Case Summary: Inotiv Chapter 11

Inotiv filed a prepackaged Chapter 11 to cut funded debt by ~$325 million, after an overleveraged capital structure was compounded by NHP supply-chain strain, federal research-funding uncertainty, and DOJ settlement obligations, backed by an RSA with supermajority support across all voting classes.

A deck version of this summary is also available HERE.

Business Description

Headquartered in West Lafayette, IN, Inotiv, Inc. ("Inotiv"; Nasdaq: NOTV), along with its Debtor⁽¹⁾ and non-Debtor affiliates (collectively, the "Company"), is a leading contract research organization ("CRO") that specializes in nonclinical and analytical drug discovery and development services for the pharmaceutical and medical device industries. The Company also sells a range of research-quality animals to pharmaceutical and medical device companies, other CROs, and academic and governmental organizations.

The Company operates two reportable segments:

- Discovery and Safety Assessment ("DSA"): Discovery, translational-sciences and safety-assessment services—toxicology, pathology, in vivo pharmacology, pharmacokinetics and bioanalysis—on Good Laboratory Practice ("GLP") and non-GLP bases for small molecules, biotherapeutics and biomedical devices.

- Research Models and Services ("RMS"): Offers a wide range of purpose-bred research models essential to basic research and drug discovery, including specialized models for specific diseases and therapeutic areas, as well as diet, bedding, and enrichment products. The segment also provides genetically engineered models and services, client-owned animal colony management, and health monitoring and diagnostics services.

As of the Petition Date, the Debtors employed approximately 1,756 people (1,710 full-time and 46 part-time), all based in the United States.

Inotiv, Inc. and certain affiliates filed for Chapter 11 protection on June 3, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Southern District of Texas, reporting approximately $702.4 million in assets and $625.3 million in liabilities.

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below.

Corporate History

Inotiv began operations in 1975 as Bioanalytical Systems, Inc., a single-site analytical services provider, completing its initial public offering in 1997. On March 18, 2021, the Company formally changed its corporate name to Inotiv, Inc.—ratifying a strategic repositioning already underway to become a vertically integrated, full-service CRO spanning the preclinical drug-development continuum.

Acquisition-Driven Transformation

Between July 2018 and July 2022, Inotiv executed 14 strategic acquisitions, transforming itself into a scaled, two-segment platform. DSA and platform deals added toxicology, pathology, in vivo pharmacology, bioanalysis and surgical-modeling capabilities.

- In July 2018, Inotiv completed an acquisition of Seventh Wave Laboratories — an asset purchase in which Seventh Wave received 1,500,000 then-Bioanalytical Systems common shares and approximately $7 million in cash for substantially all of its assets — broadening the Company's CRO offering with DSA capabilities. Subsequently, the Company completed its acquisitions of Plato BioPharma, a Colorado-based in vivo pharmacology company in October 2021 for $15 million and Protypia, an emerging protein/peptide bioanalytical company in July 2022 for $11 million. Other DSA-related transactions include the Company's acquisitions of Integrated Laboratory Systems, Histion, Bolder BioPATH, HistoTox Labs, Gateway Pharmacology, Pre-Clinical Research Services, and certain assets from BioReliance and the Gaithersburg, Maryland operations from Smithers Avanza.

- The Company established its RMS segment through the acquisition of Envigo RMS Holding Corp. — a leader in the breeding, supply, and distribution of purpose-bred laboratory animals — in November 2021 for approximately $545 million. The Envigo transaction was financed with $215 million in First Lien Term Loans and $140 million in Unsecured Convertible Notes due 2027 (details below in Prepetition Obligations section). Subsequently, the Company acquired Robinson Services, Inc. — a rabbit breeding and supply business — in December 2021, and Orient BioResource Center, a primate quarantine and holding facility near Alice, Texas, in January 2022 in an effort to further strengthen its RMS segment.

Pivot From Expansion to Consolidation

Since 2023, the Company has shifted from buying assets to rationalizing them, focusing on optimization, consolidation and integration. Inotiv reduced its RMS operating footprint from 23 facilities to 11—through site closures, consolidations into the U.K. and Netherlands, and the sale of its Israeli businesses in the fourth quarter of fiscal 2023—to improve efficiency, revenue per facility, service quality and animal welfare.

