Case Summary: Trinseo Chapter 11

Trinseo filed a prepackaged Chapter 11 to cut approximately $2 billion of debt, driven by a chemical-sector downturn, Asia-Pacific overcapacity, and liquidity strain following a leveraged expansion into PMMA, supported by an RSA with holders of 78% of funded debt and a parallel Irish examinership.

A deck version of this summary is also available HERE.

Business Description

Headquartered in Wayne, PA, Trinseo PLC, along with its Debtor⁽¹⁾ and non-Debtor affiliates (collectively, "Trinseo" or the "Company"), is a publicly traded specialty chemical manufacturer that makes engineered plastics and latex binders for everyday products across building and construction, automotive, paper and packaging, appliances, textiles, footwear, medical devices, and consumer electronics. Its portfolio spans mass-ABS, SAN, polycarbonate, polystyrene, and PMMA resins and sheet, soft thermoplastic elastomers, and styrene-butadiene and styrene-acrylic latex—sold under brands including MAGNUM™, CALIBRE™, STYRON™, PLEXIGLAS®, and ALTUGLAS®. Individually these inputs are typically a small share of a finished good's cost, but the Company stresses they are highly customized and often critical to its function.

Trinseo operates globally through three operating segments—Engineered Materials, Latex Binders, and Polymer Solutions—plus a 50% interest in the Americas Styrenics LLC ("AmSty") joint venture with Chevron Phillips Chemical Company LP. As of the Petition Date, it ran 32 manufacturing plants and one recycling facility across 28 sites in 14 countries, supported by 11 R&D facilities, and employed roughly 2,800 people worldwide.

Trinseo PLC and certain affiliates⁽²⁾ filed for Chapter 11 protection on May 26, 2026 (the "Petition Date") in the U.S. Bankruptcy Court for the Southern District of Texas, reporting $2.3 billion in assets and $3.4 billion in liabilities.

