall (40% of Customer Deposit Balance over actual inventory, one-way downward only); minus any Marketing Expenditure Shortfall vs. a $30 million spend commitment.

- Bid protections - The stalking horse is entitled to a break-up fee of $12.45 million, representing 3% of the base purchase price, plus an expense reimbursement capped at $4 million, both of which constitute allowed administrative expense claims that survive termination of the APA, conversion of the cases, and plan confirmation. To displace the stalking horse, a competing bidder must clear an effective floor of $441.45 million — covering the $415 million base price, the $16.45 million in bid protections payable in cash, and a $10 million minimum overbid that may be satisfied in cash or non-cash consideration. The stalking horse receives a credit equal to the full bid protections amount in each auction round, preserving its competitive position against higher bids. A good faith deposit of $41.5 million is required; in the event of a buyer breach, forfeiture of that deposit is the estate's sole remedy absent fraud or willful breach.

Lease Considerations

Sleep Number's lease portfolio represents one of the more consequential open variables in this sale. The Company operates 572 leased retail stores across all 50 states — it owns no real property — carrying approximately $348 million in present value of operating lease liabilities as of April 4, 2026. The $18 million in lease impairment charges recorded in Q1 2026 alone, reflecting locations that had already ceased or were planning to cease operations before the filing, signals that the portfolio was already under stress heading into Chapter 11.

The Debtors filed a rejection schedule covering 44 locations — all under the Select Comfort Retail Corporation entity — with rejection effective as of the Petition Date of June 12, 2026, representing approximately 8% of the total store portfolio. The landlords of these locations are immediately left with capped rejection-damages claims under Bankruptcy Code Section 502(b)(6) — limited to the rent reserved for the greater of (i) one year or (ii) 15% of the remaining lease term (the latter not to exceed three years' rent), plus any unpaid pre-rejection rent — and given the capital structure, those claims face little to no prospect of meaningful recovery in the unsecured creditor pool.

The remaining roughly 528 locations are preserved through closing under tight APA restrictions — the Debtors cannot enter into, modify, or terminate any lease with annual rent exceeding $50,000 without the buyer's prior written consent, and no additional store closures are permitted outside the pre-agreed list. The buyer's real decisions on the surviving portfolio come post-closing, during a Designation Rights Period running up to 60 days after closing (ending earlier if a plan-confirmation hearing is set, and extendable by agreement), in which it formally designates each unassumed lease for assumption and assignment or rejection. Any lease not designated by the deadline is automatically rejected without further court order. With closing targeted by July 31, 2026, that window could extend into late September 2026, meaning the full picture of which locations survive under Sleep Country's ownership will not be known until months after the sale closes.

On assumed leases, prepetition cure costs are capped at $8 million in the aggregate, with any excess reducing the purchase price dollar-for-dollar. On rejected leases, landlords are left with the capped unsecured claims described above. A&G Realty Partners, the Debtors' real estate advisor, is required under the APA to cooperate fully with the buyer through closing, suggesting that location-by-location analysis of the remaining portfolio is already underway in parallel with the sale process.

First-Day Highlights

The employee motion asks the court to authorize continued payment of wages, benefits, and workers' compensation programs for the Company's roughly 2,920 employees. Notably absent from the request is any insider retention package — the Debtors explicitly reserved executive retention for a separate motion subject to the stricter § 503(c) standard, a signal that the case is being run with an eye toward creditor scrutiny.

The customer obligations motion seeks to preserve the consumer relationships that underpin Sleep Number's going-concern value, covering the loyalty rewards program, financing arrangements with Synchrony and Affirm, the 100-night return policy, product warranties, and customer service operations. The theory is straightforward: a buyer paying $415 million for a sleep wellness brand is buying customer trust as much as physical assets, and letting those programs lapse mid-case would erode exactly the value the sale is meant to capture.

The critical vendor motion is the most contested of the three, drawing the U.S. Trustee's objection filed the same day. The Debtors seek authority to pay suppliers, foreign vendors, shippers, and holders of 503(b)(9) claims — capped at approximately $17.3 million in the first three weeks and $35.8 million over the life of the case — arguing that sole-source component suppliers and foreign manufacturers unfamiliar with U.S. bankruptcy law could walk away without immediate payment, jeopardizing the supply chain the stalking horse bidder is counting on remaining intact at closing.

The U.S. Trustee Objection

On the Petition Date, the U.S. Trustee filed an objection challenging two of Sleep Number's most consequential first-day motions: the Critical Vendor Motion and the DIP financing facility.

The objection centers on a straightforward capital structure problem. Sleep Number is selling substantially all of its assets for $415 million while carrying $672.5 million in prepetition secured debt. The DIP facility adds a 3:1 roll-up converting up to $195 million of that prepetition debt into superpriority DIP obligations, places first-priority liens on all previously unencumbered assets, and carries $11.4 million in fees — all for $65 million in new money in a case expected to close roughly seven weeks after filing. Against that backdrop, the U.S. Trustee argues that the Debtors' proposed trade-creditor payments — up to $35.8 million across critical vendors, foreign vendors, lien claimants, and 503(b)(9) claimants — cannot satisfy the legal standard that governs such payments: that favoring certain creditors not prejudice the remaining unsecured creditor body. With sale proceeds expected to flow entirely to secured lenders, the U.S. Trustee contends that unsecured creditors are left with nothing regardless of whether vendor relationships are preserved.

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.