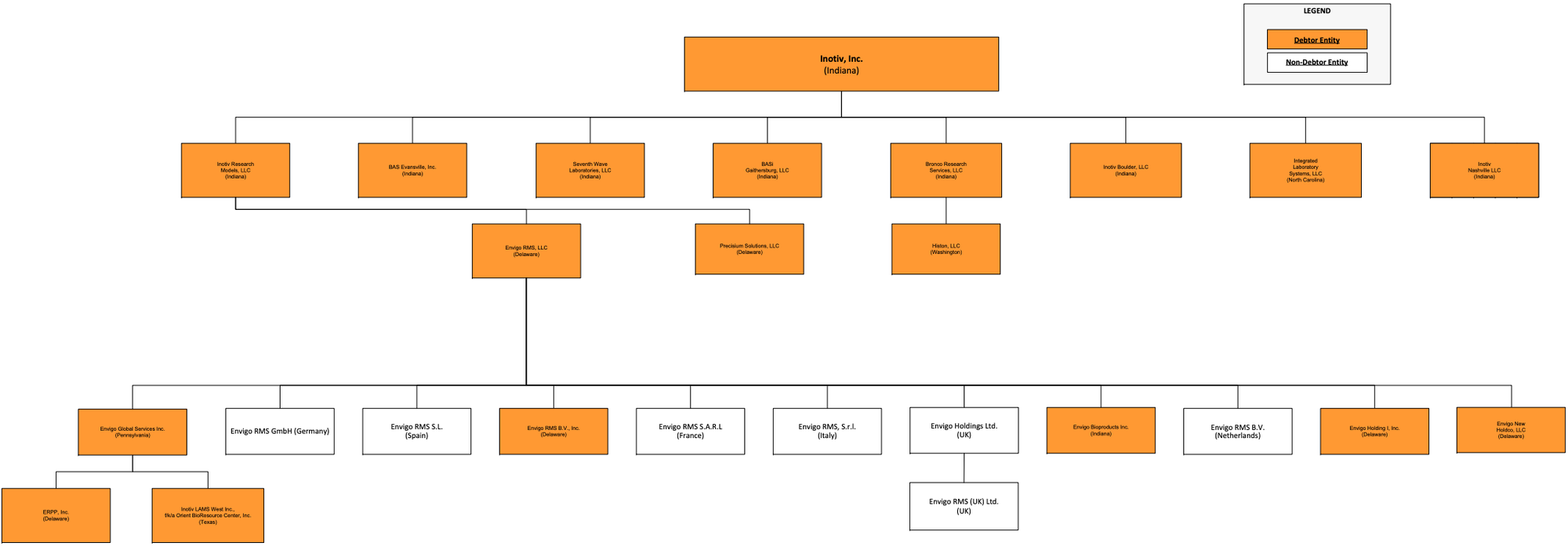

Corporate and Debtor Structure

All 19 Debtors are U.S. entities, organized in Indiana, Delaware, Texas, Pennsylvania, North Carolina and Washington. The Company's European RMS operations are conducted through non-Debtor foreign affiliates excluded from the filing—Envigo RMS GmbH (Germany), Envigo RMS S.L. (Spain), Envigo RMS S.r.l. (Italy), Envigo Holdings Ltd. and Envigo RMS (UK) Ltd. (U.K.), Envigo RMS B.V. (Netherlands) and Envigo RMS S.A.R.L. (France).

- The first lien and second lien collateral packages each extend to "substantially all of the Company's and its domestic subsidiaries' assets," leaving the foreign operating affiliates structurally outside the U.S. collateral.

- Texas Debtor Inotiv LAMS West Inc. is the former Orient BioResource Center, Inc.

Operations Overview

Inotiv operates across 22 sites encompassing 24 owned or leased facilities in four countries—approximately 86% of them in the United States, with the remainder across Europe and the Middle East. The Company also maintains 11 distribution hubs and warehouse facilities to support its Research Model and non-human primate (“NHP”) logistics operations.

Discovery and Safety Assessment (DSA)

The DSA segment is organized into two service areas:

- Discovery and Translational Sciences — Supports early-stage drug development through bioanalytical method development and validation, preclinical in vivo pharmacology (supported by genetically modified rodent production and advanced proteomics), and exploratory pharmacokinetics and toxicology studies designed to evaluate initial drug candidate safety and guide downstream pivotal study design.

- Safety Assessment — Covers the full nonclinical safety testing continuum — from acute drug and medical device evaluation through chronic multi-year oncogenicity studies — including toxicologic pathology, developmental and reproductive toxicology, cardiovascular safety evaluation, surgical modeling, stability testing of dosing formulations, drug metabolism and pharmacokinetics analysis across in vitro and in vivo samples, and climate-controlled archiving services for client data, samples, and specimens.

Research Models and Services (RMS)

The RMS segment operates across three areas:

- Research Models — Produces and sells purpose-bred small animal models (primarily mice and rats) and large animal models (NHPs and rabbits) to pharmaceutical companies, CROs, academic institutions, and government agencies worldwide. Small animal models span outbred, inbred, spontaneous mutant, hybrid, and genetically engineered strains, including proprietary disease-specific models for diabetes, obesity, cardiovascular, and kidney disease research. Large animal models include NHPs — imported from Asia and Africa and processed through three U.S. quarantine facilities — used primarily for biological therapy safety testing, and rabbits bred in the U.K. and U.S. for reproductive safety testing.