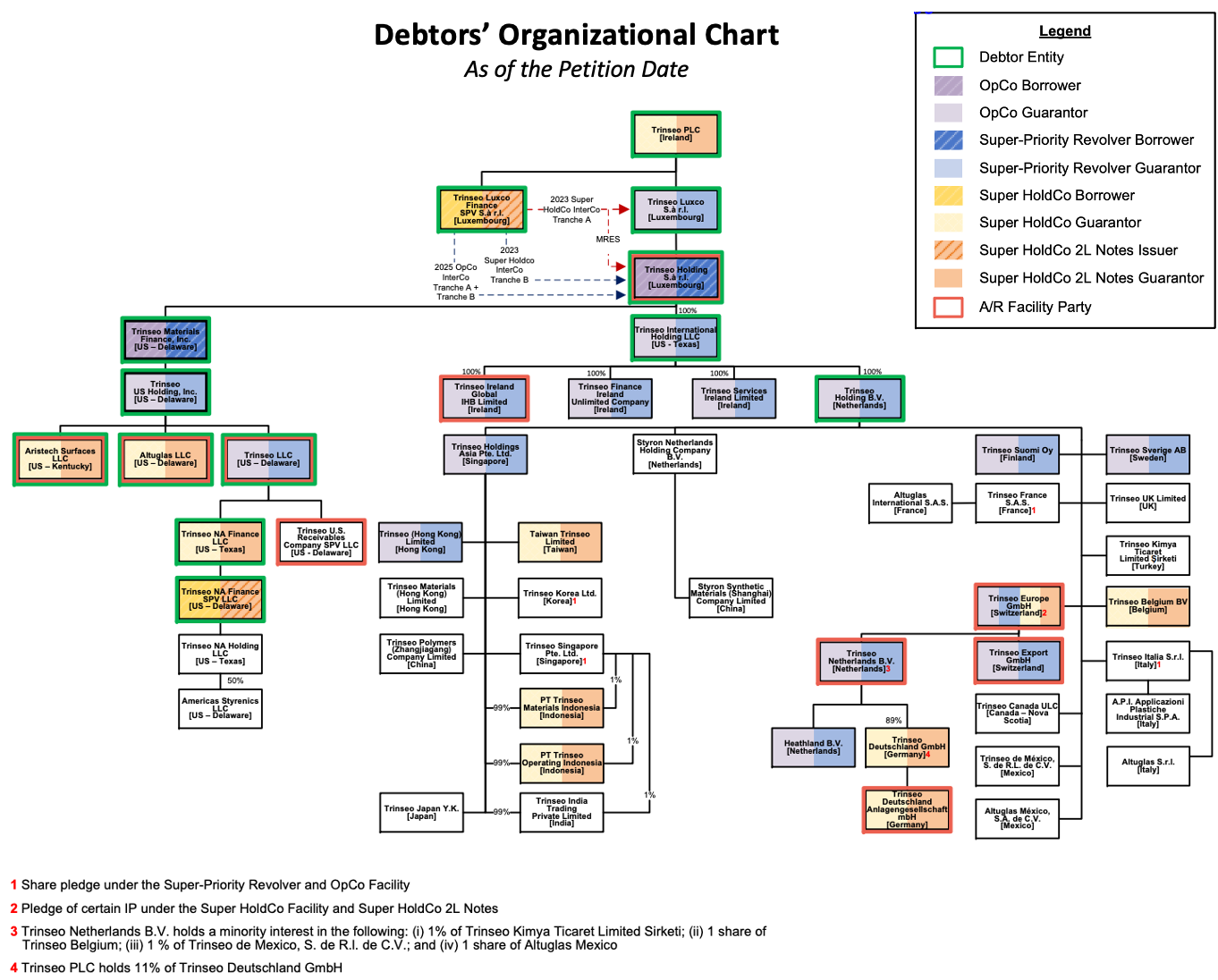

⁽¹⁾ For a complete list of Debtor entities, see organizational structure chart below. ⁽²⁾ Critically, only thirteen entities filed—the Irish parent (Trinseo PLC) and twelve U.S., Luxembourg, and Dutch holding and finance vehicles. The Debtors directly employ only about 718 people, nearly all in the United States. The bulk of the enterprise—the global manufacturing footprint, the operating affiliates across Europe and Asia, and the 50% AmSty interest—sits at the non-Debtor level, which is why the cross-border cash-management and intercompany-funding relief discussed below is essential.

Corporate History

Trinseo began life as Styron, the plastics, rubber, and latex operations that The Dow Chemical Company carved out and sold to an affiliate of Bain Capital Partners, LP in a roughly $1.63 billion leveraged buyout that closed in June 2010. The Company listed on the New York Stock Exchange under the ticker "TSE" in a 2014 IPO, and Bain Capital fully exited by 2016. Christopher Pappas led the business from the buyout until March 2019, when Frank Bozich — now President and CEO — succeeded him; David Stasse serves as CFO.

On October 8, 2021, the publicly traded parent, Luxembourg-domiciled Trinseo S.A., merged into Trinseo PLC, an Irish public limited company. That redomicile matters: the Irish parentage is what enables the dual-track restructuring, pairing the U.S. Chapter 11 cases with a parallel Irish examinership to implement the parent-level transactions.

Acquisitions & Divestitures

Under Bozich, Trinseo pursued a multi-year pivot away from cyclical, commodity styrenics toward higher-margin specialty materials. The centerpiece was the May 2021 acquisition of Arkema S.A.'s PMMA and methyl methacrylate businesses — owner of the Plexiglas and Altuglas franchises — for approximately €1.12 billion (~$1.36 billion). This acquisition was primarily debt funded through $450M in 2029 unsecured senior notes (which later got exchanged to the second lien notes in 2025), and $750M in incremental term loan borrowings. Subsequently, in September 2021, Trinseo acquired North American cast-sheet and solid-surface producer Aristech Surfaces LLC for $445 million.

The Company also completed several divestitures prior to the Petition Date. It sold its Schkopau, Germany synthetic rubber business to Synthos S.A. for roughly $491 million in December 2021, and in 2024 decommissioned its virgin polycarbonate facility in Stade, Germany and in November 2024 agreed to sell the related virgin-polycarbonate technology license and Stade production assets to Deepak Chem Tech Limited for approximately $52.5 million, with delivery completed in 2025.

In March 2024, Trinseo commenced a process to sell their 50% interests in AmSty, however, no transaction had closed as of the Petition Date, and Trinseo continues to hold its 50% stake.

NYSE Delisting

The Company's distress surfaced publicly in its share price. After a December 2025 NYSE notice that the Company had fallen out of compliance with two continued-listing standards — minimum market capitalization and the $1.00 minimum share price, the NYSE notified Trinseo on March 2, 2026 that it was commencing delisting proceedings for failure to maintain a minimum average global market capitalization. Trinseo did not appeal; the delisting became effective March 30, 2026, and its ordinary shares now trade on the OTC Pink market under "TSEOF."

Organizational Structure

Operations Overview

Following segment realignments through 2024 — the Company ceased styrene manufacturing effective January 1, 2024 (dropping the Feedstocks segment) and, on October 1, 2024, combined its Plastics Solutions and Polystyrene businesses into the new Polymer Solutions segment — Trinseo now reports four reportable segments — Engineered Materials, Latex Binders, Polymer Solutions, and Americas Styrenics (the last consisting solely of its 50% interest in AmSty joint venture).

- Engineered Materials makes rigid and soft thermoplastic compounds, cell-cast PMMA sheet, and PMMA resins (the Plexiglas/Altuglas franchises) for higher-growth consumer-electronics, medical-device, footwear, automotive, and construction applications. In 2025, the Engineered Materials segment generated $1.08 billion in net sales, approximately 36% of which is in Europe, 49% in the United States, and 15% in the Asia Pacific region.

- Latex Binders produces SB and styrene-acrylic latex and related binders for paper and board, carpet and turf, and coatings/adhesives - a segment where Trinseo is a global leader. In 2025, the Latex Binders segment generated approximately $788 million in net sales, 38% of which came from Europe, 31% from the United States, and 31% from Asia.

- Polymer Solutions produces mass ABS, styrene-acrylonitrile, and polystyrene under the MAGNUM™, CALIBRE™, and STYRON™ brands, primarily for automotive, building, and construction applications. The segment also recycles post-consumer and post-industrial thermoplastic waste—PMMA, polycarbonate, ABS, and polystyrene—into high-quality materials for premium manufacturers. In 2025, Polymer Solutions generated $1.1 billion in net sales, of which ~59% came from Europe, 28% from Asia Pacific, and 13% from North America.

- Americas Styrenics is a leading Americas producer of both styrene and polystyrene. Styrene is a key feedstock for polystyrene, which serves a broad range of end markets including appliances, food packaging, food service disposables, consumer electronics, and building and construction—as well as polystyrene foam products such as DuPont's STYROFOAM®.

Workforce Overview

Trinseo's global headcount stands at approximately 2,800 employees as of the Petition Date, with the majority—roughly 55%—based across Europe and the Middle East, 30% in the Americas, and the remainder in Asia-Pacific. Of that total, 718 employees are directly employed by the Debtor entities, nearly all of whom are based in the United States, with one employee in Luxembourg supporting corporate operations.

Approximately 252 Debtor employees are covered by collective bargaining agreements. The Debtors also engage around 15 contract workers and temporary staff to supplement their workforce on discrete projects and specialized functions.

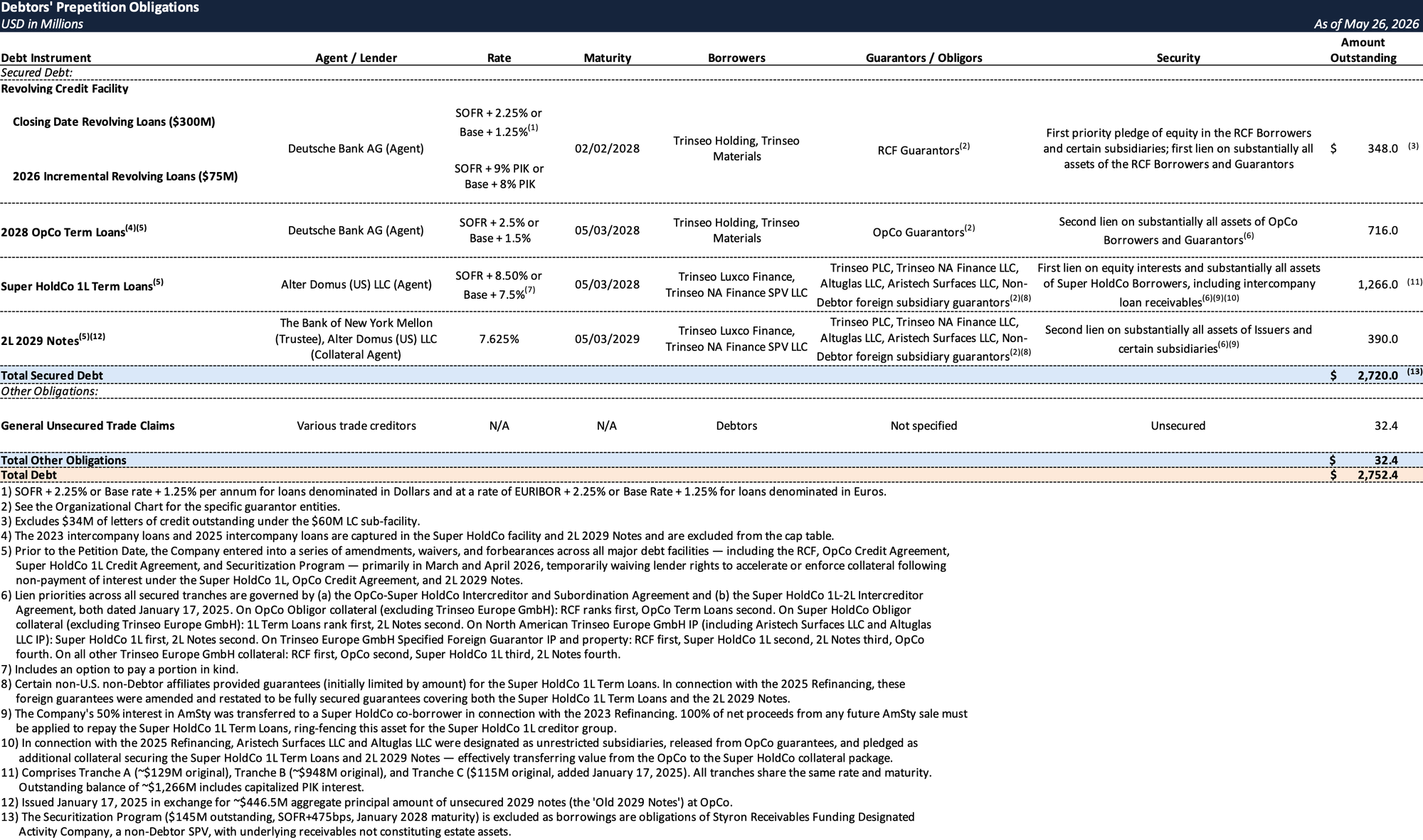

Prepetition Obligations

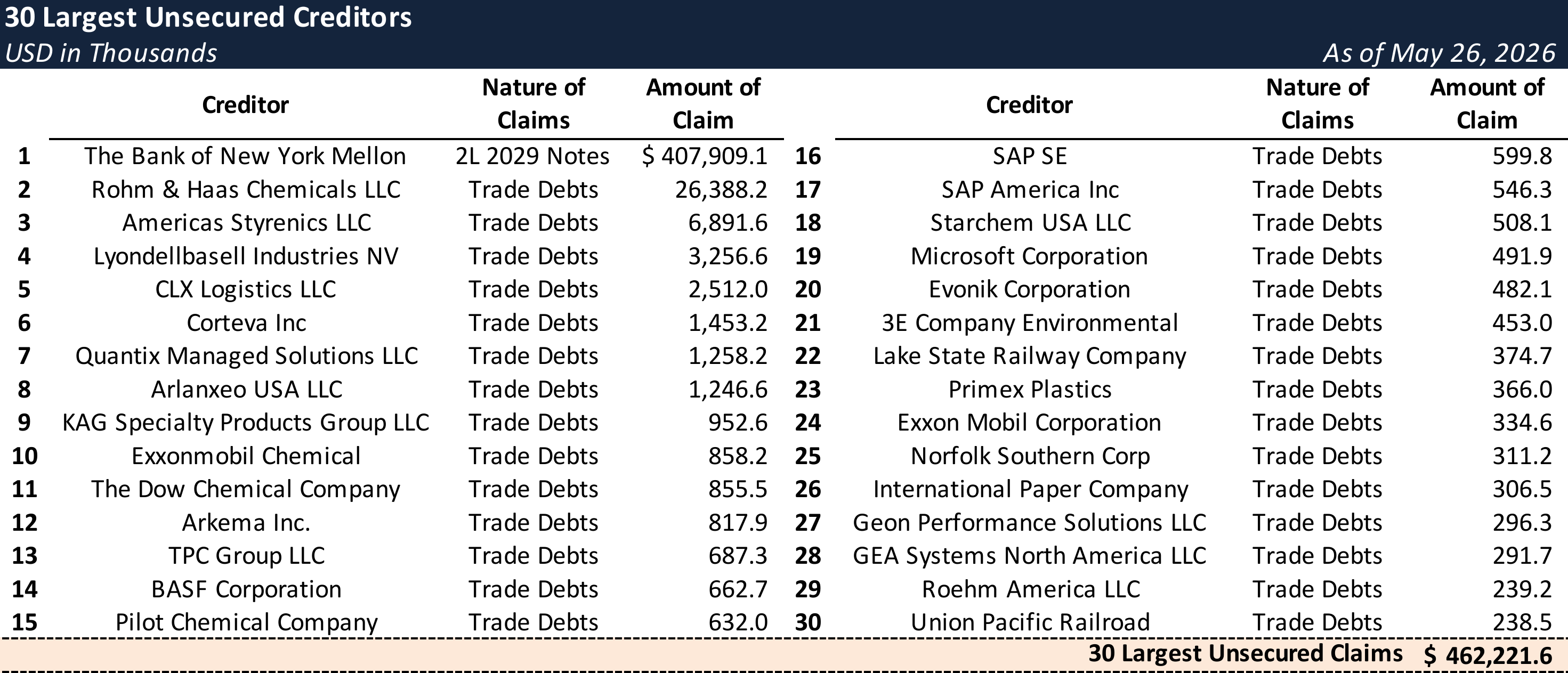

Top Unsecured Claims

Events Leading to Bankruptcy

Macroeconomic Headwinds

Trinseo was overtaken by a sustained, severe chemical-sector downturn that hit precisely its core product chains. Structural Asia-Pacific overcapacity collided with a European cost disadvantage rooted in elevated energy prices following Russia's invasion of Ukraine and ongoing Middle East conflict, compressing margins across Trinseo's polystyrene, PMMA, and ABS portfolios. The damage was amplified by a company-specific vulnerability: having exited upstream European styrene production in 2022 and 2023, Trinseo was left more reliant on merchant styrene and increasingly exposed to import competition at the worst possible moment.

The April 2025 U.S. "reciprocal" tariff regime and broader trade-policy volatility weakened demand and drove customer destocking, and S&P tied weak volumes to "global tariff uncertainty and changing customer purchasing patterns." The First Day Declaration concedes demand is not expected to recover "until 2027 at the earliest". Net sales fell roughly 15% to $2.975 billion in 2025 and 2025 Adjusted EBITDA was just $162.5 million against ~$2.9 billion of funded debt.