- Diet, Bedding and Enrichment — Produces and sells laboratory animal diet, bedding, and enrichment products under the Teklad brand. Offers both standard off-the-shelf and custom diet formulations developed by an in-house nutritionist team. Manufacturing facilities are ISO 9001:2015 certified, with distribution across the U.S., U.K., and Europe and a contract manufacturing relationship in Italy.

- Research Model Services — Provides a range of support services including surgical modifications (cannulation, implants, disease-state models), contract breeding, colony management, health monitoring, transgenic model creation, quarantine, cryopreservation, rederivation, antibody development and production, and transportation services.

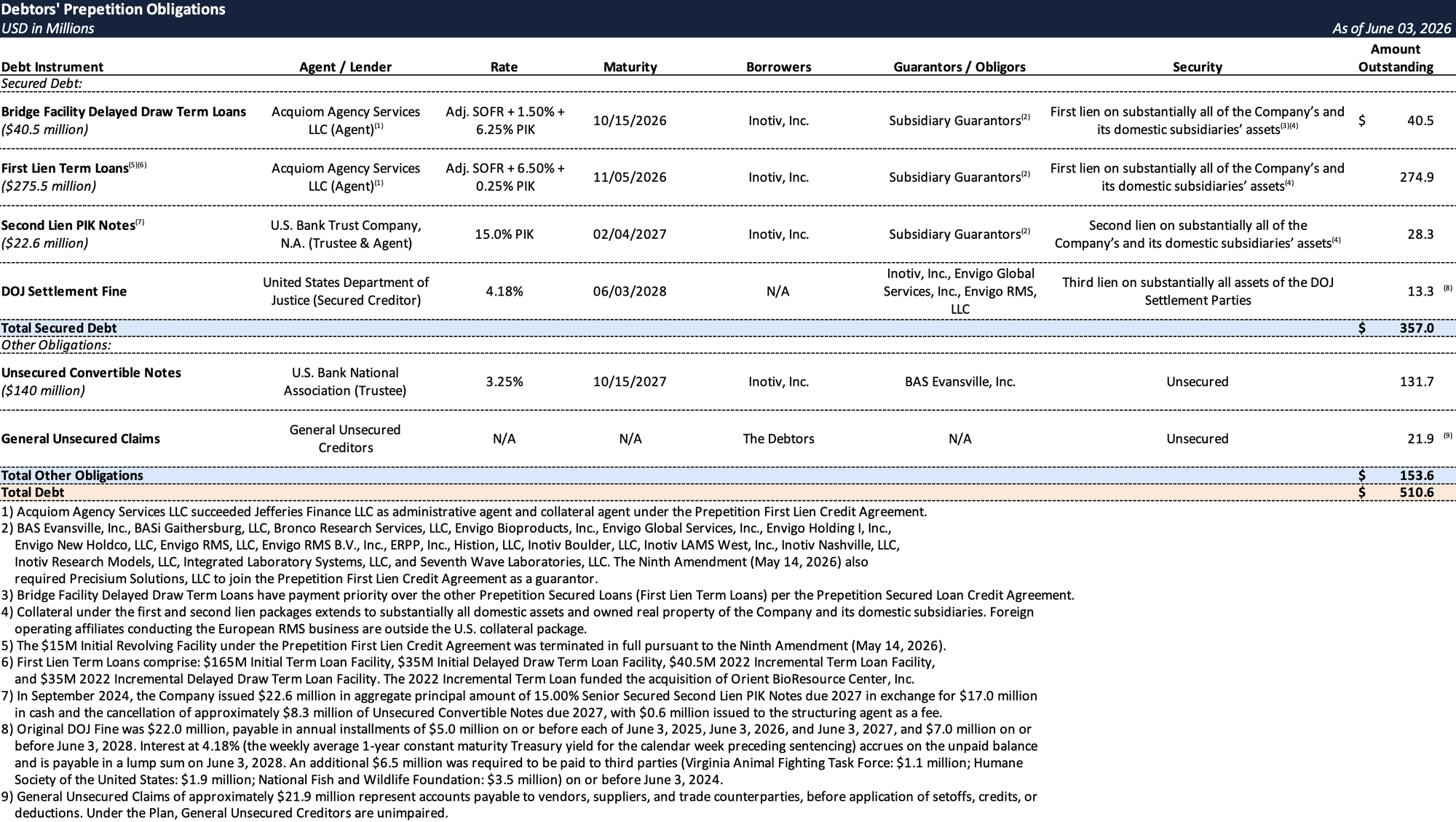

Prepetition Obligations

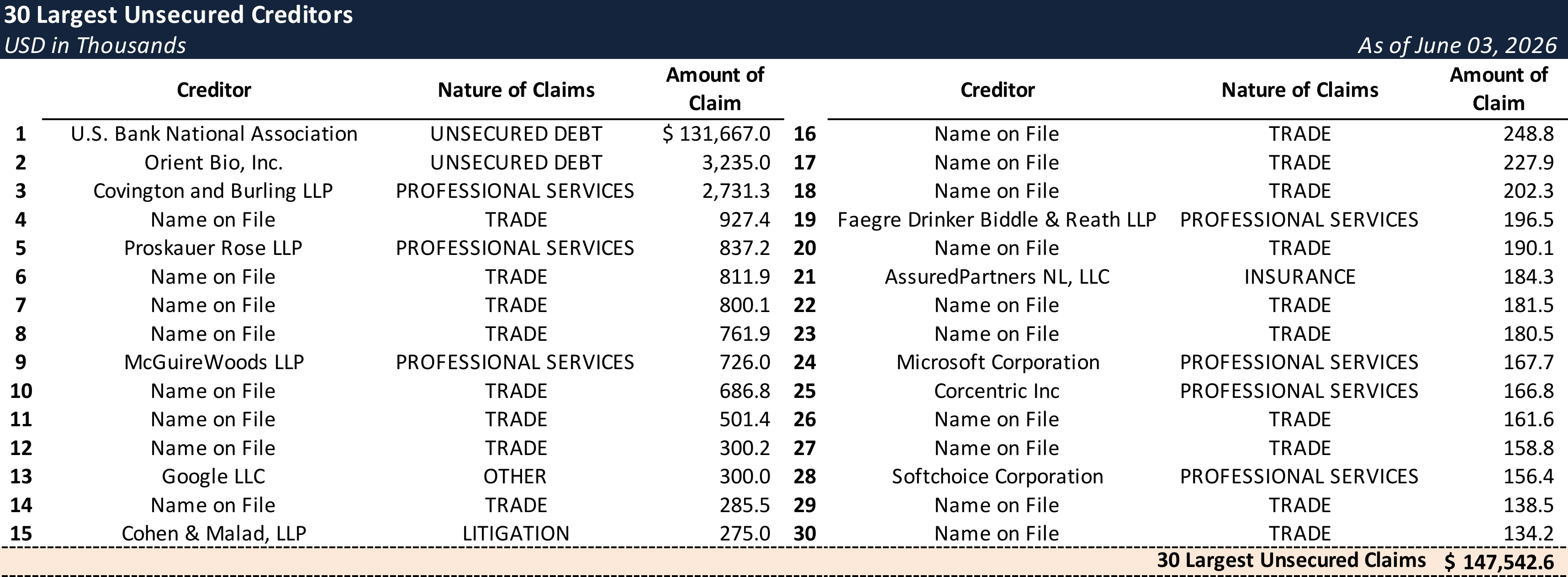

Top Unsecured Claims

Events Leading to Bankruptcy

Inotiv entered Chapter 11 carrying approximately $488.7 million of funded debt it could no longer service. For the first half of fiscal 2026 alone the Company incurred approximately $27.5 million of interest expense at a weighted-average term-loan rate exceeding 11.6%, which the Company warned could eventually divert necessary capital away from operational investments and growth initiatives. With first lien maturities looming in October and November 2026 and substantial doubt about going-concern status flagged across two consecutive quarters, the over-leveraged balance sheet left the Company with no viable path outside of a formal restructuring process.

Market Competition

The CRO and research model industries are highly competitive and have undergone significant consolidation, intensifying pressure on domestic providers like Inotiv. The Company competes against internal R&D departments within client companies, offshore CROs operating in lower-cost and less-regulated markets, and — in the DSA segment specifically — two U.S. and three Chinese public company competitors. In the RMS segment, competitors range from large biopharma companies maintaining their own rodent colonies to one U.S. public company, four privately-held domestic firms, a government-funded not-for-profit, and one privately-held European company. While the RMS segment benefits from significant barriers to entry, the expanding footprint of lower-cost international competitors has nonetheless eroded Inotiv's competitive position.

Regulatory Environment and Industry Headwinds

Inotiv operates in a heavily regulated environment spanning multiple federal agencies. Its animal research facilities are subject to the Animal Welfare Act (enforced by USDA/APHIS), its DSA laboratories must comply with FDA and EPA Good Laboratory Practice regulations, and certain operations involving controlled substances fall under DEA oversight. NHP imports and exports are further governed by the U.S. Fish and Wildlife Service and applicable international conventions. Noncompliance across any of these frameworks can result in fines, license suspension or revocation, disqualification of study data, or criminal prosecution.