Operational Restructuring Attempts & Liquidity Strain

Trinseo undertook an aggressive restructuring of its global manufacturing footprint in response to market challenges, closing or announcing the permanent closure of eight facilities across five countries. The closures were concentrated in European commodity chemical production — styrene facilities in Boehlen, Germany and Terneuzen, the Netherlands; virgin polycarbonate manufacturing in Stade, Germany; PMMA cast sheets in Bronderslev, Denmark; methyl methacrylate in Rho, Italy; acetone cyanohydrin production in Porto Marghera, Italy; and polystyrene manufacturing in Schkopau, Germany. The only North American closure was a batch polyester tray casting plant in Belen, New Mexico.

Despite the breadth of these initiatives, the operational restructuring proved insufficient to offset the structural deterioration in demand and the unsustainable weight of the Company's debt burden. Liquidity fell from $334.2 million at year-end 2025 to $114.2 million by March 31, 2026. Trinseo then elected to skip interest payments—deferring ~$10.0 million on the 2029 second-lien notes (grace begun February 17, 2026) and ~$12.0 million on the 2028 term loan (February 27, 2026), neither paid by the March 19, 2026 grace-period expiry, and later a further ~$38.2 million on the 2028 Refinance Term Loans (delayed April 14, 2026) — which — after the grace periods expired March 19, 2026—constituted events of default under the Senior Credit Agreement (2028 term loan) and the 2L Notes Indenture (2029 notes) and triggered cross-defaults under the Refinance Credit Agreement, the OpCo Super-Priority Revolver, and the A/R Securitization Facility, accelerating the related debt. By the Petition Date, total liquidity had fallen to approximately $65 million, well below the $125 million minimum the Company historically maintained, per the Boyko DIP Declaration.