- Animal Testing Regulatory Changes - The regulatory landscape has shifted materially against traditional animal-based preclinical testing. The FDA Modernization Act 2.0 (December 2022) removed certain mandatory animal testing references from the Federal Food, Drug, and Cosmetic Act, and in April 2025 the FDA published a roadmap to reduce animal testing through New Approach Methodologies (NAMs), including a framework allowing well-characterized therapeutics such as monoclonal antibodies to seek expedited review based on NAMs data in lieu of traditional animal studies. While the pace and scope of implementation remain uncertain, these developments have introduced structural uncertainty over the long-term demand for the Company's core services.

- Government Funding Reductions - The Company's client base is partially dependent on government-funded research, particularly NIH grants. The Administration has proposed a ~40% reduction to the NIH's ~$47.2 billion annual budget and announced a policy capping indirect cost reimbursements at 15% (down from ~27%), while a proposed consolidation of 27 federal health agencies has added further uncertainty. These pressures contributed directly to measurable financial deterioration: for the six months ended March 31, 2026, RMS revenue fell ~$12.6 million (8.0%) year-over-year on lower NHP volumes, total revenue declined ~$5.7 million (2.3%), and the Company's operating loss widened from ~$18.4 million to ~$35.6 million — all compounded by an overleveraged capital structure that limited the Company's ability to respond.

- NHP Supply Chain Disruptions - The global NHP supply chain has been severely strained since China ceased cynomolgus macaque exports in 2020, forcing a shift to higher-priced suppliers in Vietnam and Mauritius. Compounding this, imported NHPs were subject to tariffs of 10%–20% during fiscal year 2025 and the first half of fiscal 2026, payable within approximately 30 days of import — significantly shorter than the average NHP Research Model inventory turnover period — creating acute working capital pressure.

DOJ Settlement and Compliance Costs

On June 3, 2024, Inotiv entered into a Resolution Agreement and Plea Agreement with the DOJ relating to a canine breeding facility in Cumberland, Virginia. Under the agreement, the Company is obligated to: (a) pay $22.0 million in fines; (b) pay $6.5 million in community and environmental support; (c) spend at least $7.0 million on animal welfare facility and personnel improvements; and (d) maintain a compliance monitor through at least January 20, 2028 tasked with evaluating the Company's compliance and establishing industry-leading standards.

The ongoing compliance burden has had a direct impact on liquidity. For the six months ended March 31, 2026, the Company incurred approximately $5.3 million in third-party and legal costs attributable to the agreement, covering compliance monitor fees and the design and implementation of a nationwide compliance plan. As of the Petition Date, approximately $13.3 million in total liabilities remain outstanding under the agreement, accruing interest at 4.18% per annum with a balloon payment due June 3, 2028. According to the First Day Declaration, the Company's ongoing compliance costs have placed significant and continuing strain on liquidity and operational capacity.

Liquidity Crisis

By early 2026, the Company's liquidity position had deteriorated sharply. Cash fell from $21.7 million at September 30, 2025 to $12.7 million and then $15.2 million over the following two quarters, while revolver borrowings climbed from $3 million to $6 million to $13 million against a $15 million facility — leaving approximately $2 million of availability as of March 31, 2026 and the revolver effectively fully drawn. The quarterly report for the period ended March 31, 2026 concluded that existing cash and cash equivalents, together with cash generated from operations, would not be sufficient to fund operations and satisfy obligations over the next 12 months absent a transaction that positively impacts the Company's liquidity and reduces its debt obligations, and disclosed that the company was exploring potential recapitalization, reorganization, refinancing, or restructuring transactions, or other strategic alternatives.

Against this backdrop, the Company skipped its approximately $2.139 million interest payment due April 15, 2026 on the Convertible Notes. Noteholders extended the applicable grace period to May 29, 2026 and subsequently through June 5, 2026, while the Prepetition First Lien Lenders granted a temporary cross-default waiver through June 3, 2026 to prevent an immediate acceleration event.

Prepetition Restructuring Efforts

Prior to filing, the Company undertook a series of operational initiatives to strengthen its financial position, including facility and system integrations, cost reductions, strategic site consolidations, workforce optimization, investment in technology and NAMs, and engagement with existing lenders on potential recapitalization and refinancing transactions.

The Company retained Ropes & Gray as legal counsel, Perella Weinberg Partners ("PWP") as investment banker, and FTI Consulting as financial advisor to explore strategic and financial alternatives. The Company pursued three primary capital structure alternatives: (i) refinancing the Prepetition Secured Loans, (ii) equitizing the PIK Notes and Convertible Notes in conjunction with a broader refinancing, and (iii) facilitating a Prepetition Secured Loans extension coupled with an equitization of the PIK Notes and Convertible Notes. Beginning in July 2025, PWP led a comprehensive financing outreach process, contacting 87 potential financing parties. Of those contacted, 64 executed non-disclosure agreements and five submitted financing proposals — four of which fell significantly short of the required capital, providing commitment amounts ranging from approximately $175 million to $215 million, less than half of the Company's outstanding funded indebtedness.

The Company ultimately executed a binding term sheet with the sole party to submit a proposal of sufficient size, which committed to provide up to $300 million of new first lien capital in the form of a senior secured term loan. In parallel, the Company reached an agreement in principle with the Prepetition Secured Lenders and Ad Hoc Noteholder Group to equitize their respective claims in connection with the refinancing. However, following approximately eight weeks of due diligence — including on-site visits and negotiation of a new first lien credit agreement — the third-party financing source materially reduced its committed financing from $300 million to a range of $125 million to $150 million on March 10, 2026, an amount insufficient to effectuate the contemplated transaction. Having exhausted all viable refinancing alternatives, the Company secured interim financing from the Prepetition Secured Lenders in the form of the Bridge Facility Delayed Draw Term Loans to fund continued operations while negotiations toward a longer-term solution continued.

The Company simultaneously explored a formal sale process but ultimately declined to pursue one, concluding that the nature of its business severely restricts the universe of potential buyers, that a sale process would not be successful absent a meaningful balance sheet deleveraging. The Company's advisors engaged select strategic acquirors, but these parties were unwilling to acquire the Company with its existing capital structure. Inbound interest in select business units was also deemed insufficient, as any piecemeal transaction would destroy synergies between business units without raising compensatory funds in exchange.

On May 14, 2026, the Company established a Special Committee comprised of two newly appointed independent directors — Eugene I. Davis and John T. Young, Jr. — alongside existing independent director Michael J. Harrington, with exclusive authority to negotiate and approve restructuring transactions.