Governance and Independent Investigations

Recognizing the divergent interests of its OpCo and Super HoldCo creditor groups, the Company installed independent fiduciaries in January 2026. The OpCo obligors appointed M. Elizabeth Abrams and Alan J. Carr (advised by Quinn Emanuel and Portage Point) to run an independent investigation of intercompany and prepetition claims; the Super HoldCo obligors appointed Jill Frizzley and Carol Flaton (advised by McDermott Will & Schulte) to run a parallel review. The OpCo Investigation analyzed the OpCo transaction documentation over the relevant period (including the 2023 Refinancing, the 2025 Refinancing, and the 2026 Financings) and identified as challengeable only the make-whole, yield-protection, prepayment, and similar premiums on the OpCo Intercompany Term Loans (the "Specified Claims").

The Prepackaged Restructuring

On May 13, 2026, the Debtors executed a Restructuring Support Agreement backed by holders of 78% of total funded debt — comprising 100% of RCF claims, approximately 99.9% of Super HoldCo 1L claims, and approximately 86% of OpCo term loan claims. The 86% figure, however, overstates the true consensus: it includes the $1.508 billion intercompany term loan held by a supporting Super HoldCo entity, which mechanically inflates the participation rate. Stripped of that balance, only approximately 57.2% of third-party-held 2028 OpCo term loans signed the RSA — the most telling consent figure, as the 2028 tranche is where dissent is concentrated. That margin is thin: the RSA terminates as a Company termination event if supporting OpCo 2028 lender participation falls below 50.1%, leaving just 7.1 percentage points of cushion.

The prepackaged Plan delivers an approximately $2 billion reduction in funded debt and roughly $140 million in annual interest savings, anchored by a $142.5 million new money DIP, a fully backstopped $450 million equity rights offering, post-emergence revolving credit facility of at least $200 million, an approximately $850 million exit term loan, refinancing of the $150 million accounts receivables facility, and a parallel Irish examinership process.

At the heart of the Plan is a global Intercompany Settlement resolving cross-silo disputes without litigation. The Settlement allows the OpCo Intercompany Term Loan Claim at $1.5 billion, with the Specified Claims — make-whole premiums, yield protection fees, and prepayment premiums — surrendered and excluded. Because the intercompany lender, Trinseo Luxco Finance, is simultaneously the lead Super HoldCo borrower, the allowed claim channels OpCo value upward into the Super HoldCo silo, with the associated equity subscription rights flowing to Super HoldCo 1L holders.

Value also flows in the other direction: through a collateral carve-out, Trinseo Luxco Finance gifts its pro-rata share of the $35 million OpCo Exit Distribution — approximately $23.7 million — to Supporting OpCo 2028 Term Lenders, with the entire $35 million effectively landing with the OpCo 2028 cohort. The Settlement is best read as the senior creditor groups paying targeted consideration to the impaired OpCo 2028 cohort to secure consensual confirmation — not as the estate realizing litigation value.