The RSA and Prepackaged Plan

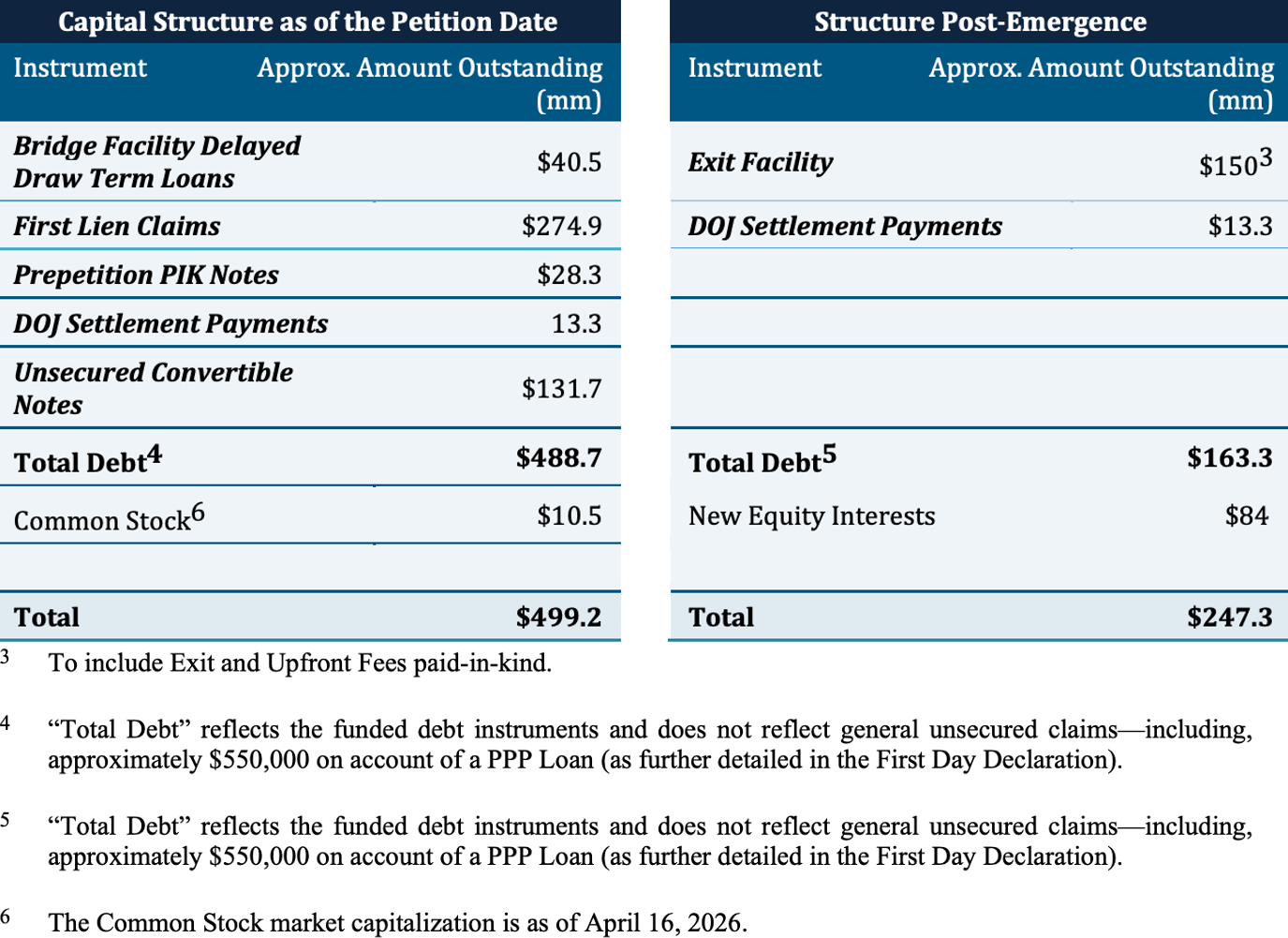

On June 2, 2026, Inotiv executed a restructuring support agreement with its first lien lenders, second lien PIK noteholders and convertible noteholders—each consenting class holding more than two-thirds of its tranche—and filed for Chapter 11 the next day already carrying votes from holders of greater than 99% of first lien loans, 85% of PIK notes and 80% of convertible notes. The plan cuts funded debt by approximately $325.4 million (about 66.6%), to roughly $163.3 million post-emergence (a $150 million exit term loan plus the reinstated $13.3 million DOJ claim), with new equity carried at approximately $84 million in the illustrative post-emergence capital structure.

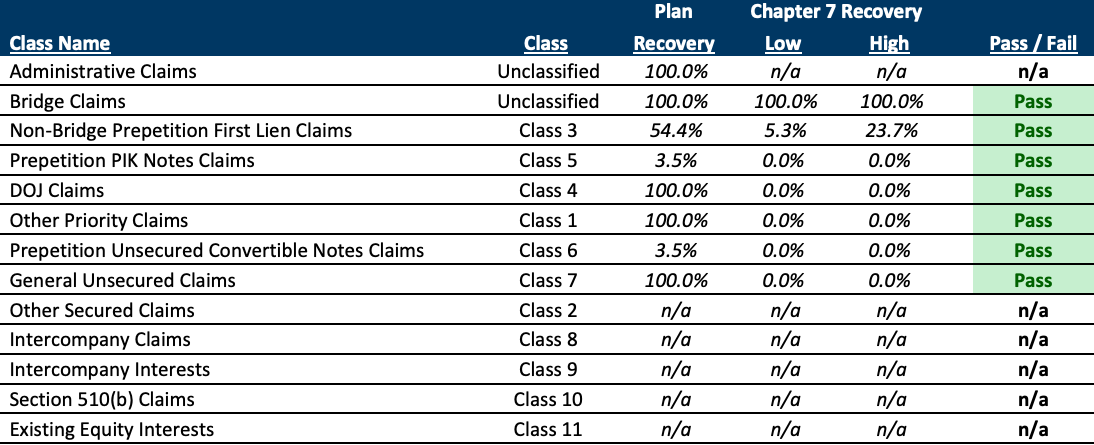

Treatment of Claims

- First Lien Claims (~$315.4 million): Conversion to 93% of new equity, subject to warrant and management-incentive-plan dilution, plus the remaining exit term loans;

- PIK Notes (~$28.3 million) and Convertible Notes (~$131.7 million): 21% and 79%, respectively, of a shared "notes recovery" pool of 7% of new equity plus 100% of the new warrants, which represent 11% of reorganized equity on a fully diluted basis, subject to MIP dilution;

- DOJ Claims: Allowed and reinstated;

- General Unsecured Claims: Unimpaired, 100% recovery, with the Debtors anticipating assumption of all executory contracts and unexpired leases;

- Section 510(b) Claims and Existing Equity: Discharged and cancelled for no recovery; the MIP covers up to 10% of new equity.

Recoveries, Valuation and the Best-Interests Case

The disclosure statement's best-interests analysis frames the plan against a hypothetical chapter 7 conversion:

DIP Financing, Exit and Path Forward

The cases are funded by a $65.5 million DIP facility provided by the Prepetition First Lien Lenders, with Acquiom Agency Services LLC serving as DIP agent. The facility consists of $25.0 million in new-money senior secured superpriority term loans — $16.0 million available upon entry of the interim order and $9.0 million on a delayed-draw basis — plus a $40.5 million dollar-for-dollar roll-up of the prepetition Bridge Facility loans effected upon entry of the interim order. The DIP facility bears interest at Adjusted Term SOFR (subject to a 2.50% floor) plus 11.50%, payable entirely in kind, with a 4.50% upfront fee on new-money commitments, a 3.50% upfront fee on the roll-up, and a 4.50% exit premium, each capitalized and rolled into the exit facility. The facility matures 60 days from the Petition Date, subject to a single 30-day extension with required lender consent. Upon the Plan effective date, all outstanding DIP obligations will convert on a dollar-for-dollar basis into an exit term loan facility of up to $150.0 million, priced at SOFR plus 7.50% (subject to a 1.00% floor) with a five-year maturity and a projected all-in cash cost of approximately 11.00%, alongside a potential approximately $25.0 million working capital facility.