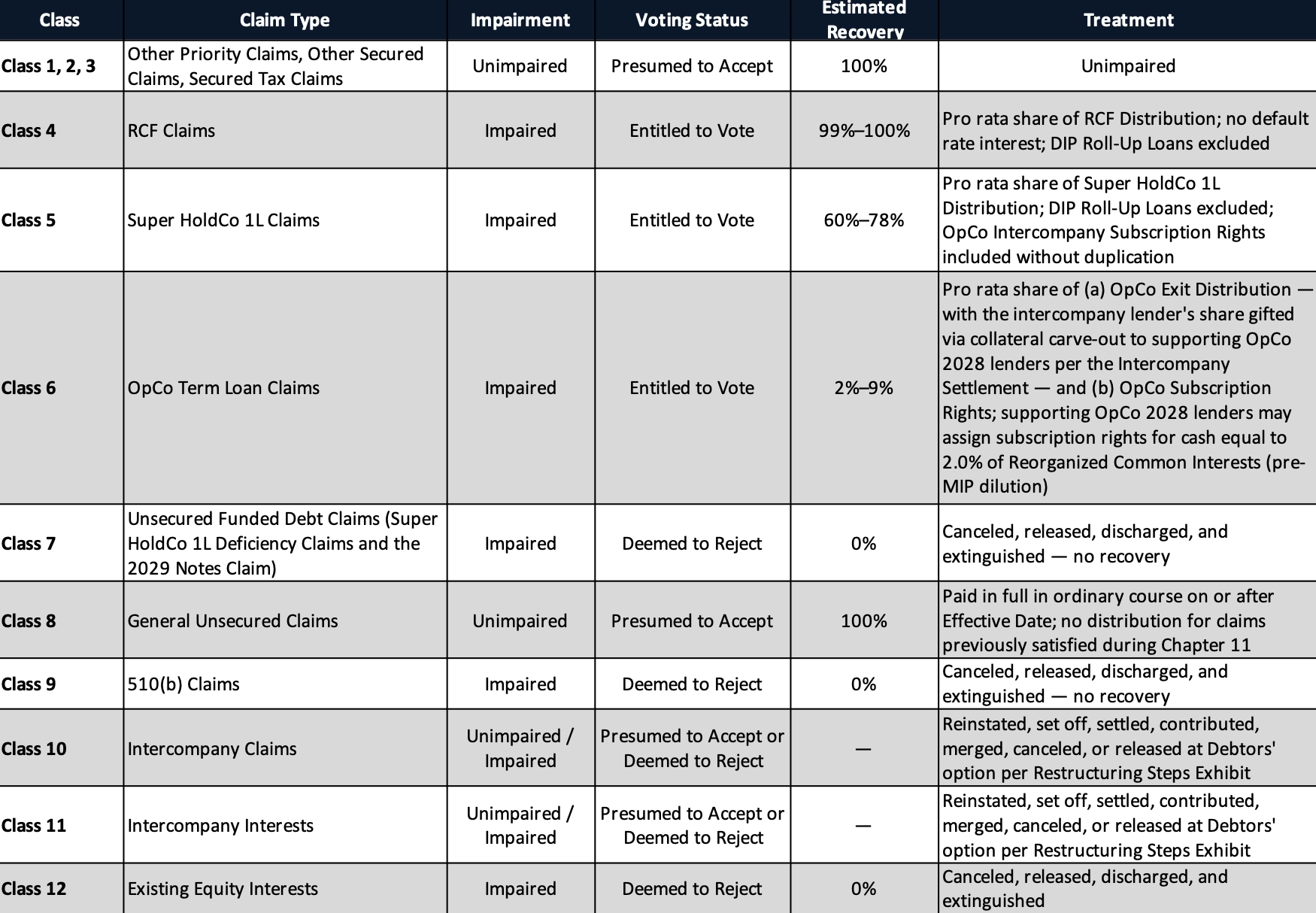

Recoveries and the Fulcrum

The Plan is a separate plan for each of the thirteen Debtors (no substantive consolidation); only Classes 4, 5, and 6 vote. Estimated recoveries expose the gulf between the silos:

The super-priority RCF is made nearly whole at 99%–100%, consistent with its first-lien position on OpCo assets. The Super HoldCo 1L is the fulcrum security: holders receive an $810 million distribution in takeback term loans and cash, 10% of reorganized equity, and the lion's share of the rights offering — yet recover only 60%–78% on a blended basis, confirming that reorganized enterprise value falls short of repaying the 1L in full and that residual equity vests in this class. Below the break, OpCo Term Loan holders recover 2%–9%, while the 2L 2029 Notes and existing equity are wiped out entirely at 0%. General unsecured trade claims — estimated at approximately $32.4 million, or roughly 1.1% of total funded debt — are unimpaired and paid in full in the ordinary course.

DIP Financing and Timeline

The Chapter 11 cases are funded by two senior secured, superpriority, priming DIP term facilities provided by the Ad Hoc Group of Senior Secured Creditors — a $270 million OpCo facility ($90 million of which is new money) and a $157.5 million Super HoldCo facility ($52.5 million of which is new money) — totaling $427.5 million in aggregate commitments, comprising $142.5 million in new money against $285 million of rolled-up prepetition claims on a 2:1 ratio. New money loans bear interest at Term SOFR+9.00%. The interim DIP orders allow an initial new-money draw of $95 million ($60 million OpCo / $35 million Super HoldCo) against the full $142.5 million committed, plus up to $190 million of cashless roll-up at the 2:1 ratio; the balance unlocks at the final DIP hearing scheduled for June 18, 2026 (objections due June 11). The DIP carries $100 million / $25 million minimum-liquidity covenants and a 17.5% disbursement variance. The Securitization Program is simultaneously replaced with a postpetition equivalent to maintain ongoing receivables liquidity.

A critical first-day measure embedded in the DIP structure is a one-time cash infusion of approximately $58 million to non-Debtor foreign affiliates, funded upon entry of the Interim DIP Order. As the CRO testified, without this infusion foreign affiliates risked exiting the Company's cash-pooling arrangements or initiating their own insolvency proceedings — an outcome that would have destabilized Trinseo's foreign manufacturing footprint, supply chain, and in-house treasury infrastructure at the outset of the case.

Because Trinseo PLC is an Irish public limited company, U.S. plan confirmation alone cannot cancel and reissue parent-level equity. Accordingly, the Company will run a parallel Irish examinership under Part 10 of the Companies Act 2014 following U.S. confirmation. Confirmation of the Irish Scheme of Arrangement is an express condition precedent to the U.S. Plan's effectiveness — a structural dependency the Company acknowledges carries risk, including the potential for a creditor to object on the basis that the Irish parent lacks a standalone going concern undertaking.

The RSA sets a Confirmation Order within 60 days of filing, emergence within 180 days, a voting deadline of July 17, 2026 (Doc. 178), and a combined disclosure-statement and confirmation hearing targeted for July 27, 2026 (Doc. 178).

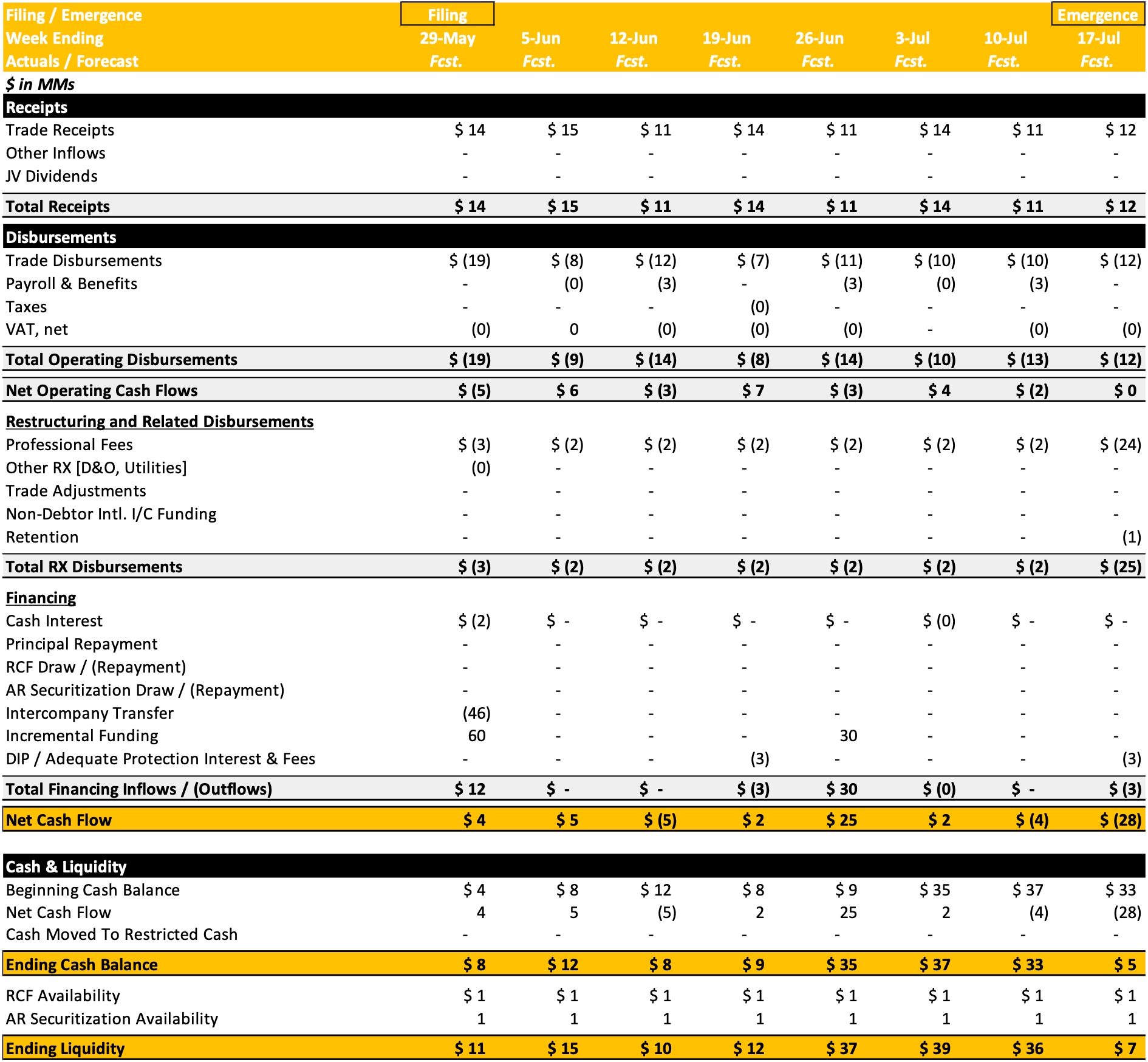

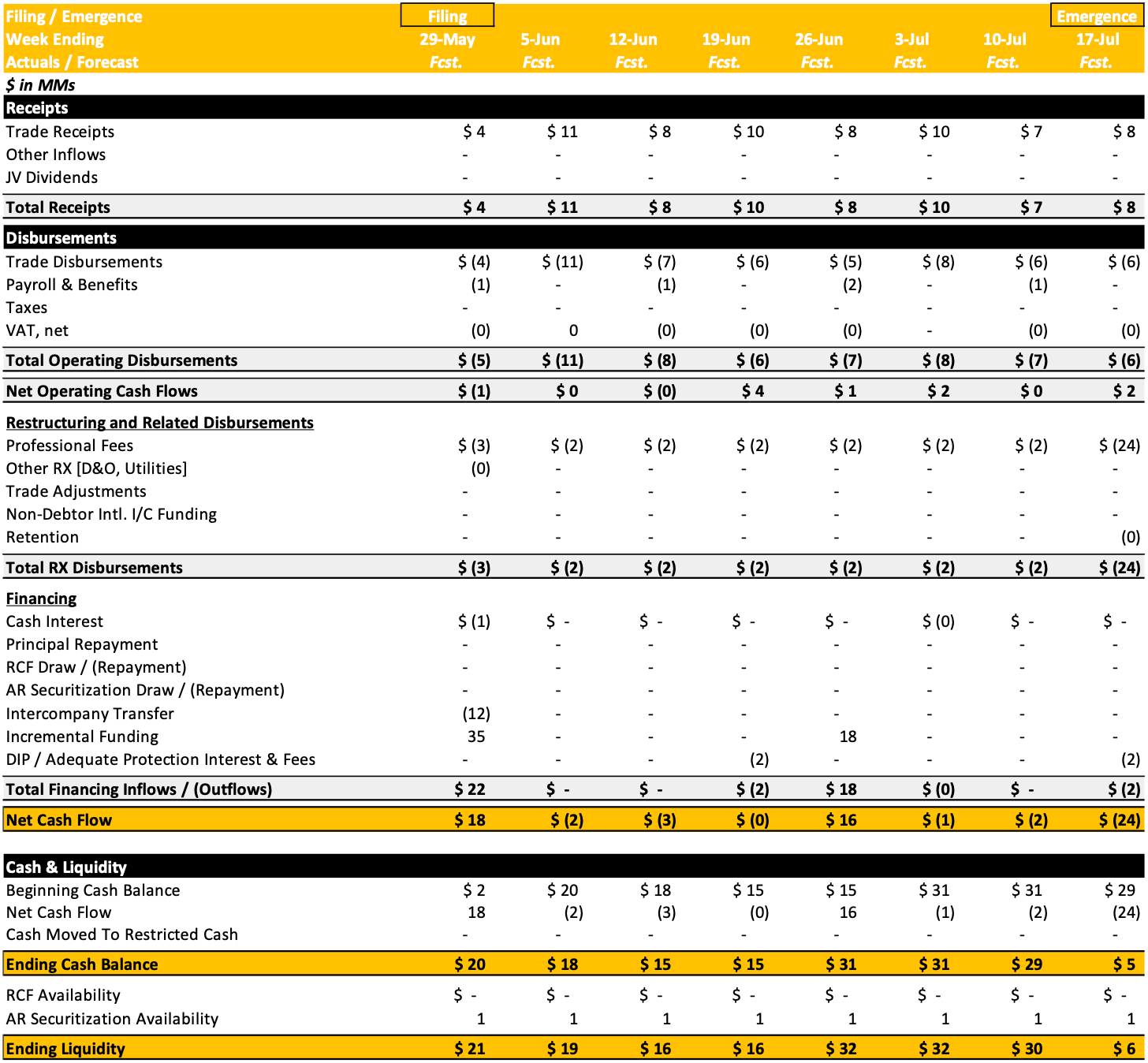

The cashflow forecasts at OpCo and SuperHoldCo entity level are shown below.

OpCo Filing Cash Flow

Super HoldCo Filing Cash Flow

The Contested Confirmation

The restructuring is contested. The dissent is led by the Ad Hoc Group of Excluded OpCo Term Lenders — sixteen funds anchored by CastleKnight Master Fund L.P. (holding $271.8 million of 2028 OpCo Term Loans plus $93.5 million of 2L 2029 Notes), together with eight ArrowMark-managed Elevation CLOs and seven Signal Peak CLOs — collectively holding approximately $293.7 million, or 40% of 2028 OpCo Term Loans. Represented by Pallas Partners (US) LLP and Gray Reed, the group filed a 70-page objection to conditional approval of the Disclosure Statement and commenced Adversary Proceeding No. 26-03208 against the Super HoldCo Lenders (funds managed by Angelo Gordon, Apollo, Oaktree, and TPG AG), Alter Domus, Deutsche Bank, and four Trinseo Debtor entities. The four-count complaint seeks (i) a declaratory judgment voiding the 2023 and 2025 credit-agreement amendments, the ~$948 million 2023 intercompany loan, the ~$494.5 million 2025 intercompany loan, and the Intercreditor Agreement ab initio; (ii) recharacterization of the OpCo intercompany loans as equity; (iii) equitable subordination of Trinseo Luxco Finance SPV's intercompany loan claims; and (iv) equitable subordination of the Super HoldCo Lenders' acquired OpCo RCF claims.

The 2028 OpCo lenders’ disclosure statement objection rests on 6 principal grounds: (a) The Debtors stuffed a $1.508B intercompany claim into Class 6 alongside third-party lenders, giving it 68% of the class by value and effectively drowning out outside creditor votes; (b) Plan supporters receive ~$56M in exclusive perks — a cash gift, premium interest, allocation interest, and equity backstop rights — that non-supporters don't get, which violates the equal treatment requirement; (c) The intercompany claimant (Luxco SPV) is