Milestones are tight: interim DIP and scheduling orders within three days; final DIP and confirmation orders within 45 days; effective date within 50 days; and a Consenting Noteholder right to terminate the RSA (which the parties must negotiate in good faith to waive) if the Plan Effective Date does not occur within 75 days of the Petition Date. The confirmation schedule sets a voting, objection and opt-out deadline of July 6, 2026 and a requested combined hearing on July 14, 2026. The Company expects to emerge as a private company within roughly 50 days.

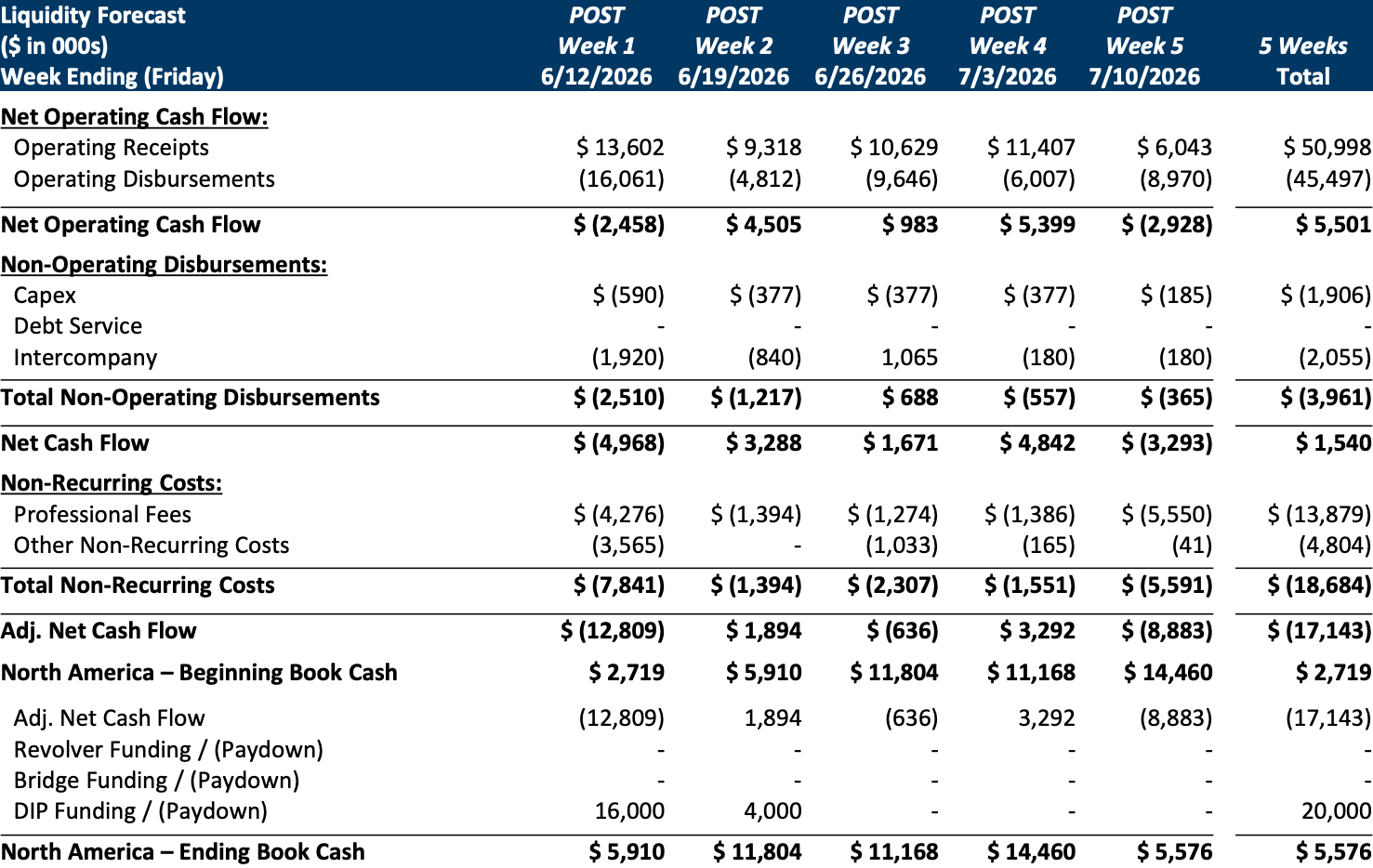

Initial DIP Budget

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.