a Debtor affiliate, and if its vote gets stripped, the plan loses its only accepting impaired class and fails the §1129(a)(10) confirmation test; (d) The Debtors frame surrendering make-whole and prepayment premium claims as meaningful consideration, but those claims are routinely disallowed in bankruptcy as unmatured interest anyway — so the concession is effectively worthless; (e) The Super HoldCo Lenders acquired the prepetition RCF, caused Trinseo to draw $60M+, then diverted the proceeds up to HoldCo collateral before filing — a manufactured priority grab the objectors call a "pre-DIP DIP" that warrants equitable subordination. (f) Four days to object to the disclosure statement and 45 days to confirmation is unreasonably compressed for a case this complex.

A separate 2L 2029 Noteholder Group represented by Paul, Weiss and Porter Hedges — is organized around five members holding approximately $136.3 million of 2L 2029 Notes: JPMorgan Investment Management (~$64.5 million), Wasserstein Debt Opportunities (~$30.1 million), Nomura Corporate Research and Asset Management (~$19.6 million), Hotchkis & Wiley (~$15.2 million), and BlackRock (~$6.8 million). Combined with CastleKnight's $93.5 million 2L position held through the Excluded OpCo group, approximately $229.8 million — or roughly 59% — of the ~$390 million 2L tranche is organized against the 0% Class 7 treatment. This group has reserved rights against First Day relief and flagged fiduciary-duty concerns over the Class 7 deemed-rejection treatment without "genuine engagement."

Explore Bondoro Insights for live case dockets and comprehensive coverage of material filings from petition to plan confirmation.

Stay informed on every Chapter 11 bankruptcy case with liabilities exceeding $10 million. Subscribe for free to have our coverage delivered directly to your inbox, and explore our full archive of past summaries.

Subscribers can also opt in to timely filing alerts by updating their email preferences in Account Settings.